Introduction

The Central Board of Indirect Taxes and Customs (‘CBIC’) has issued a new circular[i] to clarify the provisions of clause (ca) of s. 10(1) of the Integrated Goods and Services Tax Act, 2017 (‘IGST Act’). The circular clarifies the determination of the place of supply of goods to unregistered persons, especially in scenarios where the billing and delivery addresses differ. The clarification follows the amendment brought by notification[ii], due to which the IGST (Amendment) Act, 2023 (31 of 2023) came into force from 01.10.2023.

Key Highlights

1. Clause (ca):

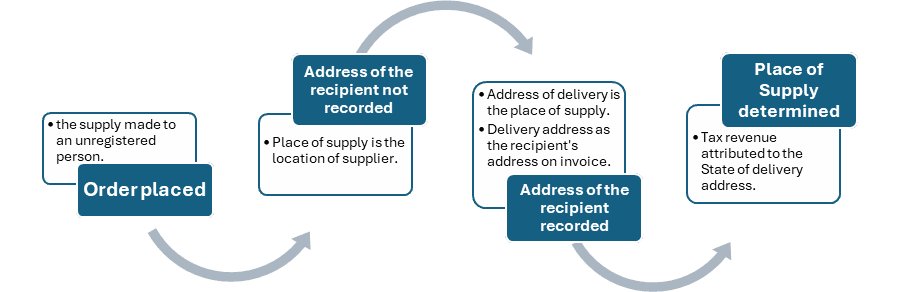

Clause (ca) was added to s. 10(1) of the IGST Act specifies that for supplies made to unregistered persons, the place of supply shall be the location as per the address recorded in the invoice. If the address is not recorded, the location of the supplier will be considered. An explanation clarifies that recording the name of the state on the invoice is deemed to be recording the address.

2. Clarification on Billing and Delivery Addresses:

The CBIC received queries about scenarios where the billing address differs from the delivery address, especially for e-commerce transactions.

For instance, if Mr. A from State X orders a mobile phone to be delivered to State Y and provides State X as the billing address, the place of supply will be the delivery address, i.e., State Y.

Suppliers can record the delivery address as the recipient’s address on the invoice to determine the place of supply.

Illustration

Conclusion

The circular provides a definitive framework for determining the place of supply for goods to unregistered persons, especially in e-commerce transactions. By establishing that the delivery address is the decisive location for supply, businesses can more accurately manage tax liabilities and reduce confusion in dealings with unregistered buyers. This clarity not only ensures compliance but also carries substantial economic advantages. For example, allocating tax revenues to the state where goods are delivered enhances local infrastructure and public services, ensuring that taxes contribute to regions where consumption actually occurs. Furthermore, this clarification simplifies tax calculations for businesses, significantly reducing administrative burdens and diminishing the risk of disputes over tax jurisdictions.

End Notes

[i] Circular No.209/3/2024-GST, Dated: 26.06.2024.

[ii] Notification 02/2023-Integrated Tax, Dated 29.09.2023.

Authored by Priyavansh Kaushik, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinion.

AUTHORED BY

More Insights

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.

2026-04-23

18

min read

Mandatory Pre-Deposit for Appeals in Indirect Tax Laws: A Barrier to Justice?

Mandatory pre-deposit has become a defining feature of indirect tax litigation, balancing revenue protection with access to appellate remedies. While the shift to a fixed statutory framework has improved procedural efficiency, it also raises concerns regarding financial barriers and effective access to justice. This insight examines the legal evolution, judicial interpretation, and practical implications of the regime.

2026-04-20

10

min read

Legal Strategy in Startup Ecosystems: Risk Mitigation and Value Maximisation from Formation to Exit

Legal structuring across the startup lifecycle extends beyond compliance to shape valuation, governance, and investor confidence. From intellectual property protection and entity selection to funding arrangements and exit mechanisms, each stage involves critical legal considerations that determine risk allocation and long-term scalability within a regulated framework.