Blogs

Insights and Resources

Our articles explore leadership and performance helping decision-makers turn ideas into sustainable growth.

Blogs

Insights and Resources

Our articles explore leadership and performance helping decision-makers turn ideas into sustainable growth.

Blogs

Insights and Resources

Our articles explore leadership and performance, helping decision-makers turn ideas into sustainable business growth.

All Articles

All Articles

All Articles

Insights

Insights

Insights

Court Rulings

Court Rulings

Court Rulings

Updates

Updates

Updates

Communique

Communique

Communique

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.

23-04-2026

18

min read

Mandatory Pre-Deposit for Appeals in Indirect Tax Laws: A Barrier to Justice?

Mandatory pre-deposit has become a defining feature of indirect tax litigation, balancing revenue protection with access to appellate remedies. While the shift to a fixed statutory framework has improved procedural efficiency, it also raises concerns regarding financial barriers and effective access to justice. This insight examines the legal evolution, judicial interpretation, and practical implications of the regime.

20-04-2026

10

min read

Legal Strategy in Startup Ecosystems: Risk Mitigation and Value Maximisation from Formation to Exit

Legal structuring across the startup lifecycle extends beyond compliance to shape valuation, governance, and investor confidence. From intellectual property protection and entity selection to funding arrangements and exit mechanisms, each stage involves critical legal considerations that determine risk allocation and long-term scalability within a regulated framework.

06-04-2026

5

min read

Minority Exit under S. 66: The Supreme Court on Fairness, Valuation, and the Limits of Judicial Scrutiny

The Supreme Court’s ruling in Pannalal Bhansali v. Bharti Telecom Ltd. clarifies the contours of fairness under Section 66 of the Companies Act, 2013. It reinforces a market-based approach to valuation, affirms the permissibility of DLOM, and underscores judicial deference in the absence of oppression, marking a significant shift in minority exit jurisprudence.

05-04-2026

4

min read

NCLAT Clarifies that Accounting Set-Offs May Constitute Preferential Transactions under s. 43 of the IBC

The NCLAT clarifies that accounting set-offs may constitute preferential transactions under s. 43 of the IBC where they result in the extinguishment of receivables and confer a benefit on related parties. The ruling reinforces a substance-over-form approach and underscores that even non-cash adjustments impacting the asset pool of the corporate debtor are subject to avoidance.

12-03-2026

7

min read

Supreme Court on Value of TRC, Grandfathering & GAAR Provisions: A Shift in How Treaty Claims Are Tested

The Supreme Court’s ruling in Union of India v. Tiger Global International II Holdings re-examines how treaty claims under the India–Mauritius DTAA are tested. By permitting a prima facie avoidance enquiry despite the presence of TRCs and treaty grandfathering, the Court signals a stronger substance-over-form approach and raises important questions on the interaction between treaty certainty, GAAR, and anti-avoidance scrutiny.

24-02-2026

12

min read

The Rise of Preventive Law and the Fear of Future Harm

This essay examines where preventive law has overreached: in compliance frameworks divorced from the actual causes of contraventions, in the systematic reversal of the burden of proof, and most acutely, in the routine deployment of provisional attachment as a pre-adjudicatory punishment. The law designed to address the fear of harm has itself become an object of fear. Preventive law has emerged as the legislature's response to the complexity, scale, and pace of modern business activity and in jurisdictions like India, as a scaffolding for laws that lack organic social consensus.

01-01-2026

6

min read

Wealth Without a Will Is a Legal Vacuum

Wealth without a will does not pass in silence; it passes under statute. When intention is unexpressed, the law steps in with mechanical rules that distribute entitlement but cannot preserve context, dignity, or harmony. Intestate succession offers certainty of rule, not certainty of outcome. A will is not an assertion of control beyond death, but an assumption of responsibility during life.

19-12-2025

18

min read

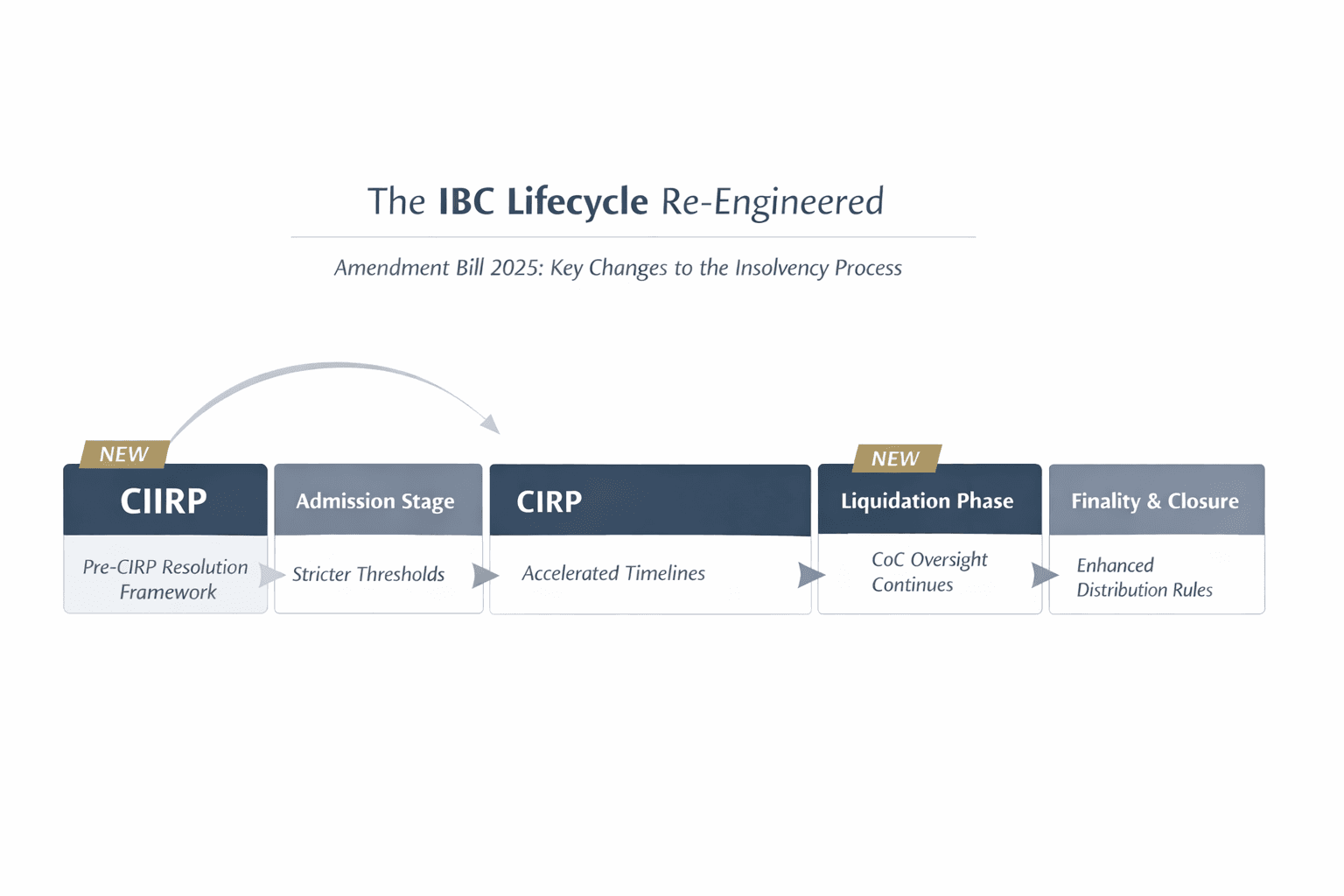

A One-Stop Shop for the IBC Amendment Bill of 2025 - Legal Update & Analysis of the IBC’s Next Turning Point

The IBC (Amendment) Bill, 2025 marks a structural recalibration of India’s insolvency regime. Beyond procedural changes, it reshapes when insolvency becomes collective, how decisional authority is exercised, and what finality means post-resolution. This Insight examines the Bill through the normative foundations of insolvency law, asking whether speed and certainty can be pursued without eroding inclusion, equality, and legitimacy.

12-11-2025

14

min read

A Bird’s Eye View of the Insolvency and Bankruptcy Framework for Personal Guarantors under the IBC with Recent Judicial Developments

A concise overview of the personal insolvency and bankruptcy framework for personal guarantors under the IBC, with key NCLAT and NCLT rulings shaping the law. This piece explains initiation, moratoriums, repayment plans, creditor rights, bankruptcy triggers, and the 2025 Amendment Bill, offering a clear snapshot of the evolving jurisprudence and its practical implications for stakeholders.

04-11-2025

15

min read

Clean Before the Crime? Attachment of Properties Acquired Before the Commission of the Scheduled Offence under the PMLA

Can property acquired before a crime be seized under the PMLA? This article examines how Indian courts have interpreted the concept of “proceeds of crime,” balancing enforcement power with constitutional safeguards, and compares global confiscation regimes to determine where the legal line truly lies.

24-09-2025

6

min read

Authority to Represent & Vakalatnamas: Juridical Foundations and Practical Issues

In litigation practice, the authority of an advocate to act is often taken for granted, with vakalatnamas and authority letters treated as routine paperwork. Yet beneath this apparent formality lies a dense body of law that determines the very legitimacy of representation. Questions of who may sign, how consent is proved, and whether a scanned signature suffices are not clerical details: they cut to the root of agency, evidence, and procedure.

28-06-2025

4

min read

Beyond Procedural Lapse: Delhi High Court Rules GST Proceedings Against Non-Existent Entity Void ab initio

The Delhi High Court in HCL Infosystems Ltd. v. Commissioner of State Tax reaffirmed that GST proceedings against a company dissolved due to amalgamation are void ab initio. The Court held that such actions are not curable under section 160 of the CGST Act, nor authorised by section 87. This judgment aligns with the Supreme Court’s ruling in Maruti Suzuki, reinforcing the principle that legal proceedings cannot be pursued against non-existent entities.

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.

23-04-2026

18

min read

Mandatory Pre-Deposit for Appeals in Indirect Tax Laws: A Barrier to Justice?

Mandatory pre-deposit has become a defining feature of indirect tax litigation, balancing revenue protection with access to appellate remedies. While the shift to a fixed statutory framework has improved procedural efficiency, it also raises concerns regarding financial barriers and effective access to justice. This insight examines the legal evolution, judicial interpretation, and practical implications of the regime.

20-04-2026

10

min read

Legal Strategy in Startup Ecosystems: Risk Mitigation and Value Maximisation from Formation to Exit

Legal structuring across the startup lifecycle extends beyond compliance to shape valuation, governance, and investor confidence. From intellectual property protection and entity selection to funding arrangements and exit mechanisms, each stage involves critical legal considerations that determine risk allocation and long-term scalability within a regulated framework.

06-04-2026

5

min read

Minority Exit under S. 66: The Supreme Court on Fairness, Valuation, and the Limits of Judicial Scrutiny

The Supreme Court’s ruling in Pannalal Bhansali v. Bharti Telecom Ltd. clarifies the contours of fairness under Section 66 of the Companies Act, 2013. It reinforces a market-based approach to valuation, affirms the permissibility of DLOM, and underscores judicial deference in the absence of oppression, marking a significant shift in minority exit jurisprudence.

05-04-2026

4

min read

NCLAT Clarifies that Accounting Set-Offs May Constitute Preferential Transactions under s. 43 of the IBC

The NCLAT clarifies that accounting set-offs may constitute preferential transactions under s. 43 of the IBC where they result in the extinguishment of receivables and confer a benefit on related parties. The ruling reinforces a substance-over-form approach and underscores that even non-cash adjustments impacting the asset pool of the corporate debtor are subject to avoidance.

12-03-2026

7

min read

Supreme Court on Value of TRC, Grandfathering & GAAR Provisions: A Shift in How Treaty Claims Are Tested

The Supreme Court’s ruling in Union of India v. Tiger Global International II Holdings re-examines how treaty claims under the India–Mauritius DTAA are tested. By permitting a prima facie avoidance enquiry despite the presence of TRCs and treaty grandfathering, the Court signals a stronger substance-over-form approach and raises important questions on the interaction between treaty certainty, GAAR, and anti-avoidance scrutiny.

24-02-2026

12

min read

The Rise of Preventive Law and the Fear of Future Harm

This essay examines where preventive law has overreached: in compliance frameworks divorced from the actual causes of contraventions, in the systematic reversal of the burden of proof, and most acutely, in the routine deployment of provisional attachment as a pre-adjudicatory punishment. The law designed to address the fear of harm has itself become an object of fear. Preventive law has emerged as the legislature's response to the complexity, scale, and pace of modern business activity and in jurisdictions like India, as a scaffolding for laws that lack organic social consensus.

01-01-2026

6

min read

Wealth Without a Will Is a Legal Vacuum

Wealth without a will does not pass in silence; it passes under statute. When intention is unexpressed, the law steps in with mechanical rules that distribute entitlement but cannot preserve context, dignity, or harmony. Intestate succession offers certainty of rule, not certainty of outcome. A will is not an assertion of control beyond death, but an assumption of responsibility during life.

19-12-2025

18

min read

A One-Stop Shop for the IBC Amendment Bill of 2025 - Legal Update & Analysis of the IBC’s Next Turning Point

The IBC (Amendment) Bill, 2025 marks a structural recalibration of India’s insolvency regime. Beyond procedural changes, it reshapes when insolvency becomes collective, how decisional authority is exercised, and what finality means post-resolution. This Insight examines the Bill through the normative foundations of insolvency law, asking whether speed and certainty can be pursued without eroding inclusion, equality, and legitimacy.

12-11-2025

14

min read

A Bird’s Eye View of the Insolvency and Bankruptcy Framework for Personal Guarantors under the IBC with Recent Judicial Developments

A concise overview of the personal insolvency and bankruptcy framework for personal guarantors under the IBC, with key NCLAT and NCLT rulings shaping the law. This piece explains initiation, moratoriums, repayment plans, creditor rights, bankruptcy triggers, and the 2025 Amendment Bill, offering a clear snapshot of the evolving jurisprudence and its practical implications for stakeholders.

04-11-2025

15

min read

Clean Before the Crime? Attachment of Properties Acquired Before the Commission of the Scheduled Offence under the PMLA

Can property acquired before a crime be seized under the PMLA? This article examines how Indian courts have interpreted the concept of “proceeds of crime,” balancing enforcement power with constitutional safeguards, and compares global confiscation regimes to determine where the legal line truly lies.

24-09-2025

6

min read

Authority to Represent & Vakalatnamas: Juridical Foundations and Practical Issues

In litigation practice, the authority of an advocate to act is often taken for granted, with vakalatnamas and authority letters treated as routine paperwork. Yet beneath this apparent formality lies a dense body of law that determines the very legitimacy of representation. Questions of who may sign, how consent is proved, and whether a scanned signature suffices are not clerical details: they cut to the root of agency, evidence, and procedure.

28-06-2025

4

min read

Beyond Procedural Lapse: Delhi High Court Rules GST Proceedings Against Non-Existent Entity Void ab initio

The Delhi High Court in HCL Infosystems Ltd. v. Commissioner of State Tax reaffirmed that GST proceedings against a company dissolved due to amalgamation are void ab initio. The Court held that such actions are not curable under section 160 of the CGST Act, nor authorised by section 87. This judgment aligns with the Supreme Court’s ruling in Maruti Suzuki, reinforcing the principle that legal proceedings cannot be pursued against non-existent entities.

27-06-2025

4

min read

[Patna HC] Appellate Authorities Under GST Must Decide Appeals on Merits, Not Technicalities

In M/s Silverline v. State of Bihar, the Patna High Court held that GST appellate authorities must adjudicate appeals on their merits, even in cases of procedural lapses or absence of supporting documents. The Court ruled that dismissal for non-prosecution without a merit-based inquiry violates statutory duty under s. 107 of the Bihar GST Act reinforces the importance of reasoned, fair, and substantive appellate decisions.