The Central Board of Direct Taxes (‘CBDT’), the authority on direct taxes in the country, released the Income Tax (Fifth Amendment) Rules, 2023 (‘IT Rules of 2023’) thereby bringing in an elaborate Rule 133 to the Income Tax Rules, 1962, in order to streamline and standardize the calculation and reporting of winnings from online gaming. The IT Rules of 2023 prescribes specific formulae including formula for calculating the net winnings from online games in one financial year that would then be liable to a 30% Tax Deduction at Source (‘TDS’).

Rule 133 has been introduced in the backdrop of the amendments made in this regard by the Finance Bill, 2023. The two most important insertions made in the Income Tax Act of 1961 by the Finance Bill, 2023 are:

Section 115BBJ to provide for 30% tax on net winnings from online games and

Section 194BA to impose an obligation to withhold tax on any person responsible for paying any income by way of winnings from any online game during the financial year at the prescribed rates in force (Reference: Finance Bill, 2023, Bill No. 17 of 2023, https://www.indiabudget.gov.in/doc/Finance_Bill.pdf)

Hence, the IT Rules of 2023, in fact, have been inducted to give meaning, purpose and effect to Section 194BA of the Income Tax Act of 1961.

The IT Rules of 2023 also lay down the definition of certain terms and concepts that were undefined earlier. Additionally, online gaming platforms are not required to deduct TDS on withdrawals of an amount less than Rs. 100 per month, provided that such winnings do not exceed this limit in the same month or the subsequent month or at the end of the financial year. However, in order to qualify for this concession, the online gaming platform would have to take on the responsibility of paying the difference, if the balance in the user account is insufficient to meet the tax liability at the time of such deduction.

TDS on winnings of online gamers were to be deducted from 01.07.2023, however, the government revised the effective date to 01.04.2023. This was done to align with the end and beginning of the financial year and consequentially, to avoid substantial operational difficulties for not just the online gaming operators but also for over a million gamers in India.

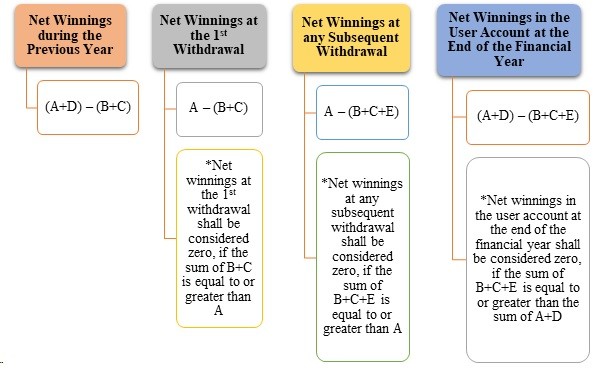

The Pool of Calculations

Before diving into the pool of formulae laid down by Rule 133 of the IT Rules of 2023, let’s assume as follows:

A: Amount withdrawn from the user account.

B: Aggregate amount of non-taxable deposit made in the user account.

C: Opening balance of the user account at the beginning of the financial year.

D: Closing balance of the user account at the end of the financial year.

E: Net winnings comprising of earlier withdrawals if tax has been deducted on it.

One of the key takeaways from the above framework is that the amount of money deposited by the online gamer in their user account will not be subject to tax. Further, losses suffered by players during a financial year will be adjusted while computing net winnings.

Removal of Difficulties

By way of two explanations, the IT Rules of 2023 clear the confusion with regard:

to multiple user accounts of the same individual,

taxable deposit and non-taxable deposit,

payments in cash and kind in the form of goodies or merchandise,

referral bonus and incentives, etc.

Generally, a deposit made in the user account will not be subject to tax and would be called non-taxable deposit. However, this non-taxable deposit must be from an amount that has already been taxed before it was deposited in the user account and includes borrowed money. On the other hand, bonus, referral bonus, incentives, etc. are provided by gaming platforms and are non-taxable as long as they can be used to play the game and not for withdrawals. However, if these amounts are recharacterized so as to make them eligible for withdrawals by the user, then such amounts shall be called taxable deposits.

In the event that a gamer operates multiple accounts on the same gaming platform, each such user account, regardless of its name, shall be considered for calculating the net winnings. However, the transfer from one user account to another user account, maintained with the same online gaming intermediary, by the same user shall not be considered as withdrawal or deposit (Reference:Central Board of Direct Taxes, (THE GAZETTE OF INDIA : EXTRAORDINARY) (2023), https://incometaxindia.gov.in/communications/notification/notification-28-2023.pdf).

It has been provided that if a tax deductor uses multiple platforms and it is technologically possible for him to integrate various user accounts across several platforms, they may determine the amount of tax that must be deducted for each platform. However, even in such a situation, all user accounts across the same platform must be necessarily taken into consideration while computing the net winnings as per Rule 133.

Where the winning of an online game involves a reward which is partly in cash and partly in kind, and the part in cash is insufficient to meet the TDS liability thereon, the tax deductor shall release the net winnings in kind only after collecting the proof of payment of tax on it. Further, the valuation of winnings in kind would be based on fair market value (‘FMV’) except when the online gaming platform has purchased the winnings before providing it to the user or has itself manufactured such winnings in kind.

Conclusion

It is evident that we are beyond the point of return in terms of debates and discussions regarding regulations in the online gaming sector in India. Experts on the topic have opined that such changes in the gaming industry have, without a doubt, brought clarity to the tax regime and plugged certain loopholes. However, they contemplate a dip in online gaming activities as a result of such amendments.

When it comes to taxation, both the tax rate as well as the taxable value are of key importance. Countries around the world have adopted different rates of taxation as well as models in order to strike a balance between having a robust taxation regime for the sector given its popularity and addressing the need for social regulation. (Reference: Online Gaming in India -The Taxation Quandary (March 2023), Policy Watch India Foundation,https://primuspartners.in/docs/documents/ltOAZaeMVPLOkrH54fDe.pdf)

Money laundering and addiction are the two largest known monsters that the world of online gaming has created. While addiction is not a criminal offence, money laundering through online gaming platforms has been making headlines lately, with raids at over 20 locations in about 5 Indian states totalling to a possible scam of Rs. 4000 crores. With the onset of new guidelines and tax laws in this relation, we can only wait and see whether the experts are correct about a dip in the gaming industry.

*Authored by Srishty Jaura, Advocate at Metalegal Advocates. The views are personal and do not constitute legal opinion. *

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.