Introduction

Taxes are the main source of government income, yet a large part of the economy remains undocumented. Tax amnesty programs are a short-term solution to address tax non-compliance, providing immediate revenue recovery and enhancing long-term compliance.

Tax amnesty schemes are government initiatives that allow taxpayers to disclose previously unreported income or assets or resolve tax disputes by paying a reduced penalty or tax amount. These schemes are designed to encourage compliance by allowing individuals and businesses to regularize their tax affairs, thereby avoiding the harsher consequences of penalties, interest, and legal actions. These measures allow taxpayers who have evaded taxes or failed to meet obligations to settle dues more leniently, ensuring legal and financial compliance.

In the context of modern tax administration, tax amnesty schemes significantly reduce the backlog of tax disputes and promote voluntary compliance. They efficiently resolve disputes between taxpayers and tax authorities, often providing a quicker, more cost-effective resolution than lengthy litigation processes. These schemes help to foster a more cooperative environment between taxpayers and the government, encouraging those who may have previously avoided tax compliance to come forward and disclose their income or assets. By offering reduced penalties or immunity from prosecution, the schemes create a less intimidating path to compliance, benefiting the taxpayers and the government.

Objective of Amnesty Schemes

The core objectives of tax amnesty schemes are to reduce tax litigation, broaden the tax base, promote voluntary compliance, and generate quick revenue for the government. By allowing taxpayers to resolve their issues without facing prolonged legal battles, these schemes significantly reduce the burden on the judicial system. Additionally, they encourage individuals and businesses to disclose previously hidden income, thus expanding the tax base and increasing government revenue. Furthermore, by providing an easier and less punitive means of coming into compliance, these schemes incentivize taxpayers to regularly meet their tax obligations, which ultimately strengthens the overall tax system.

However, while tax amnesty schemes offer a range of benefits in the short term, their long-term effectiveness remains debatable. Some argue that such schemes only provide temporary relief, failing to address the underlying issues of tax evasion and non-compliance. The concern is that they may inadvertently foster a culture of waiting for future amnesty programs, with taxpayers postponing their obligations, hoping that future schemes will offer similar leniency. As a result, while these schemes may help the government collect revenue quickly, they could also encourage a cycle of non-compliance that undermines establishing a sustainable, long-term tax culture. Thus, the true challenge lies in determining whether tax amnesty schemes can lead to enduring tax discipline or merely serve as stopgap measures that fail to address deeper issues in the tax system.

Historical Evolution of Tax Amnesty Schemes in India

The evolution of tax amnesty schemes in India can be classified into three phases: (i) Early tax amnesty programs, (ii) Mid-evolution and (iii) Recent Schemes. These phases reflect the government’s efforts to address tax evasion, broaden its tax base, and generate revenue while encouraging compliance. Introduced over the decades, these schemes have been tools for bringing undisclosed income into the formal economy. However, these schemes have encountered both success and criticism, reflecting the complexities of tax administration and policy design.

Early Tax Amnesty Programs

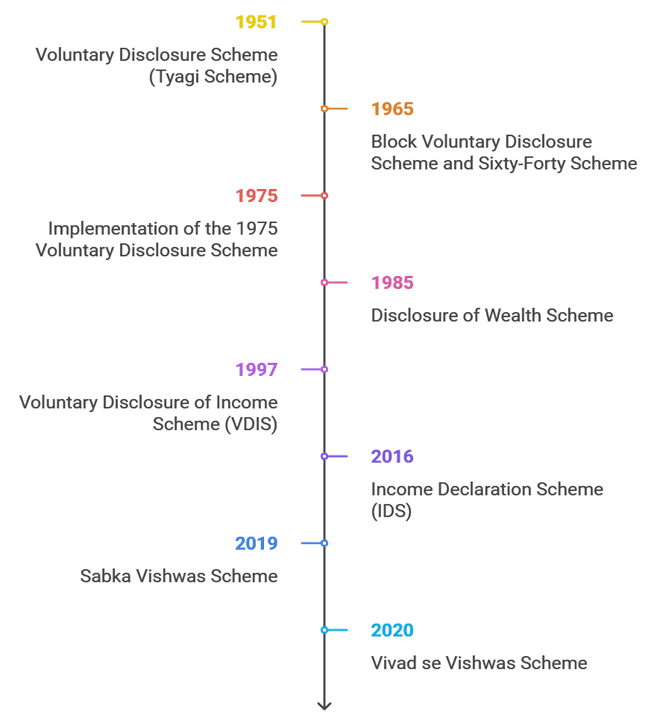

In India, the tax amnesty scheme began in 1951 with the introduction of the Voluntary Disclosure Scheme (‘VDS’), popularly known as the Tyagi Scheme. This initiative aimed to encourage taxpayers to declare concealed income with assurances of immunity from prosecution. Although the scheme resulted in Rs.20 crore in tax collection and Rs.70 crore in disclosed income, it failed to win the confidence of taxpayers. Many were sceptical of the government’s intentions, and the confidentiality promised resulted in limited participation and rendered the scheme ineffective.

In 1965, the government introduced the ‘Block Voluntary Disclosure Scheme’ (‘BVDS’) and the ‘Sixty-Forty Scheme’, which attempted to address income tax evasion through innovative approaches. The BVDS treated disclosed income as separate from regular income. At the same time, the Sixty-Forty Scheme imposed a flat tax rate of 60% on disclosed income, with provisions for confidentiality and instalment-based payment. These schemes collectively yielded significant revenue, with Rs.145 crore disclosed, Rs. 20 crore collected in taxes under the BVDS, and Rs.52 crore disclosed with Rs.30 crore collected under the Sixty-Forty Scheme. However, criticisms emerged regarding the flat tax rate, disregarding income slabs and limiting the schemes’ appeal among taxpayers.

The 1975 Voluntary Disclosure Scheme marked a shift towards more nuanced tax policies by introducing a slab-rate taxation model. Taxpayers declaring income up to Rs.25,000 were taxed at 25%, while those disclosing larger amounts were taxed at higher rates, with a maximum of 60% for income above Rs.50,000. This progressive structure garnered a better response, resulting in Rs.744 crore in disclosures and Rs.241 crore in tax collection. The scheme’s structure and relatively higher participation rates highlighted the potential for equitable tax amnesty programs to achieve success.

Mid-Evolution Period

In 1985, the Disclosure of Wealth Scheme extended the amnesty approach to wealth tax. This scheme taxed disclosed wealth at notified rates and aimed to address the issue of undisclosed assets. However, its impact remained limited as it failed to incentivize widespread participation.

A significant milestone in India’s history of tax amnesty was the Voluntary Disclosure of Income Scheme, 1997 (‘VDIS’). Launched under the Finance Act, 1997, the scheme allowed individuals to declare undisclosed income from prior years without legal repercussions. Taxpayers could disclose income omitted from returns, escaped assessment, or remained undeclared under s. 139 of the Income-tax Act, 1961 (‘IT Act’). Tax rates under this scheme were fixed at 30% for individuals and 35% for companies and firms. The scheme was immensely successful, leading to disclosures worth Rs.33,000 crore and tax collection of Rs.9,584 crore. Notably, 77.5% of the collected taxes were shared with state governments, highlighting its financial significance.

Despite its apparent success, the VDIS faced substantial criticism. The Comptroller and Auditor General (CAG) labelled the scheme a ‘fraud on honest taxpayers’, as it was perceived to reward those who evaded taxes at the expense of compliant citizens. The Supreme Court also expressed concerns about the scheme’s ethical implications and advised against similar policies in the future. These critiques highlight the tension between the short-term revenue benefits of amnesty schemes and their potential to erode long-term compliance.

Recent Amnesty Programs

Recently, the government has reintroduced tax amnesty schemes with renewed objectives and strategies. The Income Declaration Scheme, 2016 (‘IDS’) was a notable example, introduced as part of the Union Budget. This scheme aimed to address black money by encouraging taxpayers to declare undisclosed income through an online platform, a first for such programs. Taxation under IDS included a 30% tax rate, a 7.5% surcharge, and a 7.5% penalty on declared income, reflecting the government’s focus on penalizing evasion while facilitating compliance. While the scheme brought some success, its impact on curbing systemic tax evasion remained debatable.

The Sabka Vishwas Scheme, 2019, introduced during the Goods and Service Tax ('GST') regime, focused on resolving legacy disputes related to service tax, central excise, and other subsumed taxes. By allowing taxpayers to pay only the outstanding tax amount without penalties or interest, the scheme resolved over 1,89,000 cases. It played a pivotal role in easing the transition to GST and reducing litigation.

The Vivad se Vishwas Scheme, 2020 (‘VSVS 2020’), a Hindi term meaning ‘From Dispute to Trust’, aimed to resolve pending direct tax disputes. At the time of its launch, India faced a staggering 4.83 lakh pending tax cases involving over Rs.9,000 crore in disputed taxes. VSVS 2020 allowed taxpayers to settle disputes by paying only the tax amount, with waivers on interest and penalties. By March 2021, nearly 90% of disputed taxes were settled, solidifying the scheme’s success as a dispute resolution mechanism. However, critics questioned whether such schemes inadvertently encouraged taxpayers to delay compliance in anticipation of future amnesties.

Thus, India's evolution of tax amnesty schemes points out their dual nature. While they have proven effective in generating revenue and resolving disputes, they have also been criticized for rewarding non-compliance. However, each scheme indubitably offers valuable insights into how tax policies can be balanced to address immediate needs without compromising long-term goals of fairness and systemic adherence.

Current Amnesty Schemes: A Closer Look

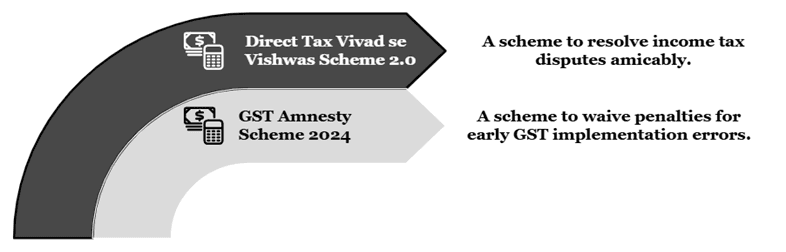

Over time, tax amnesty schemes in India have become more focused on solving disputes and encouraging taxpayers to comply. Recent programs, like the Direct Tax VSVS 2.0 (2024) (‘DT VSVS 2024’)and the GST Amnesty Scheme (2024), aim to make it easier for taxpayers to settle issues while building trust between taxpayers and the government. In this section, we will explore the recent tax amnesty schemes introduced by the government, designed to address ongoing tax disputes and encourage voluntary compliance.

DT VSVS 2024

The DT VSVS 2024 was announced in the Union Budget 2024 and is a significant initiative to resolve pending tax disputes swiftly and cost-effectively. Building upon the framework of the VSVS 2020, this updated version seeks to address the backlog of tax litigation under the IT Act by offering taxpayers an opportunity to settle disputes amicably. Its design not only simplifies the resolution process but also encourages voluntary compliance, contributing to a more efficient tax administration system.

Provisions and Scope

The DT VSVS 2024 covers a wide range of pending disputes as of 22.07.2024. These include appeals, writ petitions, and special leave petitions (SLPs) filed by taxpayers or the Income Tax Department (ITD) at various appellate levels, including the Income Tax Appellate Tribunal (ITAT), High Courts, and the Supreme Court. Additionally, the scheme encompasses objections pending before the Dispute Resolution Panel (DRP), where directions have yet to be issued, as well as revision applications filed under s. 264 of the IT Act. Disputes concerning Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) are also eligible, making the scheme highly inclusive in its scope.

However, certain disputes are explicitly excluded, such as cases involving search assessments, undisclosed foreign assets or income, and prosecutions under laws like the Prevention of Money Laundering Act, 2002 or the Prohibition of Benami Transactions Act, 1988. These exclusions reflect the government’s intention to reserve the benefits of the scheme for less complex cases and straightforward tax arrears.

Settlement Process and Payments

The scheme outlines a structured process for settlement. Taxpayers are required to submit a declaration to a Designated Authority (‘DA’), who will determine the amount payable within 15 days of receiving the application. Once the taxpayer receives the DA’s certificate, the amount must be paid within the next 15 days, along with proof of withdrawal of any pending appeals or legal petitions. Once a dispute is settled under the scheme, it cannot be reopened in subsequent proceedings, ensuring finality for taxpayers and authorities.

The payment mechanism under the scheme is designed to incentivize early settlement. Taxpayers settling disputes before 31.12.2024 must pay 100% of the disputed tax amount for new cases or 110% for disputes eligible under the VSVS 2020 but remain unresolved. After this deadline, the payable amount increases to 110% for new cases and 120% for unresolved cases under the earlier scheme. Taxpayers can settle disputes involving penalties, interest, or fees by paying a reduced percentage of the disputed amount. These provisions encourage timely compliance and offer financial relief to taxpayers.

Comparison with the VSVS 2020

The DT VSVS 2024 closely mirrors its predecessor in structure but introduces key changes to broaden its applicability and address prior shortcomings. Unlike the VSVS 2020, which excluded certain cases involving search assessments exceeding Rs.5 crore, the DT VSVS 2024 entirely excludes search-related disputes, regardless of the amount involved. This change reflects a more cautious approach to high-value or complex cases.

Another distinction lies in the treatment of appeals awaiting filing deadlines. While the 2020 VSVS Scheme explicitly included disputes where the time to file an appeal had not expired, the DT VSVS 2024 does not address such cases, potentially creating ambiguity for taxpayers. Additionally, the DT VSVS 2024 allows taxpayers with disputes predating the 2020 VSVS Scheme to participate, making it more inclusive and attractive to a broader audience.

Impact and Limitations

The scheme is poised to significantly impact the economy by reducing the burden of pending tax litigation. It offers a practical and time-bound mechanism for resolving disputes, freeing up resources for both taxpayers and the judiciary. This not only improves the ease of doing business in India but also enhances taxpayer confidence in the fairness and efficiency of the tax system.

However, the scheme is not without its limitations. Excluding search cases may limit its utility in resolving contentious and high-value disputes. Additionally, the absence of clear provisions for appeals awaiting filing deadlines could discourage participation from certain taxpayers. Critics have also expressed concerns about the potential for frequent amnesty schemes to undermine regular compliance, as taxpayers might delay their obligations in anticipation of future relief measures.

Overall, the DT VSVS 2024 is a commendable step toward addressing India’s longstanding tax litigation challenges. Providing a simplified and inclusive framework offers taxpayers a valuable opportunity to resolve disputes and achieve compliance. However, its success will depend on the extent of taxpayer participation and its ability to strike a balance between immediate revenue gains and fostering a culture of long-term compliance. While the scheme has limitations, it represents a crucial step in the government’s broader efforts to streamline tax administration and build a more cooperative compliance framework.

GST Amnesty Scheme (2024)

The GST Amnesty Scheme (2024) is a targeted initiative introduced to provide relief to taxpayers who faced difficulties during the early years of Goods and Services Tax (GST) implementation. When GST was launched in July 2017, it replaced a fragmented indirect tax system with a unified framework. While this shift promised to streamline tax compliance, the initial implementation phase was far from smooth. Frequent notifications, technical glitches, and a lack of clarity on procedural aspects created significant challenges for taxpayers and businesses alike. These transitional issues led to widespread errors, delayed filings, and unintentional non-compliance. To address these concerns, the GST Amnesty Scheme (2024) aims to ease the burden on taxpayers by waiving penalties and interest for tax liabilities during the initial GST period, covering the Financial Years 2017-18 to 2019-20.

Provisions Under Section 128A of the Central Goods and Services Tax Act, 2017 (‘CGST Act’)

The scheme is codified through s. 128A of the CGST Act, 2017, and came into effect on 01.11.2024. It provides taxpayers with an opportunity to settle their outstanding tax liabilities from the initial GST years by paying the full tax amount without additional penalties or interest. To avail themselves of the scheme's benefits, taxpayers must make these payments by 31.03.2025.

To streamline the application process, r. 164 was introduced under the CGST Rules, 2017, which lays down the procedural framework for applying under the scheme, including the forms taxpayers must submit to seek waivers. The scheme is accessible to taxpayers who have received Show Cause Notices or tax demands, have pending appeals or revisions before appellate authorities, or whose tax liabilities have been reassessed. However, it is important to note that the scheme excludes certain cases, such as erroneous refunds, undeclared foreign income, or criminal proceedings involving money laundering and tax evasion. By narrowing its scope, the scheme focuses on resolving genuine compliance issues arising from technical and procedural challenges during the GST transition.

Addressing Challenges and Ambiguities

While the GST Amnesty Scheme (2024) is a step in the right direction, it is not without its challenges. Procedural ambiguities, such as unclear timelines for applications and the documentation required for waiver approvals, can create hurdles for taxpayers seeking relief. Moreover, repeated amnesty programs have sparked debates about their potential to create moral hazards. These schemes might encourage non-compliance by offering periodic relief, as taxpayers could perceive amnesties as a predictable and lenient fallback option. This perception can undermine the overall integrity of the GST framework by rewarding habitual defaulters while penalizing those who consistently comply with tax regulations.

Benefits and Long-Term Impact

Despite these concerns, the GST Amnesty Scheme (2024) offers significant benefits. It helps taxpayers rectify past mistakes without facing the financial burden of steep penalties and interest, making compliance more achievable. Businesses that lost GST registrations due to early non-compliance can re-register under this scheme and clear pending returns. The scheme reduces pending litigation and improves overall tax compliance for the government, creating a more predictable and stable revenue stream.

The GST Amnesty Scheme (2024) promotes a more cooperative tax environment by addressing transitional challenges and simplifying the resolution of past disputes. However, to ensure long-term success, such initiatives must be paired with robust compliance measures, clear guidelines, and taxpayer education to prevent reliance on future amnesties. The scheme is a crucial step toward resolving legacy issues from GST’s early years, fostering trust between taxpayers and authorities, and strengthening the efficiency of the tax system in India.

Constitutionality of Amnesty Schemes

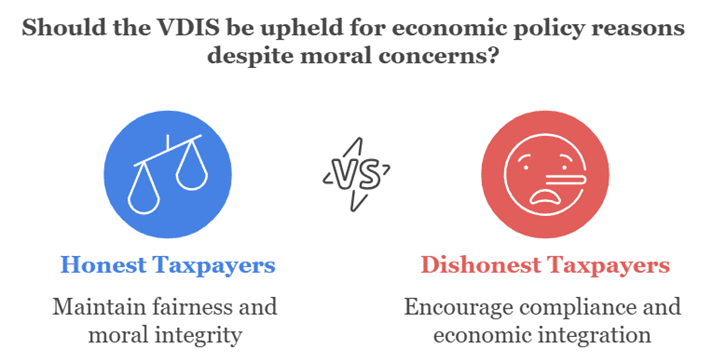

In the landmark case of The All-India Federation of Tax Practitioners & Another v. Union of India & Others[i], the constitutional validity of the Voluntary Disclosure of Income Scheme, 1997 (VDIS), enacted under ss. 64 to 78 of the Finance Act, 1997, was called into question. The petitioners, comprising a federation of tax practitioners and a practising advocate, contended that the scheme was arbitrary, violative of a. 14 of the Constitution of India (‘Constitution’), and contrary to public morality. They argued that it unjustly rewarded dishonest taxpayers, allowing them to declare unaccounted income at a concessional tax rate of 30% while offering immunity from prosecution. Conversely, honest taxpayers, who had discharged their obligations at higher rates, were placed at a comparative disadvantage, undermining society's moral fabric.

The Bombay High Court, while dismissing the petition, upheld the constitutionality of VDIS, observing that economic legislation is an area within the exclusive domain of the legislature, and courts should exercise restraint in substituting their judgment for legislative policy. The Bombay High Court emphasized that unearthing black money is a pressing and complex issue that requires pragmatic solutions. It held that VDIS was a bona fide policy decision aimed at mobilizing unaccounted wealth and channelling it into the formal economy. The classification between honest and dishonest taxpayers was found to have a rational nexus with the object sought to be achieved, namely, reducing black money circulation and enhancing compliance.

Addressing the alleged violation of a. 14 of the Constitution, the Court referred to the established principle that laws concerning economic matters are entitled to greater latitude in judicial review. It reiterated that legislation directed at resolving practical economic problems, even if imperfect, cannot be struck down merely on the grounds of inequities or potential for abuse. The Court noted that granting immunities and incentives to tax evaders was a legitimate method to address endemic tax evasion and unaccounted wealth.

Further, the Court noted that while the moral argument advanced by the petitioners was valid, it could not override the constitutionality of the scheme. The judiciary’s role, it held, is limited to ensuring that legislation does not violate constitutional principles; it is not for the courts to judge the wisdom, fairness, or morality of economic policies enacted by Parliament. The Court also remarked that expert committee reports, which had previously advised against such schemes, were not binding on the legislature, which retains the discretion to formulate policies based on prevailing social and economic conditions.

The Bombay High Court's ruling was challenged before the Supreme Court in All India Federation Of Tax Practitioners And Another v. Union Of India And Others[ii]. However, the Supreme Court upheld the decision of the High Court, concurring with its reasoning, which comprehensively addressed the constitutional validity of VDIS.

Therefore, the Court held that VDIS was neither arbitrary nor irrational. The legislative measures, though controversial, were necessary to address the parallel economy and mobilize resources for public benefit. The petition was accordingly dismissed, with the Court reiterating that such policy decisions fall squarely within the legislative domain and should not be interfered with by the judiciary in the absence of clear constitutional infirmities.

Challenges and Criticism

While tax amnesty schemes in India have successfully generated revenue and resolved disputes, they are not without their challenges and criticisms. Several issues arise in these schemes' implementation and long-term impact, which hinder their effectiveness in fostering sustainable tax compliance. Some of the key challenges include:

Moral Hazard and Encouragement of Non-Compliance: One of the most significant criticisms of tax amnesty schemes is that they may create a culture of non-compliance. Taxpayers may delay meeting their obligations, anticipating future amnesties that offer leniency, thereby undermining the integrity of the tax system. The cyclical nature of these schemes may encourage individuals and businesses to withhold income or assets until a future amnesty is announced.

Inequity Between Compliant and Non-Compliant Taxpayers: Amnesty programs often reward individuals who have evaded taxes, offering them a chance to settle their dues at a reduced cost, which can be seen as unfair to those who have been consistently compliant. This perception can affect public trust in the tax system, as it appears to incentivize dishonesty while penalizing those who have adhered to tax obligations.

Limited Scope and Exclusions: Many amnesty schemes come with exclusions, such as the non-eligibility of disputes involving high-value tax evasion cases, search assessments, or foreign assets. These exclusions can leave significant loopholes, allowing some taxpayers to escape the consequences of serious tax evasion while others, whose cases are included, may face financial burdens in order to comply.

Short-Term Focus and Long-Term Sustainability: While tax amnesty schemes provide quick revenue for the government, they often fail to address the underlying systemic issues of tax evasion and poor compliance. Critics argue that these schemes offer only temporary relief and do little to build a robust and sustainable culture of tax compliance in the long run.

Increased Litigation and Complexity in Application: Amnesty schemes often introduce legal complexities and administrative hurdles despite their intent to resolve disputes. The numerous forms, documentation requirements, and varying deadlines can create confusion and delays in the settlement process. This not only reduces the effectiveness of the schemes but can also discourage taxpayers from participating.

Risk of Repeated Amnesty Programs: The frequent introduction of tax amnesty schemes may signal to taxpayers that they can continue to evade taxes and wait for the next amnesty program. This could undermine the principles of tax fairness and compliance, making it difficult for authorities to establish a solid, long-term framework for taxation.

Overall, while tax amnesty schemes can improve short-term tax compliance and generate revenue, their challenges underscore the need for a balanced approach that ensures both immediate and long-term solutions to tax evasion and non-compliance.

Conclusion

Tax amnesty schemes in India are designed to reduce tax litigation, expand the tax base, and generate immediate revenue by encouraging taxpayers to disclose previously hidden income voluntarily. These programs provide a simplified mechanism for resolving tax disputes without penalties or legal repercussions, easing the burden on the judiciary and promoting compliance. Schemes like the VDIS and the VSVS, 2020, have successfully mobilized significant revenue and resolved disputes. Still, they have also faced criticism for rewarding non-compliance, potentially undermining long-term tax discipline.

The recent iterations, such as the DT VSVS 2024 and the GST Amnesty Scheme (2024), aim to address specific challenges like legacy disputes and compliance gaps during the GST transition. While these schemes reduce litigation and offer relief to taxpayers, they raise concerns about their potential to encourage habitual non-compliance. Their success depends on balancing short-term revenue goals with fostering sustainable tax compliance, supported by robust measures to prevent misuse and promote fairness in the tax system.

End Notes

[i][1997 SCC OnLine Bom 301.

[ii] (1998) 2 Supreme Court Cases 161.

Authored by Ritik Kumar Jha, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions.

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.