The emergence of the digital economy and its consequential impact on the conventional tax systems led the OECD to address the issue of BEPS, which refers to the strategies Multinational Enterprises (‘MNEs’) used to reduce their tax liabilities by shifting profits to law-tax jurisdictions. As a participant in the OECD Inclusive Framework on BEPS, India has instituted various legislative modifications to harmonize its tax statutes with the BEPS action plans, stressing its commitment to international standards. This article examines the specific amendments made in the Indian tax laws in response to the BEPS action plans and their impact on the Indian taxation landscape.

For more on the 15 BEPS action plans, please refer to our Insight titled ‘BEPS Actions – A Concise Summary’.

Introduction

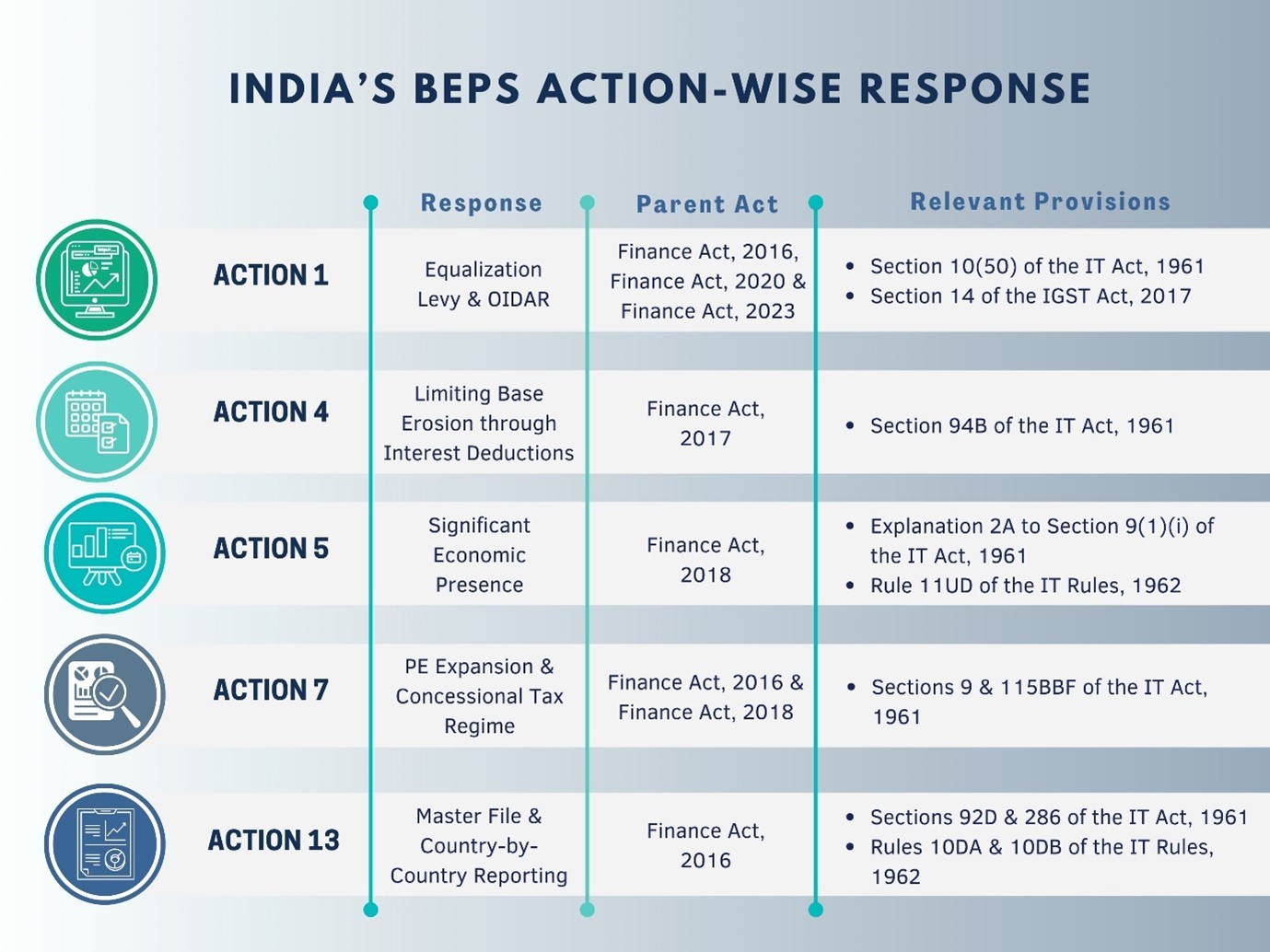

India has been proactively implementing changes suggested through international consensus under the Base Erosion and Profit Shifting (‘BEPS’) project. Over the years, starting from 2015, several amendments have been brought into the Income-tax Act, 1961 (‘IT Act’) in provisions concerning the taxation of permanent establishments, digital transactions, transfer pricing, and tax treaties. This article is an Action-wise analytical compendium of such amendments and changes and attempts to give a summary of the implementation of the BEPS thought in the Indian domestic tax law framework.

Action Plan 1: Taxation of Digital Transactions

One of the key challenges the digital economy poses is the allocation of taxing rights between the source and residence countries of income. BEPS Action 1 aimed to address this challenge by proposing various options to tax the digital economy, including a new nexus rule based on the significant economic presence (‘SEP’), a withholding tax on certain types of digital transactions, an equalization levy on gross revenues generated from digital activities, and implementing a value-added tax (‘VAT’) on the online information database access and retrieval (‘OIDAR’) services. Including implementing a withholding tax, taxing economic presence, and implementing a value-added tax on transaction value.

Equalisation Levy

In 2016, India adopted the equalisation levy *vide *Chapter VIII of the Finance Act, 2016 and substantially extended its scope *vide *the Finance Act, 2020. The equalization levy is a presumptive tax imposed by the Indian government on certain online transactions or services provided by non-resident entities to Indian residents or non-residents having a permanent establishment (‘PE’) in India. The objective of the equalization levy is to ensure a level playing field between resident and non-resident service providers and to prevent the erosion of the Indian tax base.

The equalization levy has two components: the first one applies to specified services, such as online advertising, and the second one applies to e-commerce supply or services, such as online sale of goods or services, online provision of software, or online platform services. The first component is levied at the rate of 6% on the amount of consideration received or receivable by the non-resident service provider if it exceeds Rs. 1 lakh in a financial year. The second component is levied at the rate of 2% on the amount of consideration received or receivable by the non-resident e-commerce operator, without any threshold limit. The person making the payment to the non-resident entity is responsible for deducting and depositing the equalization levy to the government. The income subject to the equalization levy is exempt from income tax under s. 10(50) of the IT Act.

While the equalization levy was initially introduced to tax digital transactions, the Finance Act, 2020 expanded its scope to cover non-resident e-commerce operators as well. This amendment reflects India’s efforts to ensure fair taxation of digital businesses in India and to align with global initiatives to address the taxation challenges posed by the digital economy.

Virtual PE

Another option to tax the digital economy is to introduce a new nexus rule based on SEP also known as virtual PE. This option allows the source country to tax the profits of a non-resident entity that has a substantial digital presence in its territory, even if it does not have a physical PE there. The virtual PE concept is based on the idea that the continuous and systematic interaction of a non-resident entity with the customers or users in the source country through digital means creates a taxable nexus, regardless of the degree of human intervention or automation involved in the delivery of the services. The virtual PE approach has been endorsed by countries such as Israel, Nigeria, and South Africa, but it also faces some practical and conceptual difficulties such as defining the criteria for determining the existence and attribution of profits to a virtual PE, ensuring the compatibility with the existing tax treaties, and avoiding double taxation or non-taxation of the same income. Though this concept has not been expressly defined in the Indian statutes, the concept of SEP was introduced which is discussed later in this article.

OIDAR

A third option to tax the digital economy is to impose VAT or goods and services tax (‘GST’) on OIDAR services that are defined as services delivered through the internet or an electronic network, and that are essentially automated and impossible to ensure without the use of information technology such as advertising, cloud computing, e-books, music, games, software, and streaming services. VAT or GST on OIDAR services is levied on the consumption of such services in the destination country, regardless of the location or residence of the service provider. This option aims to ensure that the VAT or GST is paid in the country where the value is created and consumed and to avoid the distortion of competition between domestic and foreign service providers. This option has been widely adopted by many countries such as the European Union, Australia, Japan, South Korea, and Singapore. India implemented changes to the GST OIDAR rules in the Finance Act, 2023 effective from 01.10.2023[i].

The Finance Act, 2023 has broadened the scope of OIDAR services under the GST regime by eliminating the terms ‘minimal human intervention’ and ‘essentially automated’ from its definition. Consequently, any service delivered via information technology or an electronic network, which cannot be ensured without information technology, is now considered an OIDAR service. It also redefines ‘non-taxable online recipient’ to include GST-registered individuals who register solely to claim TDS benefits, thereby classifying them as B2C customers for non-resident sellers. Furthermore, the Finance Act, 2023 imposes penalties on marketplaces that facilitate sales of goods or services by vendors in India who are not GST-registered, if they are required to do so, thereby shifting the responsibility of assessing GST registration obligations onto the marketplaces.

Action 4: Limiting Base Erosion through Interest Deductions

BEPS Action 4 aimed to limit the base erosion through interest deductions and other financial payments, which are often used by MNEs to shift profits to low-tax jurisdictions. The action plan recommended a three-tiered approach to limit the net interest deductions of an entity or a group, consisting of a fixed ratio rule, a group ratio rule, and targeted rules. India, as a member of the Inclusive Framework (‘IF’) on BEPS, has adopted some of these recommendations under s. 94B of the IT Act that became enforceable from 01.04.2018 introducing the thin capitalisation rules.

These rules apply to Indian companies or PEs of foreign companies that pay interest or similar payments to a non-resident-associated enterprise or a PE of a non-resident-associated enterprise. The primary objective is to prevent excessive interest deductions by entities with a disproportionate amount of debt in comparison to equity. The thin capitalisation rules operate as follows:

(i) The rules are applicable when the interest or similar payments exceed Rs. 1 crore in a financial year.

(ii) The interest deduction is capped at 30% of the earnings before interest, taxes, depreciation, amortization (‘EBITDA’) of the entity, or the actual interest paid – whichever is lower.

(iii) Any excess interest disallowed under these rules can be carried forward for 8 years and deducted within the same limit.

(iv) The rules do not apply to interest paid to banks or financial institutions unless there is a guarantee or an implicit or explicit arrangement by an associated enterprise.

(v) Banking or insurance companies are exempt from these rules.

Action 5: Significant Economic Presence

BEPS Action 5 aimed to address harmful tax practices frequently exploited by MNEs to take advantage of preferential tax regimes and circumvent taxation in source countries. The action plan called for the elimination of such regimes, promoting a fair and transparent taxation system. In alignment with this action plan and conjunction with Action 1, India introduced the concept of SEP through the Finance Act, 2018. This amendment to the IT Act included SEP as a criterion for establishing a business connection with non-residents in India. SEP allows for the taxation of businesses with a substantial economic presence in India, irrespective of their physical presence.

As per Explanation 2A to s. 9(1)(i) of the IT Act, SEP is defined to include transactions in respect of any goods, services or property carried out by a non-resident in India, as well as systematic and continuous soliciting of business activities or engaging in interaction with users in India through digital means. Until May 2021, the thresholds for SEP were unspecified. However, in that month, the Central Board of Direct Taxes (‘CBDT’) issued a notification[ii] prescribing the limits for transactions and user engagement by inserting r. 11UD in the IT Rules, 1962 that became enforceable from 01.04.2022. As per this notification, a non-resident will be considered to have SEP in India if:

(i) The aggregate of payments arising from transactions in respect of any goods, services or property carried out by the non-resident with any person in India, including the provision of download of data or software in India, exceeds Rs. 2 crores in a previous year; or

(ii) The number of users with whom systematic and continuous business activities are solicited or who engage in interaction with the non-resident through digital means exceeds Rs. 3 lakhs in a previous year.

The notification also clarified that the provisions of SEP will not apply to income from royalties or fees for technical services, as these are already covered under the existing provisions of the IT Act.

SEP represents a novel concept that underscores India’s commitment to tackling taxation challenges posed by the digital economy. It aims to ensure that businesses deriving value from the Indian market contribute their fair share of taxes.

Action 7: PE Expansion & Concessional Tax Regime

BEPS Action 7 aimed to prevent the artificial avoidance of PE status by non-residents, which is used to escape taxation in the source countries. The action plan proposed changes to the definition of PE to include cases where an agent habitually concludes contracts or plays the principal role leading to the conclusion of contracts on behalf of a non-resident principal. India implemented these changes through the Finance Act, 2016 and the Finance Act, 2018, which amended the IT Act to include such cases as a criterion for establishing a business connection with non-residents in India. The Finance Act, 2018 proposed to broaden the scope of the term ‘business connection’ under s. 9 of the IT Act which became applicable from the assessment year 2019-2020.

The Finance Act, 2016 introduced s. 115BBF in the IT Act in compliance with BEPS Action 7 providing a concessional tax regime for royalty income from patents developed and registered in India. This regime is also known as the patent box regime, which is a preferential tax treatment for income derived from the exploitation of intellectual property rights. The patent box regime provides that the royalty income of an assessee, who is an Indian resident and a patentee (eligible taxpayer), shall be taxed at a reduced rate of 10%, subject to the condition that the patent is developed and registered in India. The regime covers income from the worldwide exploitation of patents and is intended to encourage innovation and research and development activities in India. These amendments aim to address the situations where non-residents use commissionaire arrangements or other intermediaries to avoid having a taxable presence in India.

Action 13: Country-by-Country Reporting

Under BEPS Action 13 provides a template for MNEs to report annually and for each tax jurisdiction in which they do business the information set out therein. India, as a member of the G20 and an active participant in the BEPS project, has adopted these recommendations through the Finance Act, 2016 *vide *ss. 92D and 286 of the IT Act. New rules in the form of rs. 10DA and 10DB were also inserted in the IT Rules, 1962 along with forms 3CEAA to 3CEAE for furnishing information. This introduced a comprehensive framework for transfer pricing documentation and reporting. The framework consists of two main components: the Master File and the Country-by-Country Report (‘CbCR’).

The Master File is a document that provides an overview of the MNE’s global business, including its organizational structure, business activities, intangibles, financial and tax positions, and transfer pricing policies. The Master File is intended to give a high-level picture of how the MNE operates and allocates profits among its group entities.

The CbCR is a document that provides detailed information on the MNE’s global allocation of income, taxes, and economic activity, by country and by entity. The CbCR is intended to give a granular view of where the MNE generates value and pays taxes and to identify potential risks of BEPS.

India has adopted the OECD’s standards and thresholds for preparing and filing the Master File and the CbCR, incorporating some modifications. The parent entity of the MNE group, or a designated surrogate entity, is required to file the Master File and the CbCR in their country of residence. This information is then shared with other tax authorities through automatic exchange of information agreements. In India, the Master File and the CbCR are mandated to be filed electronically with the IT authorities under s. 286 of the IT Act.

Multilateral Instrument Adoption

The Multilateral Instrument (‘MLI’), developed by the OECD, serves as a tool to implement measures against BEPS in tax treaties. Its primary goals include preventing tax avoidance, enhancing dispute resolution, and aligning treaty provisions with BEPS standards.

India demonstrated early commitment to these measures, being among the first countries to sign and ratify the MLI. The signing took place in Paris on 07.06.2017, and India deposited its instrument of ratification, along with its final positions, with the OECD on 25.06.2019.[iii] Effective from 01.04.2020, the MLI applies to 20 of India’s tax treaties, including those with Australia, France, Japan, the UK, and more. However, noteworthy treaties with the US, Mauritius, Germany, and China, are not covered by the MLI.

The MLI brought about modifications to treaty preambles, introduced a principal purpose test (‘PPT’), and established a simplified limitation on benefits (‘SLOB’) to counter treaty abuse. The PPT acts as a general anti-abuse rule, denying treaty benefits if obtaining a tax benefit is one of the primary purposes of an arrangement or transaction unless it aligns with the treaty’s object and purpose. Meanwhile, the SLOB sets out objective criteria, including listing, ownership, activity, and specified entities, which must be fulfilled by a person to qualify for treaty benefits. India has opted for both the PPT and the SLOB, with plans to replace the PPT with a LOB clause in the future due to the MLI matching principle.

The MLI introduces various provisions that broaden the scope of PE, including an extended dependent agency PE (‘DAPE’) rule, a stricter independent agent exclusion rule, a limitation of the specific activity exemption, an anti-fragmentation rule, and an anti-splitting rule. These provisions aim to prevent the artificial avoidance of PE status by businesses. While India has accepted all these changes, some treaty partners have not, leading to the modification of the PE definition only in treaties where both parties agree. Furthermore, some countries have selectively opted in specific PE provisions of the MLI and opted out of others.

Summary

Conclusion

India has demonstrated a proactive response to the BEPS initiative, underscoring its commitment to international tax standards and acknowledgement of the evolving challenges posed by the digital economy. The nation has undertaken substantial legislative reforms to align its tax laws with BEPS action plans, signifying its preparedness to adapt and actively engage in global efforts to combat tax avoidance.

Among the noteworthy measures implemented, the introduction of the equalization levy specifically addresses tax issues within the digital economy, showcasing India’s determination to ensure equitable competition between resident and non-resident service providers. Additionally, amendments to laws governing hybrid mismatch arrangements, interest deductions, SEP, and PE criteria reflect India’s steadfast commitment to safeguard its tax base and uphold principles of fair and transparent taxation.

India’s ratification of the MLI highlights its dedication to international collaboration for the effective implementation of BEPS measures. Provisions within the MLI, such as the PPT and the SLOB, bolster India’s ability to counteract treaty abuse and align its tax treaties with global standards.

Crucially, India’s strategic approach strikes a balance between protecting its tax base and fostering a business environment conducive to innovation and research. This approach is particularly relevant as the nation navigates the intricate dynamic of the digital economy and the ever-evolving international tax landscape. In positioning itself as a proactive player, India emerges as a significant influencer in shaping fair and efficient international tax policies amidst the ongoing transformation of the global tax landscape.

End Notes

[i] *Vide *Notification No. 28/2023- Central Tax dated 31.07.2023.

[ii] Notification No. 41/2021/F. No. 370142/11/2018-TPL dated 03.05.2021.

[iii] EY, ‘How can businesses assess Multilateral instruments-led changes in India’s tax treaties’, (3 January 2020) - How can businesses assess Multilateral instruments-led changes in India’s tax treaties? (ey.com)

Authored by Srishty Jaura, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinion.

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.