Introduction

The International Accounting Standards Board (‘IASB’) has issued a new standard, the International Financial Statement Reporting Standard 18 Presentation and Disclosure in Financial Statements (‘IFRS 18’). In India, IFRS is overseen by the Ministry of Corporate Affairs (‘MCA’), Government of India (‘GOI’), through the Institute of Chartered Accountants of India (‘ICAI’). IFRS 18 supersedes International Accounting Standards 1 (‘IAS 1’), which outlines the overall requirements for financial statements and will be effective for annual periods beginning on or after 01.01.2027. IFRS 18 aims to provide investors with transparent and accurate information about a company’s financial performance for future investments under the IFRS Accounting Standards[i]. This new standard will apply to all business entities using the IFRS Accounting Standards, whether public or private.

Background

The IASB issued IFRS 18 ‘Presentation and Disclosure in Financial Statements’ on 09.04.2024. This was to address the previous standards’ insufficient details of income and expenses. IFRS 18 includes three categories of income and expenses, two-income statement subtotals, and a single note on management performance measures. The evolution of IFRS 18 began in April 2016 with a Board Discussion, leading to a decision in May 2019 to publish an exposure draft. Thereafter, the exposure draft comment period was extended until September 2020. On 09.04.2024, IFRS 18 was officially issued. The objective of IFRS 18 is to ensure that all financial statements are prepared and presented according to IFRS accounting standards.

Key Changes in New Standard

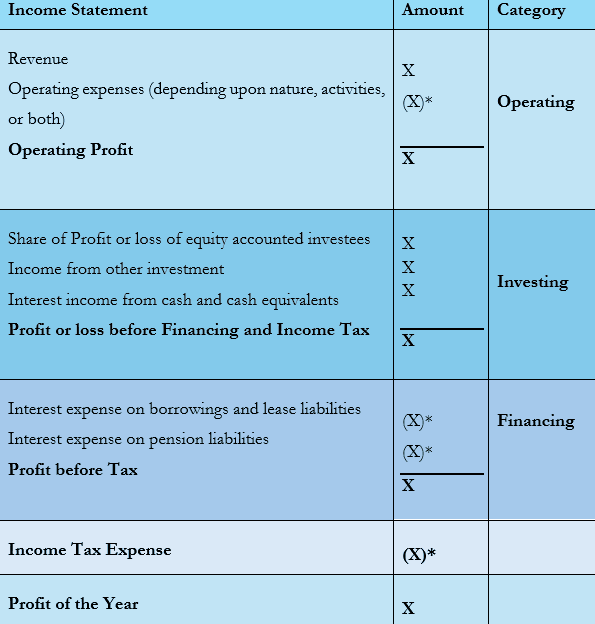

1. Structured Statement of Profit or Loss

Under the previous regime, companies had the freedom to choose which subtotals they included, thereby creating inconsistency for investors when comparing financials across companies. The new standard mandates that companies adhere to a structured format for classifying income and expenses into three categories—operating, investing, and financing—and requires the inclusion of specific subtotals.[ii]

2. New Concept of Management-defined Performance Measures (‘MPM’)

This measure, also known as Alternative Performance Measures (‘APM’) or Non-GAAP Measures[iii], allows companies to use non-GAAP measures to explain their financial statements. The introduction of MPM represents a significant shift in financial reporting practices. MPMs are defined as subtotals of income and expenses; used in public communications with users of financial statements outside the financial statements and communicate management’s view of an aspect of an entity’s financial performance.

Companies need to elaborate in a single note to the financial statements, explaining the measure offers valuable information, detailing its calculation method, and reconciling it to an amount determined under IFRS accounting standards.

3. Guidance on Aggregation/Disaggregation

The new requirements for aggregation and disaggregation extend to primary financial statements, now encompassing newly defined roles, shared characteristics, and single dissimilar characteristics. In other words, it provides guidelines for determining line items in primary financial statements and note disclosures, discouraging the use of generic labels such as ‘other.’ Additionally, goodwill has been added as a new item in the balance sheet.

Conclusion

The new standard will be effective for annual reporting periods beginning on or after 01.01.2027, including for interim financial statements, whereby early adoption is also permitted. It is crucial for companies using IFRS to implement this standard and assess its potential impact on their financial statements. Transparent communication with investors about requirements is vital, ensuring clarity and changes required for future references. Furthermore, companies should evaluate how the new requirements will affect their financial reporting systems, making any necessary adjustments to ensure compliance. It is also important to stay aware of any local adjustments from this standard.[iv]

End Notes

[i] 161 taxmann.com 469 (Article)

[ii] Presentation and Disclosure in the Financial Statements - IFRS 18 (2024),

[iii] Non-GAAP financial measures are numerical indicators of a company’s historical or future financial performance, financial position, or cash flows. These measures adjust the most directly comparable GAAP (Generally Accepted Accounting Principles) figures by excluding certain items that the company believes are not good indicators of its performance.

[iv] How Companies Communicate Financial Performance is..., KPMG (09.04.2024),

https://kpmg.com/xx/en/home/insights/2024/04/presentation-and-disclosure-ifrs18.html

Authored by Siddharth Jha, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinion.

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.