Introduction

The Ministry of Micro, Small and Medium Enterprises (‘MSMEs’), through a Notification[i], has amended the existing criteria for classifying enterprises as Micro, Small, and Medium under s. 7 of the MSME Development Act, 2006 (‘Act’). The amendments revise the threshold limits for investment in plant and machinery/equipment and turnover, effective from 01.04.2025.

Background

Earlier, the classification of MSMEs was based on investment and turnover thresholds as notified in the earlier Notification[ii]. Based on the recommendations of the Advisory Committee constituted under the Act, the Central Government has enhanced these thresholds to broaden MSME coverage and enable larger enterprises to avail MSME benefits.

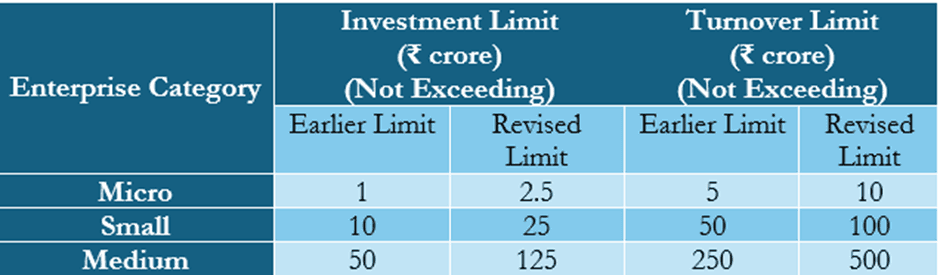

Revised Classification Criteria

The following table summarizes the revised investment and turnover limits for MSMEs classification:

Our Analysis

The amendments to the earlier Notification, as outlined in the amended Notification, represent a significant policy shift aimed at broadening the scope of enterprises qualifying as Micro, Small, and Medium Enterprises under s. 7 of the Act. By enhancing the investment and turnover thresholds, the Central Government has aligned the classification criteria with prevailing economic conditions, inflationary trends, and evolving industry demands. This revision is expected to extend statutory benefits under various schemes, such as priority sector lending, tax concessions, and public procurement incentives, to a wider base of enterprises. The revised thresholds are also likely to improve the flow of institutional credit to mid-sized enterprises that were previously excluded from the MSME ambit, thereby reducing their reliance on high-cost informal financing.

Moreover, the broadened eligibility criteria necessitate focused outreach and capacity-building efforts to ensure that newly eligible enterprises are aware of, and able to access, the benefits under the Udyam registration framework.

However, enterprises seeking reclassification are required to update their Udyam Registration in a timely manner in accordance with the revised thresholds to remain compliant and continue to be eligible for benefits under the Act.

End Notes

[i] No. S.O. 1364(E) dated 21.03.2025.

[ii] No. S.O. 2119(E) dated 26.06.2020.

Authored by Onam Singhal, Chartered Accountant at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.