BEPS 2.0, a transformative global tax reform initiative, introduces a two-pillar approach to address the challenges of international taxation in our digitally connected world. Pillar One shifts the focus to market presence-based taxation, realigning taxing rights for multinational enterprises. Pillar Two establishes a global minimum corporate tax rate to combat tax competition. This comprehensive analysis examines the intricacies of BEPS 2.0, detailing its policies and implications for businesses and international taxation. As the international tax landscape evolves, businesses must adapt to these complex changes, with the potential for substantial impacts on tax revenues and compliance burdens. BEPS 2.0 marks a historic shift in global taxation, demanding vigilance, and adaptation from multinational corporations worldwide.

Introduction

In an era marked by rapid globalization and the surge of digital commerce, the challenges confronting international taxation have grown significantly. The ascent of multinational corporations (‘MNCs’) and the ever-evolving global economic landscape necessitate adjustments to the existing tax framework. In response to these complexities, the G20/OECD Inclusive Framework (‘IF’) on Base Erosion and Profit Shifting (‘BEPS’) has introduced BEPS 2.0, a global tax reform initiative. This article offers an in-depth exploration of BEPS 2.0, providing a detailed analysis of its two-pillar approach and the far-reaching implications it holds for businesses and international taxation.

Pillar One: Market Presence-Based Taxation

Pillar One of BEPS 2.0 represents a fundamental paradigm shift in international taxation, prioritizing the allocation of taxing rights predicated on market presence rather than physical presence. Its primary objective is to address the profound impact of the digital economy on the allocation of taxing rights between the home country of an MNC and the market jurisdictions where they conduct their operations.

Under Pillar One, a portion of the profit generated by multinational enterprises (‘MNEs’) that surpasses specific thresholds is reallocated to market jurisdictions. The core concept, ‘Amount A’, is applicable to MNEs with a global annual turnover exceeding EUR 20 billion and a profitability margin exceeding 10%. Notably, the extractive and regulated financial services sectors fall beyond its purview. Market countries are entitled to an allocation of Amount A if they generate revenues of at least EUR 1 million. For countries with a GDP below EUR 40 billion, this threshold is set at EUR 250,000. Revenues are attributed to the market country where goods or services are consumed, and specific rules for sourcing revenues in various transactions will be developed.

Entities within the scope of Pillar One will reallocate a portion, typically ranging from 20% to 30% of their residual profit exceeding a 10% profit level to market countries. The 10% profit level is ascertained through the ratio of profit before tax (‘PBT’) to revenue. A marketing and distribution profits safe harbour has been designed to limit the Amount A allocation in instances where residual profits have already been subject to taxation in market countries. Any Amount A liability will be allocated to entities that have earned residual profit and will be alleviated through exemption or credit mechanisms. This streamlined administration empowers businesses to oversee their compliance through a single entity.

The implementation of BEPS 2.0 coincides with the removal of digital services taxes and similar measures, ensuring a coordinated international approach.

Pillar One Policies

1) User Contribution: This approach considers the significant value that users of digital services contribute to digital firms. It proposes allocating profits to countries where users are located, affecting platforms like social media, search engines, and online marketplaces.

2) Marketing Intangibles: This approach reallocates taxing rights based on marketing intangibles, impacting a broad range of multinational businesses. Its primary objective is to allocate income to market countries based on the value derived from marketing intangibles.

3) Significant Economic Presence (‘SEP’): This approach introduces a taxable nexus that incorporates SEP, thereby allocating taxing rights based on non-physical factors. It takes into consideration various factors, including the existence of a user base, data input, billing and collection in local currency, website maintenance, and marketing activities.

To ensure the effectiveness of Pillar One, the precise identification of market jurisdictions from which revenue is derived is of paramount importance. Draft rules for Nexus and Revenue Sourcing have been thoughtfully proposed to provide guidance in this regard, guaranteeing the accurate attribution of profits to market jurisdictions based on factors such as local revenues. Furthermore, Pillar One’s Scope Rules are geared towards large and highly profitable MNEs, with particular emphasis placed on the Ultimate Parent Entity level, thereby providing comprehensive clarity regarding the implementation of these policies.

Under Pillar One, taxable profits allocable to market jurisdictions are based on the summation of the following amounts:

Amount A: A portion of MNE’s residual/excess profit allocated to market jurisdictions.

Amount B: Fixed remuneration for ‘baseline’ routine marketing and distribution activities in line with Arms’ Length Price.

The computation of Amount A involves three steps:

Step 1: Establish a profitability threshold based on a PBT to revenue ratio, identifying residual profit subject to reallocation (10% of revenues).

Step 2: Apply the reallocation percentage to determine the share of residual profits allocated to market jurisdictions (25% of residual profit).

Step 3: Utilize an allocation key based on locally sourced in-scope revenues to distribute Amount A among eligible market jurisdictions.

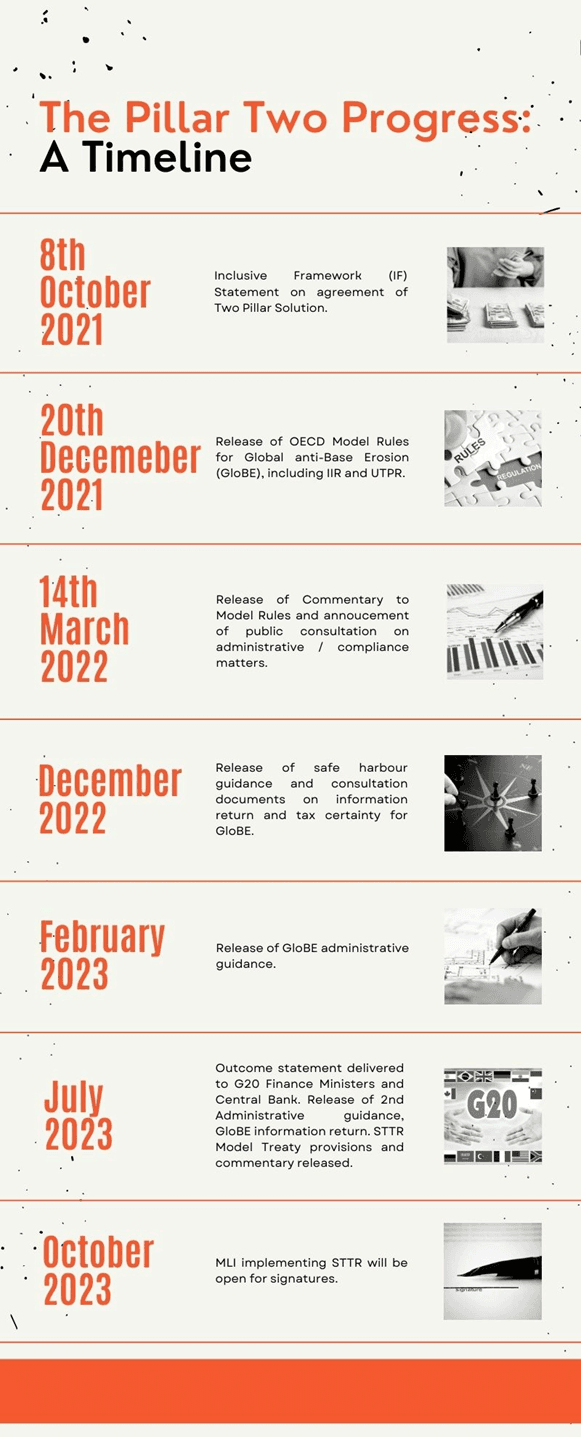

The Organization for Economic Co-operation and Development (‘OECD’) has made significant progress on Pillar One. Progress reports, which were issued in both July and October 2022, incorporate draft technical model rules designed to enable market jurisdictions to levy taxes on profits generated by some of the largest MNEs. Additionally, public consultation documents, such as those for ‘Amount B’, aim to streamline the application of the arm’s length principle in baseline marketing and distribution activities, enhancing tax certainty and reducing disputes. Furthermore, there is an ongoing effort to develop a multilateral convention (‘MLI’) that will facilitate a uniform and harmonized implementation of Pillar One across participating jurisdictions.

Pillar Two: Global Minimum Corporate Tax

Pillar Two, also known as the Global Anti-Base Erosion Rules (‘GloBE’), introduces a global minimum corporate tax rate of 15%. Its primary focus is to counteract tax competition among companies with consolidated revenues exceeding €750 million. Pillar Two consists of two interlinked domestic rules: the Income Inclusion Rule (‘IIR’) and the Undertaxed Payment Rule (‘UTPR’). Additionally, a ‘subject to tax rule’ (‘STTR’) safeguards the prerogative of developing countries to impose taxes on specific base-eroding payments, such as interest and royalties, up to the minimum rate of 15%.

The GloBE rules introduce a top-up tax on MNEs when their effective tax rate (‘ETR’) in a jurisdiction falls below the agreed minimum rate. This calculation considers a jurisdictional ETR to determine if it qualifies as a low-tax jurisdiction. The top-up tax ensures that global minimum tax standards are met and allows for the adjustment of income and taxes across jurisdictions to prevent double non-taxation.

Pillar Two Rules

1) IIR: The parent company is responsible for paying a top-up tax to ensure that the ETR on its proportionate share of income from group entities situated in low-tax jurisdictions reaches a minimum of 15%. The method for allocating top-up taxes is still a subject of ongoing discussion, particularly concerning profits with low-tax burdens in the parent company's home country. In cases where the IIR cannot be applied, the UTPR serves as an alternative.

ETR Calculation: The ETR calculation is based on financial accounts with agreed adjustments and mechanisms to address timing differences.

Switch-Over Rule: Compliments the IIR by providing a mechanism to overturn tax treaty obligations.

2) UTPR: UTPR comes into play when the IIR cannot be applied. Under this rule, the MNE Group allocates top-up tax to group entities based on deductible payments made to entities located in low-tax jurisdictions. It is important to note that the IIR takes precedence over the UTPR.

3) STTR: STTR is triggered when a covered payment is subject to a nominal tax rate in the payee jurisdiction. For example, if a payment is taxable at 5% in the payee jurisdiction, the STTR mandates an additional withholding tax at 4% in the payer jurisdiction, irrespective of the tax treaty rate. The STTR ensures that base-eroding payments, such as interest and royalties, are subject to taxation at a minimum rate of 15%.

The pertinent policy document assesses the current policy landscape as one characterized by disjointed and unilateral actions aimed at attracting and safeguarding tax revenues. This situation raises concerns for both developed and developing countries, emphasizing the risks of double taxation and potential protectionist measures.

In response, the document discusses the implementation of the IIR and a tax on base-eroding payments, aligning with the approach taken by the USA in its policies, such as the Global Intangible Low-Taxed Income and Base Erosion and Anti-Abuse Treaty regulations. The IIR empowers jurisdictions to tax foreign subsidiaries with low ETR, while the tax on base-eroding payments denies deductions or treaty relief unless such payments meet a minimum ETR. These initiatives primarily apply to multinational groups with consolidated revenues exceeding EUR 750 million, with some flexibility for countries to set lower thresholds for domestically headquartered groups. Notably, government entities, international organizations, non-profit entities, pension funds, and investment funds, along with their holding vehicles, are exempt from these rules.

While the Pillar Two rules are not mandatory, countries choosing to adopt them must adhere to the model rules and guidance provided by the IF. The OECD has provided model rules for Pillar Two, facilitating the integration of these regulations into domestic legislation, encompassing aspects like the GloBE rules, the treatment of acquisitions and disposals, and administrative considerations for MNEs subject to the global minimum tax.

Impact on Businesses and International Taxation

The implementation of BEPS 2.0 indicates significant changes for international businesses. The restructuring of international tax principles under these two pillars will usher in increased complexity and alterations in tax liability. Businesses are compelled to undertake a comprehensive assessment of their tax cost, cash flow, profitability, and financial statements. This process necessitates an assessment of existing supply chains, ownership structures, and technology, all the while ensuring alignment with the documentation and compliance requisites of BEPS 2.0. Moreover, businesses must be poised to confront pivotal issues, including the determination of the applicability of Pillar One and Pillar Two to their operations, compliance with new documentation and compliance standards, and the assurance that in-house tax teams are proficient in navigating the evolving international tax landscape. Adapting to these changes is imperative for businesses operating in the global arena, given the transformation BEPS 2.0 heralds in international taxation.

The Indian Perspective

In 2012, India embarked on a transformative journey in digital taxation by amending its domestic tax laws to redefine the term ‘royalty’. As a member of the IF, actively engaged in the implementation of the GloBE Rules, India has found itself under increased scrutiny regarding the PE concept, which has traditionally been the basis for taxing corporate profits. Indian tax authorities have broadened their purview, recognizing the existence of virtual PEs, thereby extending beyond conventional PE definitions.

India, in a pioneering move, emerged as the first country to enact an equalization levy, fixed at 6%, targeting funds received or due to non-resident entities for specific digital services provided within the country. Furthermore, India has undertaken substantial efforts to introduce the concept of SEP to amend guidelines concerning profit attribution to a PE.

The SEP concept expands the interpretation of a ‘business connection’ used to determine tax liability under the Income-Tax Act, 1961. This broadened interpretation is a response to the complexities arising from the digital economy and e-commerce. The primary objective is to ensure that enterprises with a substantial economic presence in India are subject to appropriate taxation, thus addressing the intricacies of the contemporary digital landscape. India’s proactive stance in this arena reflects its commitment to adapting to the evolving international tax landscape and ensuring that digital businesses contribute their fair share to the nation’s tax revenues.

Conclusion

BEPS 2.0, with its two-pillar approach, signifies a momentous transformation in the realm of international taxation. Pillar One introduces the revolutionary concept of market presence-based taxation, while Pillar Two establishes a global minimum corporate tax rate. These initiatives have been meticulously designed to adapt to the ever-evolving global economy, with a particular focus on the digital age.

Despite the substantial progress made in the development of BEPS 2.0, it remains a complex and continually evolving framework. The implications for businesses are substantial, necessitating a comprehensive evaluation of their operations, tax obligations, and compliance measures. As the international tax landscape continues to undergo profound changes, it is imperative for businesses operating in the global marketplace to remain vigilant, well-informed, and adaptive.

The two-pillar solution marks a historic development that seeks to reform century-old tax laws, exerting a significant influence on large corporate entities across the globe. Both Indian-based groups with international operations and foreign-based groups with interests in India must meticulously assess the impact, taking into account the potential for additional tax outflows and an augmented compliance burden. According to estimations by the OECD, Pillar Two is poised to yield additional annual tax revenue of US$150 billion, while Pillar One is anticipated to result in the reallocation of up to US$100 billion in favour of market jurisdictions. This underscores the far-reaching and substantial impact of BEPS 2.0 on the international taxation landscape. As the international tax landscape continues to evolve, staying informed and adapting to these changes will be crucial for businesses operating in the global marketplace.

In this backdrop, it will be crucial to see how India re-aligns its young amendments of equalization levy and SEP to BEPS 2.0. The equalization levy may not be compatible with Pillar One whereunder India may be entitled to a share of the residual profit of such businesses, based on their revenue and user base. This may result in double taxation or double non-taxation, depending on how the equalization levy and the Pillar One amount are coordinated. Therefore, India may need to reconsider the scope and applicability of the equalization levy or seek to negotiate a credit mechanism under the Pillar One agreement. With regard to SEP, India may not be able to tax the non-resident entities under Pillar One, unless they fall within the scope of the new nexus rule. As a result, India may need to revise or defer the SEP concept or seek to incorporate it into the Pillar One agreement. Therefore, BEPS 2.0 will have a significant impact on India’s taxation of the digital economy and may require some adjustments to the existing or proposed unilateral measures.

Authored by Srishty Jaura, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinion.

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.