Introduction

India launched the Advance Pricing Agreement program (‘APA’) through the Finance Act, 2012 (FA 2012) as a proactive strategy to tackle its complex transfer pricing ('TP') challenges. Prior to the introduction of APAs, disputes over TP were common, particularly involving large multinational corporations (‘MNCs’) (such as Microsoft and Vodafone), raising concerns about the implications of India’s tax environment on foreign investments.

APAs were designed to serve as a crucial mechanism for resolving disputes related to cross-border transactions. They allow multinational companies and tax authorities to establish arm’s length pricing agreements in advance. The primary aim is to clarify, minimise litigation, and foster a more investor-friendly atmosphere in light of India’s rigorous tax audits.

The development of APAs in India represents a paradigm shift in the approach to TP, offering a proactive and cooperative method for handling cross-border tax disputes. The APA framework has become a vital tool for navigating the intricacies of TP, which has long been a contentious issue for multinational companies operating in India. By incorporating global best practices and aligning with the OECD guidelines, India’s APA system not only ensures compliance and certainty for taxpayers but also highlights the country’s dedication to fostering a transparent and investor-friendly tax landscape. This article explores the quintessential features of India’s APA framework, its various types, and its crucial role in resolving TP disputes while examining its economic and global implications.

Evolution of APAs in India

The introduction of APAs under the Income-tax Act, 1961 (‘Income-tax Act’) was a significant step toward curtailing TP disputes in India.[i] These agreements allow taxpayers to negotiate and pre-determine the following:

a. arm’s length price (‘ALP’) or the pricing methodology for computing ALP for international transactions,

b. the income deemed to accrue in India[ii] or the basis on which such income will be determined, as is reasonably attributable to the operations carried out in India[iii].

APAs can be unilateral[iv], bilateral[v], or multilateral[vi], depending on whether the agreements involve solely the Indian tax authorities or other authorities in foreign jurisdictions. Upon approval from the Central Government, the Central Board of Direct Taxes (‘CBDT’) is empowered to enter into these agreements for a period not exceeding five consecutive years.[vii] Additionally, the roll-back provisions, although a later integration, permit retrospective application of the APA methodology for four preceding years, extending the benefit to a total of nine years.[viii]

The Indian APA regime has evolved as a groundbreaking mechanism to address the long-standing complexities of TP disputes. First proposed as a part of the Direct Taxes Code in 2009, the framework faced delays due to the uncertainty surrounding the Code’s implementation. However, the introduction of APAs in the FA 2012 marked a significant turning point in India’s TP landscape. The APA rules, notified through amendments to the Income-tax Rules, 1962 (‘Income-tax Rules’), created an efficient framework, integrating global best practices such as pre-filing consultations, detailed application processes, and expert-led assessments[ix].

TP and APAs

APAs are agreements between the taxpayer and the tax authorities to promote mutually satisfying TP. These agreements assist in determining the arm’s length price or the manner of determination of the arm’s length price for international transactions. It helps avoid long-drawn dispute resolution as it is negotiated and agreed upon in consonance with the tax authorities of the specific country where the profits are generated. In each case, the agreement will specify the nature, method, and responsibilities of the taxpayer, and it will be binding for a maximum of five years. The primary goal of the APAs is to reach a mutually acceptable price and avoid disputes by setting the price in advance. Unlike traditional agreements, there is an absence of mutual bargaining among the parties as the price is settled at an ALP. Hence, the parties are committed to setting the price whether or not it is in their private interest. This, in turn, is a good tax planning strategy.

TP is about setting the right price for transactions between companies within the same multinational group, also known as the ALP. These are cross-border deals between related parties or associated enterprises[x]. Over the years, TP has become one of the most contentious areas of tax disputes for MNCs due to its significant impact on tax revenues. On a global scale, the tax authorities treat TP as a critical issue, requiring detailed scrutiny, extensive documentation, and a deep understanding of both local tax laws and international guidelines like those from the OECD. India is no exception. In fact, India witnessed TP disputes skyrocket, with adjustments during the sixth audit cycle reaching an eye-watering Rs. 44,000 crore (around USD 9.78 billion) more than the combined adjustments of the previous four years. Unsurprisingly, India also holds the dubious distinction of having the highest number of TP litigations globally, with MNCs often accused of shifting profits abroad to minimise taxes.

Mechanisms like the Mutual Agreement Procedure (‘MAP’) have gained traction in recent years to address these disputes and avoid double taxation. Under MAP, the tax authorities from two countries collaborate to resolve conflicts, typically through their respective Competent Authorities. While MAP has its advantages, it is far from perfect. It is an optional route in India and is often criticised for being too slow, taking an average of 2-3 years to resolve such cases. Moreover, it only kicks in after multiple audits and TP adjustments, unlike APAs, which take a more proactive approach.

APAs have emerged as a game-changer, addressing the bottlenecks of TP audits. In India, the APA regime is a positive step forward. Once an APA is finalised, the regular audit of covered transactions is no longer required. Instead, the TP Officer (‘TPO’) conducts a compliance audit each year and then reports their findings to the Director General of Income Tax (International Taxation) (‘DGIT’) for unilateral agreements or to the Competent Authority for bilateral or multilateral agreements.

As discussed above, the scope of APAs encompasses not only the determination of ALP for international transactions but also the computation of income reasonably attributable to non-residents for operations carried out in India. The taxpayers can rely on prescribed methods[xi] for incomes deemed to accrue or arise in India to arrive at a mutual agreement that overrides conventional assessments by the Assessing Officers (‘AO’). These agreements bind the taxpayer(s), the Principal Commissioner/Commissioner, and the subordinate income tax authorities, ensuring streamlined and predictable tax assessment processes[xii]. However, APAs may lose their binding effect if there is a change in the law or facts fundamental to the agreement[xiii].

To further operationalise the APA regime, the Income-tax Act mandates filing a modified return within three months from the month the agreement was entered. This provision ensures alignment between past tax filings and the terms of the APA. If the assessments for such periods are completed before the APA, the AO must revise the total income in accordance with the agreement[xiv].

The bilateral or multilateral APAs require coordination amongst the Indian competent (tax) authority and their respective counterparts in the other countries to negotiate mutually agreeable terms. The process is initiated only if the associated enterprise located abroad has started APA negotiations with their respective competent authority. The Indian competent authority undertakes discussions with the foreign authorities, striving to reach mutually acceptable terms formalised as a MAP. While taxpayers are not directly involved in these negotiations, they may consult the Indian authority during the APA process. The taxpayer can opt for a unilateral APA or withdraw their application if mutual agreement fails[xv].

On an international level, APAs have proven to be reliable tools for managing TP issues, offering certainty to taxpayers and reducing audits and litigation. Many countries have adopted APAs to give businesses clarity and confidence in their tax compliance. Thus, the APA framework in India represents a significant leap in the right direction.

Types of APAs Under the Indian Tax Regime

An APA is a formal agreement between a taxpayer and the tax authority that establishes the TP methodology for the taxpayer’s international transactions for future years. This proactive mechanism is designed to provide clarity and prevent potential disputes related to TP.

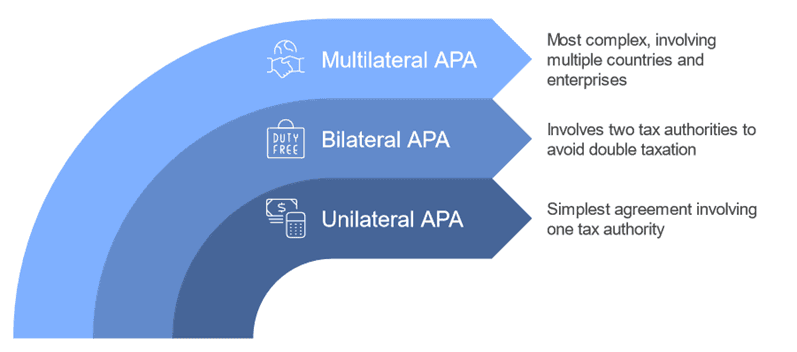

APAs can be classified into three types: unilateral, bilateral, and multilateral.

A Unilateral APA (‘UAPA’) is an agreement between the taxpayer and the tax authority of the taxpayer’s country of residence. This type of APA does not involve any foreign tax authorities or associated enterprises outside the taxpayer’s home country. Unilateral agreements are generally simpler and quicker to negotiate compared to bilateral or multilateral arrangements, making them suitable for taxpayers engaging in transactions that remain within the jurisdiction of a single tax authority.

A Bilateral APA (‘BAPA’), on the other hand, involves two tax authorities, typically the tax authorities of the taxpayer’s country of residence and the country where the associated enterprise is located. It also includes the taxpayer and the associated enterprise as key participants. Negotiated under the framework of a tax treaty, bilateral APAs often use the MAP to facilitate consensus. These agreements provide greater certainty in both jurisdictions and help avoid double taxation through corresponding adjustments. Additionally, they minimise disputes between countries regarding TP, offering a more robust solution for cross-border transactions.

The most complex type is the Multilateral APA (‘MAPA’), which involves the taxpayer, two or more associated enterprises in different countries, the tax authority of the taxpayer's country, and the tax authorities of the associated enterprises. The MAPAs are designed to comprehensively address TP issues for transactions spanning multiple jurisdictions. While they provide an efficient mechanism for agreement across various tax authorities, the negotiation process is significantly more challenging due to the number of parties and jurisdictions involved. As of 2018, India has not entered into any multilateral APAs, reflecting the logistical and procedural complexities associated with these agreements.

Each type of APA serves a distinct purpose, with its scope and challenges tailored to the taxpayer’s operational needs and the jurisdictions involved. Together, these agreements provide businesses with a pathway to navigate the intricacies of TP compliance while reducing the risks of disputes and double taxation.

APA Process and Framework

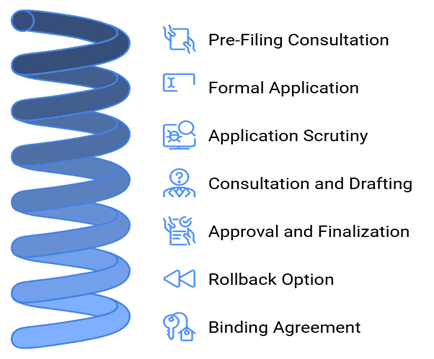

The APA process starts with a mandatory pre-filing consultation. This allows tax authorities to screen applications and gauge potential disputes, reducing the chances of non-serious applications. The consultation follows application submission, rigorous audits, compliance checks, and periodic evaluations. These steps help maintain an objective and cooperative tax environment, though they require substantial time and documentation from the applicants.

The process allows taxpayers and their counsel to meet with specialists from the APA division to determine whether their case suits an APA. During this evaluation, both the taxpayer and tax authorities review the relevant facts, discuss the appropriate TP method, and come to an agreement. Once finalised, the taxpayer commits to adhering to the agreed arm’s length margin or price for the next 5 years unless unforeseen circumstances or significant changes arise. The process lifetime of an APA is discussed as follows:

Pre-filing Consultation: As a precursor to the APA process, applicants may request a pre-filing consultation with the department[xvi]. This request must be made in writing and submitted to the DGIT[xvii]. During this stage, the APA team conducts consultations with the applicant to determine the scope of the agreement, identify the TP issues, assess the suitability of the transactions for the APA process, and discuss the broad terms of the agreement. This stage, however, does not bind either party to proceed with the agreement or indicate that a formal application has been submitted.

Application For APA: To initiate the APA process, the applicant must submit a formal application along with the prescribed fee[xviii]. The application is submitted to the DGIT for unilateral agreements or to the competent authority in India for bilateral or multilateral agreements. Applications can be filed either before the start of the relevant assessment year or before undertaking the transaction, depending on whether the transaction is ongoing or prospective. The fee for such agreements is determined based on the value of the international transactions, ranging from Rs. 10 lakhs to Rs. 20 lakhs, as specified in the APA Rules.

Withdrawal of Application: Applicants reserve the right to withdraw their application at any time before finalising the agreement terms by submitting the prescribed form. However, the fee paid during application submission is non-refundable upon withdrawal[xix].

Scrutiny and Deficiency Removal: If any defects are noted in the application, the competent authority in India will issue a deficiency letter within one month of receiving the application. The applicants have 15 days to address such deficiencies, which can be extended up to 30 days. Failure to address the deficiencies may result in the application being rejected after providing the applicant with an opportunity to be heard. In such cases, the application fee is refunded[xx].

Processing and Negotiation: Once an application is deemed complete, it is processed by the APA division team in consultation with the applicant. This includes conducting meetings, requesting additional information if necessary, conducting business visits, or making necessary inquiries. In bilateral or multilateral agreements cases, the competent authority in India forwards the application to the DGIT, which assigns it to an APA team. The team drafts a report that serves as the basis for finalising the agreement[xxi]. For bilateral or multilateral agreements, r. 44GA procedures are also invoked, and a mutually agreed draft agreement is prepared for approval.

The proposed draft agreement, incorporating all negotiated terms, is subject to approval by the Central Government. Once approved, the agreement is formally signed between the tax authorities and the applicant. A copy of the agreement is sent to the Commissioner of Income-tax overseeing the applicant.

Terms And Conditions of the APA: The finalised APA specifies the international transactions covered, the agreed TP methodology, the determined ALP, critical assumptions, and any conditions beyond the provisions of the Act or Rules. Any discrepancies in the critical assumptions or failure to meet specified conditions can render the APA non-binding. Either party must communicate Such changes in writing, and the agreement must be revised or cancelled as necessary[xxii].

Rollback Provisions: The APA may include rollback provisions to determine the ALP, the methodology to calculate the ALP, or the income deemed to be accrued in India for a maximum of four prior years[xxiii]. These provisions are applicable only if the transaction during the rollback years is the same as that covered by the APA and if the applicant meets the necessary conditions, such as timely filing of returns and reports[xxiv]. The rollback provisions are not available if the matter is under appeal or if they reduce taxable income or increase losses for the applicant. An additional fee of Rs. 5 lakhs is payable for rollback provisions.

Amendment of Applications: The applicants may request amendments to their applications at any stage before the agreement terms are finalised. Amendments are permitted only if they do not alter the nature of the original application[xxv].

Statistical Overview and Economic Impact

The sectoral and industry-wide distribution of APA applicants demonstrates a diverse range of industries benefiting from this framework. According to CBDT's fifth Annual Report, the majority of agreements finalised for FY 2022–23 were in the service sector, particularly businesses involved in IT-enabled services, software development, contract research and development, engineering design, and knowledge process outsourcing.

S. No. | Economic Activity | Agreements Signed |

|---|---|---|

1. | Service | 44 |

2. | Manufacturing & Trading | 4 |

3. | Trading & Services | 5 |

4. | Manufacturing & Service | 8 |

5 | Manufacturing, trading & Service | 2 |

Of the 63 businesses with which the CBDT signed agreements, 14 were engaged in manufacturing, while 11 operated in trading. This underscores the versatility of the APA program in addressing TP concerns across varied industries. The IT sector, banking and insurance, and engineering services represented the largest share of UAPAs signed during the financial year, reaffirming India’s reputation as a global hub for IT and business process outsourcing. With a significant concentration of multinational enterprises in IT clusters such as Bengaluru, Hyderabad, Chennai, Gurgaon, and Noida, the industry accounted for 18 APAs. In comparison, the services sector signed 26 APAs, and the pharmaceutical and chemical sectors concluded 11 agreements.

S. No. | Industry | Agreements Signed |

|---|---|---|

1. | Information Technology | 18 |

2. | Cement | 1 |

3. | Pharmaceuticals/Chemicals | 11 |

4. | Automotive | 2 |

5. | Services | 26 |

6. | Packaging | 1 |

7. | Beverages | 2 |

8. | Publication | 1 |

9. | Apparel | 1 |

The smaller sectors, such as cement, packaging, publishing, and apparel industries, also participated in the APA framework; each recorded one APA, while the automobile and beverage sectors saw two APAs each. The cumulative impact of a total of 516 APAs signed thus far is significant, providing certainty to the taxation of approximately Rs. 190 billion (US$2.2 billion) in revenue, corresponding to around Rs. 70 billion (US$838 million) in tax payments.

Global Comparisons and India’s Position

Throughout the world, mature tax jurisdictions such as the United States, Japan, and Australia have leveraged APAs to streamline TP compliance. These countries emphasise transparency, time-bound resolutions, and public reporting. India’s APA regime, although a later entrant, has rapidly gained traction due to its comprehensive framework and alignment with the OECD guidelines. While India’s APA program is at par with the global standards in terms of scope and applicability, it lags in certain areas, such as the absence of formal rollback provisions and strictly defined timelines for conclusion. Despite these challenges, India’s proactive approach to resolving disputes has established it as a stronger player in the international APA ecosystem, attracting MNCs seeking tax certainty in a complex regulatory environment.

In terms of processing timelines, the average time to complete BAPAs in India slightly increased to approximately 62.1 months in FY23, influenced by the resolution of long-standing cases with the treaty partners. Nevertheless, India has maintained its focus on expediting renewals by leveraging the due diligence undertaken during the original application process. This has resulted in a modest reduction in the average time for all BAPAs finalised by March 31, 2023, decreasing from 58.91 months in the previous year to 58.77 months.

The processing time for APAs varies across the globe. For instance, in the United States, the average time to conclude an APA increased to 43.4 months in 2022, up from 35.1 months in 2021. This comparison highlights India’s continued efforts to refine and streamline its APA process while ensuring comprehensive resolution of cases.

Critical Role of APA in Resolving TP Disputes

The APA framework in India is a critical mechanism for addressing TP disputes and ensuring tax certainty for international transactions. Since its inception, the APA regime has effectively mitigated disputes by ensuring certainty and transparency in tax obligations. For instance, it has significantly streamlined dispute resolutions for high-value complex transactions in IT services, pharmaceuticals, and manufacturing sectors, constituting a larger portion of India’s APA agreements. The program minimises post-transaction audits and litigation by addressing pricing methodologies and terms upfront. APAs offer several advantages to taxpayers and tax authorities alike:

Scope and Applicability: The framework also applies to residents and non-residents for income reasonably attributable to operations in India. APAs can be entered into for specific international transactions or a series of transactions, providing flexibility to businesses.

Methods for Determination: The determination of ALP can be based on prescribed methods such as Comparable Uncontrolled Price (CUP), Resale Price Method (RPM), etc.[xxvi] or any other methods prescribed in the Income-tax Rules. The APA allows adjustments or variations to these methods if necessary to suit the transaction’s unique nature.

Binding Nature and Certainty: Once executed, an APA is binding on the taxpayer for the agreed transactions, and the tax authorities ensure consistent application across all assessment levels. However, the APAs are not binding if a law change or material facts affect the agreement’s terms.

Roll-Back Provisions: The APA framework includes a roll-back provision, allowing the agreed terms to apply retrospectively to the four assessment years preceding the year of the agreement. This came as an excellent later addition, providing further relief and helping to reduce the overall TP disputes. The roll-back, however, is subject to the condition that the transaction and facts remain consistent with those specified in the APA.

Validity And Term Of APAs: An APA can be valid for a maximum of five consecutive previous years. The framework can cover up to nine years of transactions by including the roll-back provisions.

Flexibility in Scope: APAs can address both unilateral transactions and bilateral/multilateral transactions involving mutual agreement procedures MAPs with other jurisdictions.

Anti-Fraud Safeguards: APAs obtained through fraud or misrepresentation can be declared void ab initio. Upon such an incidence, all tax provisions are applied as if the agreement had never been entered into[xxvii].

Modified Return Filing and Adjustment of Assessments: The taxpayers who have already filed their returns can submit a modified return within three months of the agreement date. If the assessments or reassessments are completed prior to the APA, they must be revised in accordance with the APA. Pending assessments are completed as per the APA terms. This ensures seamless alignment between the agreement and the tax authorities’ evaluations.

Limitation Period Extensions: The APA framework provides for extending the limitation period for the assessments or reassessments by twelve months to account for modifications due to the APA.

MAP Integration: Bilateral/multilateral APAs require consultation between Indian authorities and their counterparts in other jurisdictions. The taxpayer, although not a part of these discussions, can meet with the Indian authorities for clarifications and treatment of such transactions.

Thus, APAs have emerged as a vital tool in resolving TP disputes by offering predictability and minimising litigation. In India, where TP adjustments have historically led to contentious audits, APAs provide an alternative by pre-emptively agreeing on the TP methodologies. This framework fosters a cooperative relationship between taxpayers and tax authorities, reducing the adversarial nature of tax compliance. Moreover, APAs mitigate the risk of double taxation, particularly in cross-border transactions, by harmonising pricing methodologies across jurisdictions. Their role in removing compliance burdens and addressing complex issues such as the valuation of intangibles and inter-company loans has made APAs indispensable in an increasingly globalised economy.

Challenges

Despite its success, India’s APA program has faced certain challenges. The timeframes for concluding APAs are often lengthy, particularly for bilateral and multilateral agreements, due to the involvement of multiple tax authorities. Apart from the processing timelines, some of the major challenges include:

Lengthy Negotiation Process: The process often takes 2–3 years to finalise, even though the objective is to provide timely certainty. This is due to the complexity of cases, resource constraints, and extensive review periods.

Resource Constraints At CBDT: The APA teams are often understaffed, leading to delays in processing and resolving applications. This reduces the framework’s efficiency and increases the number of pending cases.

High Costs for Taxpayers: The APA application and negotiation process can be costly, particularly for small and mid-sized enterprises.

Integration Of Multilateral APAs: Coordination between Indian tax authorities and foreign counterparts can be challenging, particularly in jurisdictions with differing interpretations of TP principles. As India has not signed any multilateral agreements, there needs to be more development on the aspect of MAPAs. By effectively using the MAPAs, the TP landscape can be set straight significantly.

The Future of APAs in India: Suggestions for Improvement

The Indian APA regime has made significant strides in addressing TP complexities, yet key areas for improvement remain to ensure its long-term effectiveness and worldwide competitiveness.

Adopting effective practices from mature jurisdictions, such as technology integration and increased focus on MAPAs, could further refine the APA process. Integrating technology and implementing robust e-filing systems would streamline application handling by reducing manual inefficiencies and expediting the overall process. Additionally, enhancing the pre-filing consultation process by making it more efficient and transparent would encourage greater participation while setting a clear foundation for formal APA discussions. These measures would not only save time and resources but also improve the experience for both taxpayers and tax authorities.

Another critical aspect for improvement is strengthening multilateral cooperation with foreign jurisdictions. Streamlining negotiations with foreign tax authorities could significantly reduce the time frame for concluding multilateral APAs, which are inherently more complex than their unilateral counterparts. Strengthening collaboration across global jurisdictions would ensure comprehensive solutions for taxpayers, overall reducing the risk of double taxation and fostering confidence in India’s APA regime as a worldwide competitive alternative.

By addressing these aspects, introducing MAPAs, leveraging technology, refining pre-filing consultations, and enhancing international cooperation, India can establish a more efficient, transparent, and taxpayer-friendly APA framework that aligns with global best practices while catering to the unique needs of its economic landscape.

Conclusion

The APA regime has significantly transformed India’s TP landscape, providing essential predictability and minimising litigation challenges. However, to fully realise its benefits, the program must adapt to current shortcomings, including the limited effectiveness of unilateral APAs. By implementing reforms that enhance efficiency, transparency, and fairness, India can strengthen its appeal as a top choice for multinational corporations seeking tax certainty. This evolution of the APA regime will not only help reduce disputes but also create a more favourable environment for international trade and investment.

However, to credit the rapid improvements over the past decade, India’s APA regime has become a fundamental aspect of modern tax administration, effectively linking regulatory compliance with operational predictability for multinational companies. It has improved tax dispute resolution, decreased litigation, and bolstered investor confidence in India’s tax system.

While challenges remain, such as lengthy timelines and the lack of rollback options, the APA program demonstrates India’s dedication to nurturing a collaborative tax environment. As India works to enhance its APA process and align with global standards, the framework has significant potential to simplify TP compliance, attract foreign investments, and establish the country as a leader in tax innovation worldwide.

End Notes

[i] Ss. 92CC and 92CD of the Income-tax Act.

[ii] S. 9(1)(i) of the Income-tax Act.

[iii] S. 92CC(1)(b) of the Income-tax Act.

[iv] Rule 10F(k) of the Income-tax Rules.

[v] Rule 10F(c) of the Income-tax Rules.

[vi] Rule 10F(h) of the Income-tax Rules.

[vii] S. 92CC(4) of the Income-tax Act.

[viii] S. 92CC(9A) of the Income-tax Act, introduced by Finance (No. 2) Act of 2014.

[ix] Rules 10F to 10T and Rule 44GA of the Income-tax Rules.

[x] S. 92A of the Income-tax Act.

[xi] S.92C read with S.9(1)(i) of the Income-tax Act.

[xii] S. 92CC(5) of the Income-tax Act.

[xiii] S. 92CC(6) of the Income-tax Act.

[xiv] S.92CD of the Income-tax Act.

[xv] Procedure for BAPAs and MAPAs has been prescribed under Rule 44GA of the Income-tax Rules.

[xvi] Rule 10H of the Income-tax Rules.

[xvii] Via Form No. 3CEC.

[xviii] Via Form No. 3CED read with Rule 10I of the Income-tax Rules.

[xix] Via Form No. 3CEE read with Rule 10J of the Income-tax Rules.

[xx] Rule 10K of the Income-tax Rules.

[xxi] Rule 10L of the Income-tax Rules.

[xxii] Rule 10M of the Income-tax Rules.

[xxiii] Rule 10MA of the Income-tax Rules.

[xxiv] S.92E of the Income-tax Act.

[xxv] Rule 10N of the Income-tax Rules.

[xxvi] S.92C(1) of the Income-tax Act.

[xxvii] S.92CC(7) of the Income-tax Act.

Authored by Vanshika, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions.

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.