The Insolvency and Bankruptcy Code (Amendment) Bill, 2025, marks a decisive inflection point in India’s insolvency regime. Moving beyond incremental reform, the Bill hard-codes speed, procedural certainty, and creditor control across the insolvency lifecycle. By narrowing admission-stage discretion, institutionalising creditor-initiated resolution, extending CoC oversight into liquidation, and introducing frameworks for group and cross-border insolvency, the legislature re-engineers how and when insolvency becomes collective. While these changes promise efficiency and value maximisation, they also recalibrate inclusion, defence latitude, and adjudicatory balance. This analysis maps the Bill end-to-end and evaluates whether the Code’s next phase strengthens legitimacy alongside speed.

Introduction

When the Insolvency and Bankruptcy Code, 2016 (‘IBC/Code’) came into force, it did more than consolidate statutes – it recast financial distress as a collective legal problem to be addressed through a single, time-bound process. That foundational move was not merely procedural. It reflected what Ian Fletcher describes as a core normative principle of insolvency law[i]: the transformation of multiple, individual enforcement relationships into a unified process of administration and distribution, anchored in collectivity and equality of treatment as organizing ideas.

At the same time, insolvency law does not operate in a moral vacuum. Donald Korobkin’s principle of inclusion[ii] frames the bankruptcy bargain as one in which all persons affected must be eligible to press their claims and have their interests counted in the design of the system. The principle of inclusion has often been understood as closely aligned with the idea of collectivity[iii], inasmuch as both reject fragmented, individualistic enforcement in favour of a common pool of claims. Read together, these normative claims – inclusion, equality of treatment, and efficiency – provide a useful lens to evaluate whether an insolvency amendment strengthens the Code’s legitimacy even as it pursues speed.

The IBC (Amendment) Bill, 2025 (‘Bill’) would be best understood against this backdrop. Many of its provisions tighten timelines, prescribe procedural triggers, and codify principles that had previously evolved through precedents. The Bill also introduces some ambitious amendments, such as creditor-initiated resolution and group insolvency. In that sense, the Bill is not merely incremental; it reflects an attempt to recalibrate how and when the insolvency process becomes collective and how decisional authority is distributed among institutions, creditors, and professionals.

At the same time, certain amendments tilt the balance of power decisively in favour of financial creditors (‘FC’) and resolution professionals (‘RP’), sometimes at the cost of narrowing the corporate debtor’s (‘CD’) opportunity to present a defence, particularly at the admission stage or during the conduct of the corporate insolvency resolution process (‘CIRP’). The question, therefore, is not whether the Code matures through the addition of rules, but whether these rules preserve the Code’s normative commitments, especially inclusion and non-arbitrary treatment, while continuing to pursue the time-bound outcomes that made the IBC distinctive in the first place.

Amendments at the Admission Stage - Re-defining the Gateway to CIRP

One of the most consequential sets of amendments introduced by the Bill relates to the admission stage of applications under ss. 7, 9, and 10 of the Code, which reflect a legislative attempt to narrow the scope of inquiry at the threshold. Under the existing framework of s. 7(5), the Adjudicating Authority (‘NCLT’) is required to ascertain the existence of a ‘debt’ and ‘default’ and the completeness of the application, while also being guided by judicial interpretation that has permitted a broader enquiry at the admission stage. The Bill substitutes s. 7(5) and inserts two explanations that significantly recalibrate this position[iv].

Expl. I clarify that where the requirements under s. 7(5)(a) are fulfilled, namely, the existence of ‘debt’, occurrence of ‘default’, completeness of the application, and absence of disciplinary proceedings against the proposed RP – no other ground shall be considered for rejecting an application filed under s. 7. This statutorily confines the admission enquiry to the existence of ‘debt’ and ‘default’, excluding considerations beyond these paraments at the threshold.

Expl. II further provides that where a financial institution furnishes a record of default in respect of a financial debt, as recorded with an Information Utility (‘IU’), such record shall be considered sufficient for the NCLT to ascertain the existence of ‘default’ for the purposes of s. 7. This explanation applies only where the applicant is a financial institution and the IU record pertains to a financial debt.

The Bill also strengthens the statutory discipline around timelines at the admission stage. S. 7(5), as substituted, reiterates that the NCLT ‘shall’ pass an order within 14 days of receipt of the application and mandates recording of reasons in writing where such period is exceeded. While the 14-day timeline existed under the earlier framework as well, the Bill replaces the term ‘may’ with ‘shall’, thereby fortifying its mandate character. The proviso permitting rectification of defects is retained but restricted to a single opportunity, to be exercised within 7 days out of the overall 14-day period.

Parallel amendments[v] are introduced in ss. 9(5) and 10(4), requiring the NCLT to record reasons where admission or rejection is not decided within 14 days.

Amendments in Moratorium & Cooperation - Clarifying Boundaries & Expanding Duties

The Bill also introduces targeted clarifications in relation to the scope of the moratorium under s. 14 and the duty to cooperate under s. 19 of the IBC. These amendments address interpretational ambiguities that had emerged through practice and litigation.

S. 14(3)(b) of the IBC already provides that the moratorium under s. 14(1) does not apply to a surety in respect of a contract of guarantee. The Bill inserts an explanation[vi] to s. 14(3)(b) clarifying that while creditors may proceed against a surety during CIRP, the surety itself is barred from initiating or continuing any action or proceedings against the CD during the moratorium period. Operating ‘for the removal of doubts’, the explanation makes it clear that the moratorium under s. 14(1) continues to protect the CD from proceedings initiated by a surety, notwithstanding the exclusion carved out for creditor actions against guarantors. This clarification resolves an interpretational gap without altering the substantive position that guarantor liability remains independent of the CIRP of the CD.

The second major amendment appears in s. 19, which is amended by substituting its marginal heading from ‘Personnel’ to ‘Persons’ and by widening the class of individuals bound by the duty to cooperate with the interim RP or RP, as the case may be[vii]. The amended s. 19(1) now applies not only to personnel, promoters, and persons associated with the management of the CD, but also to persons engaged under a contract for service with the CD. According to the Notes on Clauses, this expansion is intended to ensure ‘constructive cooperation’. Accordingly, the amendments to ss. 14 and 19 are clarificatory in form but structural in effect.

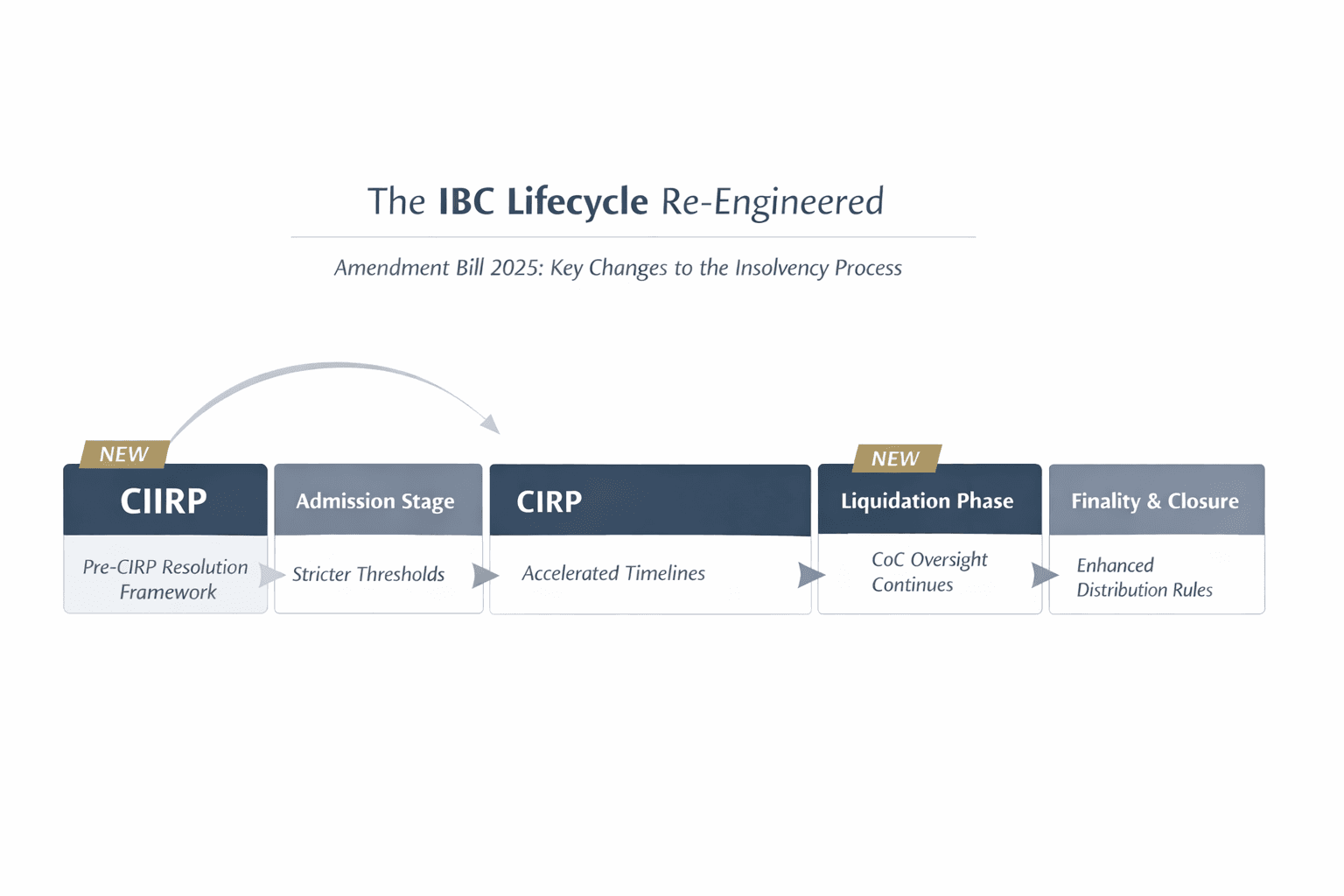

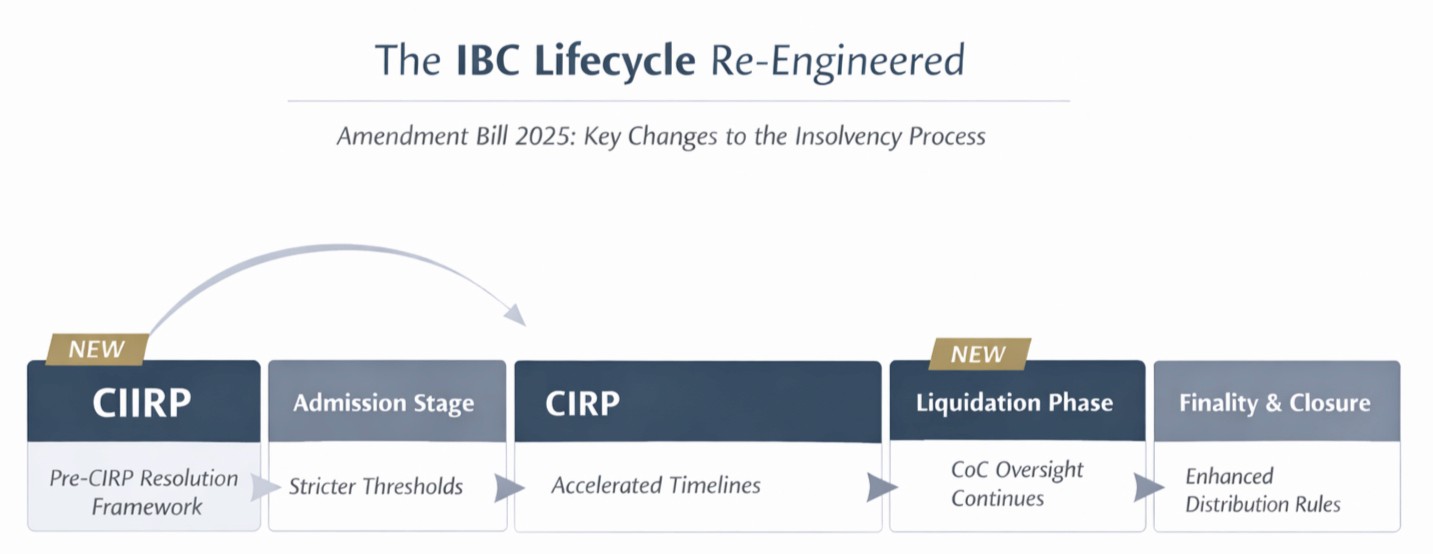

Restructuring CIRP & Extending CoC Oversight into Liquidation

One of the most noteworthy structural shifts proposed by the Bill is the extension of the supervisory role of the committee of creditors (‘CoC’) beyond CIRP and into the liquidation stage. Under the existing framework of the IBC, s. 21 governs the constitution and functioning of the CoC during CIRP, whereas liquidation under ch. III is primarily administered by the liquidator, subject to approvals of the NCLT for specific actions.

The first structural change is effected through the insertion of s. 21(11)[viii], which provides that where liquidation is initiated under ch. III, the CoC constituted under s. 21 shall continue to supervise the conduct of the liquidation process by the liquidator. The provision further clarifies that ss. 21 and 24 shall apply to liquidation, mutatis mutandis, subject to the context. The Notes on Clauses indicate that this amendment is intended to preserve institutional continuity by enabling the CoC – already familiar with the CD’s financial and commercial realities – to oversee liquidation, rather than allowing the process to operate as a standalone, administrator-centric phase.

A consequential restructuring is introduced in s. 33 through the insertion of sub-sections (1A) and (1B)[ix]. Under the amended provision, where the NCLT is satisfied that grounds for liquidation exist under s. 33(1), it is required, prior to passing a liquidation order, to consider an application by the CoC (approved by not less than 66% voting share) seeking restoration of CIRP. The restored CIRP may recommence either from the stage of invitation of resolution plans or from such other stage as the NCLT deems appropriate, depending on whether the failure relates to non-receipt or rejection of plans. The revived process is expressly capped at a maximum duration of 120 days. S. 33(1B) further clarifies that restoration of CIRP may be permitted only once.

Further, the Bill omits ss. 38 to 42 of the IBC[x], which presently govern the submission, verification, admission, and determination of claims during liquidation. This omission is accompanied by corresponding changes to s. 35[xi] and related provisions, signalling a shift away from a distinct liquidation-stage claims mechanism. The Notes on Clauses clarify that the intent is to avoid duplication of claim verification and adjudication by aligning liquidation claims with those already determined during CIRP.

Another important change concerns the timeline for completing liquidation. S. 33, read with s. 54 as amended[xii], now contemplates that liquidation should ordinarily be completed within 180 days from the liquidation commencement date, extendable by a further period of 90 days only once, upon sufficient cause.

Guarantor Assets & Liabilities – Statutory Integration & Expanded Exposure

The Bill introduces a new s. 28A, marking a significant statutory intervention in the treatment of guarantor assets during the CIRP of a CD. Under the existing Code, the assets of a guarantor and those of the CD are treated as distinct estates, enforceable through independent legal processes.

S. 28A[xiii] provides that where a creditor has taken possession of an asset of a personal guarantor or corporate guarantor by enforcement of its security interest under any applicable law, and such enforcement permits transfer of the asset, the creditor may, during the CIRP of the CD, permit the transfer of such asset as part of the insolvency resolution process, subject to prior approval of the CoC.

Where the guarantor is a corporate guarantor undergoing its own insolvency or liquidation process, the approval of the CoC of such corporate guarantor (by not less than 66% voting share) is additionally required. Where the guarantor is a personal guarantor undergoing insolvency or bankruptcy proceedings, approval by a majority of more than three-fourths in value of the creditors of the personal guarantor is mandated.

S. 28A(3) expressly provides that the amount realized from such transfer shall be adjusted towards the debt owed by the guarantor, and any surplus remaining after such adjustment shall be returned to the guarantor.

A separate but related set of amendments concerns the interim moratorium applicable in individual insolvency proceedings. S. 96(1) presently provides that upon filing an application under ss. 94 or 95, an interim moratorium applies in respect of all debts of the individual debtor. The Bill inserts s. 96(4), clarifying that the interim moratorium under s. 96 shall not apply to a personal guarantor to a CD[xiv]. A corresponding amendment is made to s. 124[xv], which governs the fresh start process, mirrors the same exclusion for personal guarantors of CDs.

Creditor-Initiated Resolution – The New Chapter IV-A

One of the most ambitious amendments proposed by the Bill is the introduction of a new ch. IV-A, which introduces a Creditor-Initiated Insolvency Resolution Process (‘CIIRP’)[xvi]. Until now, the IBC recognized only 3 statutory entry points into corporate insolvency resolution: applications by FCs under s. 7, by operational creditors (‘OC’) under s. 9, and by the CD itself under s. 10.

Ch. IV-A introduces an additional and distinct route, enabling specified classes of FCs to initiate a resolution process without invoking the standard CIRP framework under ch. II at the outset. The eligibility of CDs for CIIRP, as well as the class of FCs entitled to initiate such a process, is to be notified by the Central Government in accordance with s. 58A.

Under s. 58B, a CIIRP may be initiated by an FC belonging to a notified class of financial institutions, subject to the fulfilment of prescribed thresholds and procedural safeguards. These include obtaining prior approval of FCs representing not less than 51% in value of the debt, issuing prior intimation to the CD with an opportunity to make representations, and securing reaffirmation of creditor approval after consideration of such representations.

Unlike CIRP, the commencement of CIIRP does not automatically displace the existing management of the CD. S. 58F expressly provides that, during the CIIRP period, management of the affairs of the CD continues to vest in its board of directors or partners, as the case may be. At the same time, an RP appointed under s. 58B exercises supervisory powers, including attendance at board and committee meetings and the authority to reject resolutions, subject to prescribed conditions.

The CIIRP is expressly structured as a time-bound process. S. 58D prescribes an outer limit of 150 days for completion of the process, extendable once by a maximum of 45 days with approval of the CoC by not less than 66% voting share. The RP’s functions under s. 58E are primarily facilitative and supervisory. These include calling for claims, preparing the information memorandum, and ensuring compliance of the resolution plan with ss. 29A and 30, and filing reports with the NCLT and the Insolvency and Bankruptcy Board of India (‘IBBI’). The CoC retains decision-making authority in relation to approval of the resolution plan, consistent with the creditor-driven framework of the IBC.

A key feature of ch. IV-A is its built-in escalation mechanism. S. 58H provides that where no resolution plan is approved within the prescribed period, where the CD or its personnel fail to cooperate, or where the resolution plan is rejected by the NCLT, the CIIRP shall be converted into a CIRP. Upon such conversion, the NCLT is empowered to determine the stage from which the CIRP shall commence, after considering any recommendation of the CoC in this regard. The statute further deems such a conversion order to be an order of admission under s. 7, thereby removing the need for a fresh insolvency application.

Group Insolvency – New Framework for Coordinated Resolution

The Bill also introduces a statutory framework for group insolvency by inserting a new ch. V-A into the Code[xvii]. The absence of an express legislative mechanism for addressing insolvency of corporate groups has been a longstanding structural gap, particularly where multiple entities are linked through ownership, management, guarantees, or operational interdependence.

Ch. V-A enables the initiation of insolvency resolution processes in respect of more than one CD belonging to the same group, in such manner and subject to such conditions as may be prescribed. The determination of what constitutes a ‘group’ is left to subordinate legislation, to be specified by rules made under the Code. The chapter does not mandate collective insolvency by default. Instead, it provides a procedural framework through which coordination among group entities may be achieved, while preserving the separate legal identity of each CD.

This objective is sought to be achieved by empowering the NCLT to order coordination of proceedings involving group entities, which may include joint hearings, alignment of timelines, appointment of a common RP or liquidator, coordinated CoC meetings, and other procedural arrangements aimed at efficient conduct of proceedings.

Resolution Plan Architecture Reworked – Amendments to SS. 30 & 31

The Bill introduces significant changes to the statutory architecture governing resolution plans through amendments to s. 30, which regulates examination and approval of resolution plans by the RP and the CoC, and s. 31, which governs approval of resolution plans by the NCLT. Under the existing framework of s. 30(2), a resolution plan was required to satisfy multiple minimum-payment conditions covering both OCs and dissenting FCs.

The Bill restructures s. 30(2) to provide clearer textual segregation of these obligations. S. 30(2)(b), as amended, now deals exclusively with OCs and continues to mandate that they receive an amount not less than what would be payable to them in liquidation under s. 53. The payment requirement in respect of dissenting FCs is removed from s. 30(2)(b) and placed into a newly inserted s. 30(2)(ba)[xviii].

S. 30(2)(ba) provides that a resolution plan must ensure that dissenting FCs receive not less than the lower of (i) the amount payable to them in accordance with s. 53 in the event of liquidation, or (ii) the amount that would have been paid to them if the resolution plan distribution were made in accordance with the priority under s. 53.

Expl. I clarify that a distribution made in accordance with s. 30(2)(ba) shall be deemed to be fair and equitable. Expl. II provides that the amended payment structure applies prospectively and does not affect CIRPs where the CoC has already approved a resolution plan, resolved to liquidate the CD, or where a liquidation order has already been passed.

Amendments to s. 31 introduce a bifurcated approach to approval and implementation of resolution plans[xix]. A proviso inserted to s. 31(1) empowers the NCLT, on an application by the RP with the approval of the CoC by not less than 66% voting share, to first approve the implementation of the resolution plan and thereafter approve the manner of distribution provided in the plan within 30 days from the date of approval of implementation.

The statutory consequence of this sequencing is clarified to be that even where implementation is approved prior to approval of distribution, the resolution plan remains binding on all stakeholders in terms of s. 31. The moratorium under s. 14 is stated to continue to operate until the resolution process is fully concluded, including approval of distribution.

The more substantive changes to s. 31 are effected through the insertion of ss. 31(5) and (6), which statutorily recognize and codify the consequences of plan approval. S. 31(5) provides that where a resolution plan has been approved, any licence, permit, registration, quota, concession, clearance, or similar grant or right issued by the Central Government, State Government, local authority, sectoral regulator, or any authority constituted under law shall not be suspended or terminated during the remaining period of such grant or right, provided the obligations thereunder are complied with.

S. 31(6) stipulates that upon approval of a resolution plan under s. 31(1), all claims against the CD or its assets which are not part of the resolution plan shall stand extinguished, and no proceedings shall be continued or instituted in respect of such claims. Expl. I preserves the liability of former promoters, persons in management or control, guarantors, and persons with joint or several liability. Expl. II clarifies that where a person with joint or several liability discharges a debt after plan approval, any right of indemnification against the CD shall stand extinguished.

Avoidance Transactions – Timelines, Standing, and Uninterrupted Continuity

The Bill introduces a set of targeted but consequential reforms to the avoidance transaction framework under the Code. These amendments operate across ss. 26, 43, 46, 47, and 66, and address long-standing structural issues in the prosecution and continuation of avoidance proceedings.

S. 26, as substituted, clarifies that the filing, pendency, or adjudication of applications relating to avoidance transactions or fraudulent or wrongful trading shall not affect the continuation or completion of CIRP or liquidation, and conversely, that completion of CIRP or liquidation shall not affect the continuation of such proceedings. This amendment statutorily decouples avoidance proceedings from the lifecycle of the main insolvency process[xx].

The Bill amends ss. 43, 46, and 50 to align the look-back period for preferential, undervalued, and extortionate transactions with the ‘initiation date’ rather than the insolvency commencement date[xxi]. Further, the Bill clarifies, by insertion of a proviso to s. 5(11), that where multiple CIRP applications are pending, and one is admitted, the initiation date shall be the date on which the first application was made[xxii].

A major structural amendment is introduced through the substitution of s. 47[xxiii]. Where a RP or liquidator fails to file an application in respect of a preferential, undervalued, extortionate, or fraudulent or wrongful transaction, any creditor, member, or partner of the CD may independently apply to the NCLT. Where such an application succeeds, the NCLT may also direct the IBBI to initiate disciplinary proceedings against the RP or liquidator for failure to act despite having sufficient information. This amendment significantly alters the locus of control over avoidance proceedings.

Clarity on Who is Secured – Definitional Amendments

In insolvency, distribution priorities frequently turn on whether a creditor holds a ‘security interest’ within the meaning of the Code. The Bill proposes a targeted clarification to the definition of ‘security interest’ in s. 3(31) to address recurring disputes where government departments and other authorities have asserted ‘secured’ status on the basis of statutory charges under non-IBC laws[xxiv].

The Bill also inserts an explanation under s. 53(1)(e)(i) clarifying that amounts due to the Central Government or State Government for the two years preceding the liquidation commencement date shall be distributed under s. 53(1)(e)(i), and any remaining amount under s. 53(1)(f), whether or not a security interest is created to secure such amount[xxv]. This appears to directly complement the clarification to s. 3(31) and is aimed at preventing government dues from being elevated in the distribution waterfall through assertions of statutory security.

Digital Infrastructure & Cross-Border Insolvency - Making the IBC Future-Proof

The Bill introduces enabling provisions aimed at modernising the administration of insolvency processes, including the establishment of an electronic portal for insolvency and bankruptcy processes and a rule-based framework for administering cross-border insolvency proceedings[xxvi].

The Bill inserts a new s. 240B in Part V of the Code. Proposed s. 240B empowers the Central Government, by notification, to provide an electronic portal and to specify procedures for insolvency and bankruptcy processes under the Code that shall be carried out on such portal. The Bill leaves the operational architecture, i.e., which processes must be carried out electronically and in what manner, to delegated legislation.

The Bill also inserts a new s. 240C, which empowers the Central Government to prescribe rules relating to cross-border insolvency proceedings for administering and conducting such proceedings under the Code, for such class or classes of CDs as may be notified. S. 240C further contemplates that such rules may provide for the application of provisions of the Code and/or the Companies Act, 2013, with such exceptions, modifications, and adaptations as may be required, including designation of one or more Benches to deal with such proceedings. The provision also introduces a draft-rule laying requirement before both Houses of Parliament prior to issuance of the rules.

Conclusion – A Code that Matures

The Bill marks a decisive phase in the maturation of India’s insolvency framework. While it does not disturb the foundational objective of the Code – time-bound resolution and value maximization – it reconfigures the mechanisms through which that objective is pursued. Read as a whole, the amendments reflect a legislative shift away from an isolated, event-centric understanding of insolvency towards a continuum-based model, where early intervention, creditor supervision, procedural certainty, and post-resolution finality are treated as interlinked statutory priorities.

The legislative evolution of the Bill reflects a sustained and consultative reform process, with its core architecture traced to the discussion paper released in January 2023[xxvii], which invited public comments on proposals concerning admission thresholds, creditor-driven resolution, liquidation design, group insolvency, cross-border insolvency, and digital infrastructure. Following stakeholder feedback, deliberations of the Insolvency Law Committee, and sector-specific consultation papers issued by the IBBI[xxviii], these proposals were refined and introduced as a consolidated legislative package in 2025, with a substantial proportion of the 2023 proposals finding direct and substantive expression in the present Bill.

The introduction of the CIIRP is symbolic of this shift. CIIRP adopts a management-in-possession model with creditor and professional oversight, in contrast to the management-displacing structure of CIRP. The statutory design embeds safeguards at each stage – prior creditor approvals, debtor representations, supervisory powers of the RP, and a clear escalation pathway into CIRP – thereby attempting to balance debtor continuity with creditor control. Notably, CIIRP operates as a preliminary resolution framework rather than a parallel regime, crystallizing the Code’s emphasis on early intervention without creating procedural dead ends.

At the same time, the amendments at the admission stage significantly narrow the scope of inquiry by confining the NCLT’s assessment to the existence of debt and default, and by elevating IU records as sufficient evidence of default in cases involving financial institutions. While these changes are aimed at reducing delay and standardize threshold scrutiny, they also curtail adjudicatory discretion at the gateway to CIRP. From a defence perspective, the near-decisive status accorded to IU records raises concerns in cases where defaults are disputed on nuanced factual or contractual grounds that may not be fully or accurately captured in such records. The promise of efficiency must therefore be carefully balanced against the risk of an overly mechanical admission process.

The extension of CoC supervision into liquidation represents another important recalibration. By continuing creditor oversight beyond CIRP and introducing a limited, one-time window for restoration of CIRP prior to liquidation, the Bill acknowledges that liquidation has often suffered from diminished commercial direction. These changes reposition liquidation as a supervised and, in limited circumstances, reversible phase, without undermining its finality.

Similarly, the guarantor-related amendments, the group insolvency framework, the independence of avoidance proceedings, definitional clarity on secured claims, and the enabling framework for digital and cross-border insolvency collectively enhance institutional coherence. The introduction of s. 240C, in particular, signals a move away from the constrained bilateral approach under ss. 234 and 235, aligning India’s framework with emerging cross-border practice. While the Bill does not expressly refer to any judicial developments, its timing and design appear to be consistent with recent recognition of Indian CIRP proceedings abroad by the Singapore High Court in Re Compuage Infocom Ltd.[xxix].

Overall, the Bill reflects a legislature responding to experience. Whether this recalibration succeeds will depend on how these provisions are interpreted and applied in practice, specifically, whether the Code can remain collective without becoming exclusionary, and efficient without becoming arbitrary. That balance will determine whether the IBC’s next phase develops not only its speed but also its legitimacy.

End Notes

[i] Ian F. Fletcher, Insolvency in Private International Law, 2nd ed. 2005, Oxford University Press.

[ii] Donald R. Korobkin, Contractarianism and the Normative Foundations of Bankruptcy Law, (1993) 71 Texas Law Review 541 at 543.

[iii] Sandeep Gopalan & Michael Guihot, Cross-Border Insolvency Law (LexisNexis, 2016).

[iv] IBC (Amendment) Bill, 2025, cl. 4 (substituting s. 7(5) and inserting Explanations I & II).

[v] IBC (Amendment) Bill, 2025, cl. 5(b) and cl. 6(b)(iii) (amendment to s. 9(5) and s. 10(4), respectively).

[vi] IBC (Amendment) Bill, 2025, cl. 9(b) (insertion of Explanation to s. 14(3)(b)).

[vii] IBC (Amendment) Bill, 2025, cl. 12 (amendments to s. 19).

[viii] IBC (Amendment) Bill, 2025, cl. 13 (insertion of s. 21(11): CoC supervision of liquidation).

[ix] IBC (Amendment) Bill, 2025, cl. 20(b) (insertion of ss. 33(1A) & 33(1B): restoration of CIRP).

[x] IBC (Amendment) Bill, 2025, cl. 25 (omission of ss. 38-42).

[xi] IBC (Amendment) Bill, 2025, cl. 23 (consequential amendment to s. 35).

[xii] IBC (Amendment) Bill, 2025, cl. 33(a) (amendment to s. 54 – 180-day, extendable by 90 days’ timeline).

[xiii] IBC (Amendment) Bill, 2025, cl. 17 (insertion of s. 28A).

[xiv] IBC (Amendment) Bill, 2025, cl. 47 (insertion of s. 96(4)).

[xv] IBC (Amendment) Bill, 2025, cl. 51 (corresponding amendment to s. 124).

[xvi] IBC (Amendment) Bill, 2025, cl. 40 (introduction of CIIRP in ch. IV-A).

[xvii] IBC (Amendment) Bill, 2025, cl. 42 (introduction of Group Insolvency in ch. V-A).

[xviii] IBC (Amendment) Bill, 2025, cl. 18 (amendments in s. 30).

[xix] IBC (Amendment) Bill, 2025, cl. 19 (amendments in s. 31).

[xx] IBC (Amendment) Bill, 2025, cl. 16 (amendment in s. 26).

[xxi] IBC (Amendment) Bill, 2025, cl. 26, 27, and 30 (look-back period in ss. 43, 46, and 50).

[xxii] IBC (Amendment) Bill, 2025, cl. 3(c) (insertion of proviso to s. 5(11)).

[xxiii] IBC (Amendment) Bill, 2025, cl. 28 (substitution of s. 47).

[xxiv] IBC (Amendment) Bill, 2025, cl. 2(a) (clarification to the definition of ‘security interest’).

[xxv] IBC (Amendment) Bill, 2025, cl. 32(a) (explanation to s. 53).

[xxvi] IBC (Amendment) Bill, 2025, cl. 67 (electronic portal & cross-border insolvency).

[xxvii] Ministry of Corporate Affairs, Discussion Paper on Changes Being Considered to the IBC (18.01.2023).

[xxviii] IBBI, Discussion Paper on Streamlining Processes under the Code (04.02.2025).

[xxix] Re Compuage Infocom Ltd & Anr., [2025] SGHC 49, dated 24.03.2025.

Authored by Srishty Jaura, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions.

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.