Introduction

In the complex landscape of international trade and finance, three critical regulatory frameworks – transfer pricing (‘TP’), Customs Special Valuation Branch (‘SVB’) pricing, and the Foreign Exchange Management Act, 1999 (‘FEMA’) – play pivotal roles. These frameworks intersect at various points, impacting cross-border transactions, taxation, and regulatory compliance.

TP refers to pricing goods, services, or intangibles exchanged between related entities within multinational corporations (‘MNCs’). It aims to ensure that transactions between these entities are conducted according to the arm’s length principle/price (‘ALP’) – as if they were independent, unrelated parties. TP regulations prevent profit shifting and tax evasion by establishing fair market values (‘FMV’) for intra-group transactions.

Following closely, Customs SVB pricing (‘customs valuation’) pertains to the valuation of imported goods for customs purposes. When the declared transaction value is deemed unreliable due to related-party relationships, customs authorities invoke SVB provisions. SVB determines the appropriate value based on comparable transactions or alternative methods, ensuring accurate duty assessment.

FEMA governs foreign exchange transactions in India and regulates cross-border payments, capital flows, and external commercial borrowings[i] (‘ECBs’). It aims to maintain stability in the foreign exchange market, facilitate trade, and prevent illicit fund transfers.

Navigating the TP Maze

TP provisions, governed by the Income-tax Act, 1961 (‘IT Act’) based on the OECD mandate, are rooted in the principle of fairness. When related entities within MNCs engage in cross-border transactions, they must do so as if they were independent parties operating at arm’s length. This arm’s length standard ensures that prices for goods, services, or intangibles are realistically reflected in market realities rather than internal affiliations, promoting integrity and equity in transactions.

To understand the ALP, we look at two aspects: comparable transactions and functional analysis. TP regulations require companies to compare their intra-group transactions with similar transactions between unrelated parties. If the prices deviate significantly, adjustments are necessary to align them with market rates. Functional analysis involves understanding each entity's functions, risks, and assets (‘FAR’), informing the determination of an appropriate profit allocation.

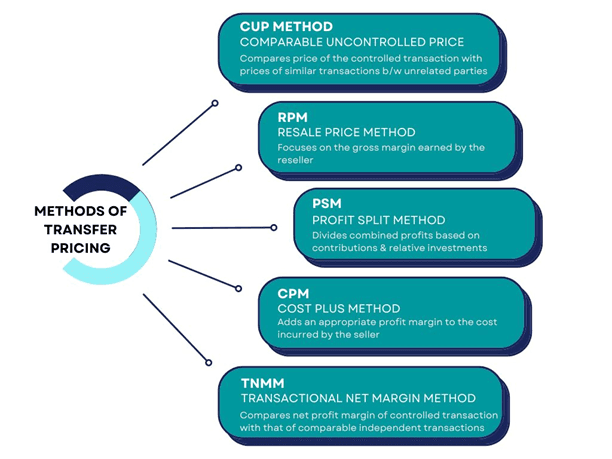

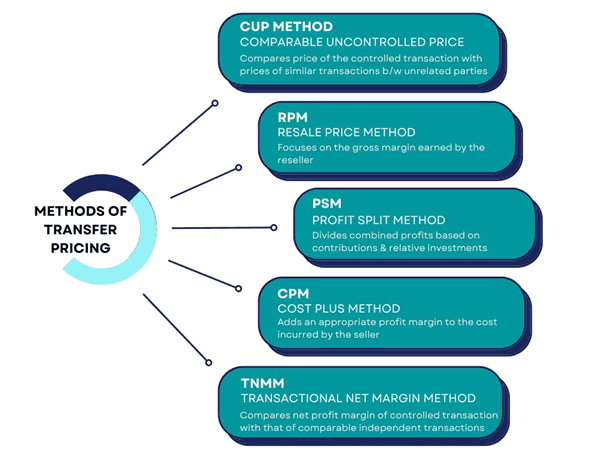

The TP law prescribes six methods for the determination of ALP. These include the comparable uncontrolled price (‘CUP’) method, resale price method (‘RPM’), cost plus method (‘CPM’), profit split

method (‘PSM’), transactional net margin method (‘TNMM’), and a residuary other method. These methods provide a mathematical, step-by-step guideline on how to calculate the ALP through a comparability analysis, factoring in business and geography-specific variables.

Transactions not conducted on an arm’s length basis are price-adjusted under the TP law to nullify the effect on the determination of tax. For instance, an overvalued import purchase would result in lesser profits. Upon a TP analysis, such import purchase would result in an adjustment being made by the tax authorities to bring true and accurate profits to tax.

A Look at Customs Valuation

The SVB is a unit of the Indian customs authorities investigating the valuation of goods during imports between related parties. This authority is located in the metro cities of Mumbai, Delhi, Chennai, and Kolkata. Its primary task is to verify that the relationship between such parties has not influenced the transaction value. This examination ensures that goods supplied by an external supplier to a related importer in India are invoiced at an ALP and not undervalued to reduce customs duty liability.

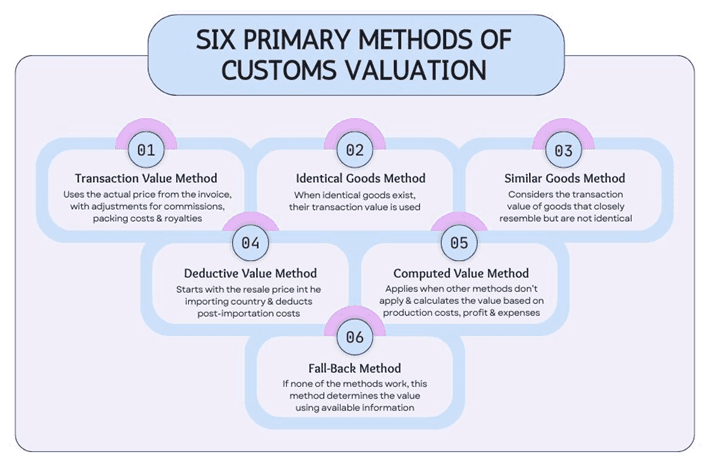

The Customs Valuation (Determination of Value of Imported Goods) Rules, 2007 (‘CV Rules’) lay out methods and principles for determining the valuation. The CV Rules replaced the CV Rules, 1988, and are

governed by the Customs Act, 1962, based on the WTO mandate[ii]. However, aligning customs valuation with TP presents unique challenges.

In the case of Ferodo India[iii], the Supreme Court acknowledged that the foundational basis of the erstwhile CV Rules of 1988 was rooted in a. VII of the General Agreement on Tariffs and Trade, 1994 (GATT). It was noted that this article introduced the concept of ALP in customs valuation, thereby providing methods to test values derived from the sale of identical or similar goods. Where such values were not ascertainable, the CV Rules provided for the deductive and computed value methods to be applied, which are similar to the RPM and CPM under the TP regime. The Court further clarified that the CV Rules essentially mandate a hierarchy of valuation methods, which must be followed when transfer prices are rejected.

Bird’s Eye View of the Interplay between TP, Customs Valuation & FEMA

Regarding the divergence in objectives of the three, while proper TP ensures that profits are fairly allocated among jurisdictions, preventing base erosion and profit shifting (‘BEPS’), customs valuation prevents the undervaluation or overvaluation of imported goods, ensuring accurate customs duties. SVB streamlines customs procedures, promoting efficient cross-border trade. FEMA facilitates cross-border business expansion by allowing capital movement and supervising foreign investments, ECBs, and remittances, impacting India’s overall economic stability. Transparent TP practices align pricing with market realities and reduce legal and reputational risks for MNCs. To understand better, while tax authorities focus on margin comparison for TP purposes, customs authorities pay attention to pricing comparisons that demonstrate the actual transaction values.

It is clear that TP regulations come into play in every cross-border transaction resulting in income generation between related entities, while customs valuation applies to all exports and imports but is only invoked when there is doubt of undervaluation or if the Customs Department feels that the declared price for customs duty purposes does not reflect the actual prices at the time of the transaction. On the other hand, FEMA is invoked not just with related entity transactions but also with every exchange or remittance of currency across borders. Hence, from a bird’s eye, FEMA has the broadest scope among the three regimes, while customs valuation has the narrowest scope of application.

Worm’s Eye View of the Interplay between TP & Customs Valuation

While tax authorities dealing with TP matters in the importing country may perceive the prices of goods as too high, thereby decreasing taxable profit, customs authorities may simultaneously challenge the prices as too low, thus decreasing customs duties. A key challenge for businesses that import goods is that customs authorities are unfamiliar with the technical aspects of TP methodologies and the practical approaches applied by taxpayers when pricing goods[iv]. While both TP and customs valuation aim to ensure no conflict of interest between related parties, the authorities handling these matters often have conflicting interests.

In a case involving Fuchs Lubricants (India) (P) Ltd.[v], one of the grounds contested was that the value of raw material imports accepted by the Customs authorities should be regarded as the ALP. The Income Tax Appellate Tribunal (‘ITAT’) rejected this contention. It held that the valuation determined by the Customs authorities cannot be directly used to determine the ALP under the provisions of the IT Act. In another case, Panasonic Consumer India v. ACIT[vi], the ITAT addressed the assessee’s reliance on the SVB’s valuation of the imports from a related entity. The Tribunal held that customs valuation and TP regulations under the IT Act served different purposes and applied different criteria. It was held that specific rules of law within the IT Act took precedence over other valuations, including those by the Customs authorities. The ITAT found that ch. X of the IT Act and the rules made thereunder were self-contained and provided all necessary answers regarding valuation issues. These decisions highlight the distinction between customs valuation and TP regulations, emphasizing that these serve different objectives and use different criteria.

In contrast, in ACIT v. Caparo Engineering India Pvt. Ltd.[vii], the ITAT upheld the impugned order that deleted the additions made by the TP officer. The grounds for the TP officer to make the additions that were challenged were that the FMV certified by the Chartered Engineer, even if accepted by the customs authorities, did not necessarily fulfil TP principles. Although the method used by the TP officer was scrutinized and adjudicated upon by the Tribunal, no express observations were made regarding the TP officer’s argument that the purposes of valuation under CA62 and the determination of the ALP under the TP regulations are distinct and separate functions and therefore, using the transactional value certified by customs authorities as the ALP under the TP regulations is neither fair nor reasonable. To support this argument, the TP officer relied on the Supreme Court’s decision in the case of Associated Cement Companies[viii], wherein a distinction was drawn between the value of imported goods and the price of such goods. However, the Central Board of Indirect Taxes and Customs (CBIC) states[ix] that the transfer price may be used as a starting point in related party transactions where both parties have a separate legal identity. This clarifies that while the transfer price determined by the TP officer can be considered, customs authorities are not bound to accept the same without further verification and possible adjustments.

Furthermore, the ITAT has addressed the reliance on customs data instead of customs valuation for TP purposes in a series of cases. In Louis Dreyfus Company[x], the Tribunal found customs data more reliable for the CUP method adjustments, emphasizing its comprehensive nature and alignment with the OECD guidelines. Cases such as Sinosteel India[xi], Coastal Energy[xii], Rohm and Haas[xiii], and Tilda Riceland[xiv] supported this stance, validating customs data for accurate TP adjustments. Conversely, in Mobis India[xv]* *and Kodak Polychrome Graphics[xvi], the ITAT rejected customs data, noting the misalignment with TP analysis requirements and the lack of proper comparability analysis.

Another divergence between TP and customs valuation lies in their methodologies. Both methods are either descriptive, focusing on ‘what is,’ normative, focusing on ‘what should be’, or a combination of both. As illustrated above, TP has 6 prescribed methods, and the assessee has the option to select any method without adhering to a particular sequence. In contrast, customs valuation requires the importer to reject each method sequentially before proceeding to the next. Another practical divergence between the two pertains to timing and documentation. TP documentation requirements are extensive, including MFs, local files, and CbCRs, while documentation in customs valuation focuses on transaction value, ensuring compliance with customs regulations during import or export.

A landmark case in this regard is the Hamamatsu case[xvii], whereby the European Court of Justice (‘ECJ’) was tasked with addressing a critical intersection between TP and customs valuation. Hamamatsu, a German subsidiary of a Japanese MNC, imported goods from its parent company using intra-group prices established under an APA with German tax authorities. These prices were adjusted post-facto to comply with ALP as per the OECD guidelines. Following an adjustment that resulted in a significant credit, Hamamatsu sought a customs duty refund, which the Munich Principal Customs Office rejected. The ECJ ruled that the applicable Customs Code did not permit the use of an agreed transaction value, composed of an initially invoiced amount and a flat-rate adjustment made post-accounting period, for customs valuation purposes. It emphasized the need for customs value to reflect the real economic value of imported goods, excluding arbitrary or fictitious valuations. This decision clarified that while TP adjustments are permissible for tax purposes under the OECD guidelines, they cannot retroactively alter customs valuation without specific, immediate cause relating to the goods’ condition or unforeseen defects.

FEMA’s Influence on TP & Customs Valuation

FEMA’s regulations significantly influence TP and customs valuation processes. Imports of goods and services are permitted[xviii] under s. 5 of the FEMA, regulated by the Directorate General of Foreign Trade (‘DGFT’). When converting foreign currency amounts to Indian rupees, FEMA guidelines come into play. The exchange rate must be consistent with market rates to avoid distortions in TP calculations. Further, FEMA mandates reporting such foreign exchange transactions, including those related to TP. Entities engaged in cross-border trade must submit periodic returns to the Reserve Bank of India (‘RBI’). These reports provide insights into the flow of funds, foreign currency borrowings, and remittances, which indirectly impact TP decisions.

FEMA also governs ECBs, and the pricing of ECBs, including interest rates and repayment terms, are subject to FEMA guidelines. These guidelines influence the overall cost of capital for Indian companies, impacting their TP strategies. FEMA also regulates the repatriation of profits and dividends earned by foreign companies operating in India. The timing and method of repatriation affect the cash flow and profitability of Indian subsidiaries, influencing their pricing decisions. Entities involved in cross-border transactions must maintain comprehensive documentation to demonstrate compliance with FEMA regulations. This documentation includes TP studies, foreign exchange contracts, and evidence of ALP. Non-compliance can lead to penalties and adverse tax implications.

The influence of FEMA on TP and customs valuation cannot be understated. Exchange rate fluctuations can affect the valuation of cross-border transactions, impacting both TP and customs valuation regulations. Under FEMA, transactions must be recorded at the exchange rate prevailing on the transaction date, creating discrepancies when there are time gaps between the transaction date, payment date, and customs clearance date.

To ensure compliance, companies should adopt strategies such as integrated financial reporting, regular audits and reviews, collaborative compliance teams, comprehensive documentation, and negotiating advance pricing agreements (‘APA’) or forward contracts to provide clarity and certainty on TP methodologies and lock in exchange rates for future transactions.

Harmonizing the Trio for Seamless Compliance or Appreciating the Differences?

At the outset, it is stated that harmonizing these three regimes for ‘seamless’ compliance is practically impossible because they are distinct regimes with entirely different objectives, methodologies, regulatory authorities, etc. Hence, it would be like comparing apples, oranges, and pears. While all three are fruits with some common benefits, they are essentially different, and one cannot replace the other. Therefore, instead of forcefully aligning them, it is preferable to appreciate their intersections and study them to harmonize the conflicts peculiar to each case’s facts and circumstances.

However, to reduce friction between the three regimes, a unified valuation framework that integrates the requirements of TP, SVB, and FEMA would provide a consistent basis for valuing cross-border transactions. Enhanced coordination and information sharing between tax authorities, customs officials, and foreign exchange regulators would be essential in reducing such friction. Joint audits and cross-training of regulatory personnel could foster a more cohesive approach to enforcement and compliance.

International organizations like the OECD and WTO play a pivotal role in this regard. By developing and promoting international standards, such as the OECD’s TP Guidelines and the WTO’s Customs Valuation Agreement (‘CVA’), these organizations set benchmarks for national policies. The CVA primarily uses the transaction value method, aligning with internationally accepted pricing principles. Internationally accepted pricing methodologies, often based on the discounted cash flow (‘DCF’) approach, determine the fair value of assets, securities, or businesses. It considers future cash flows, risk factors, and growth prospects to arrive at a present value. While it is not directly tied to customs valuation or TP, it provides a robust framework for assessing fair values in cross-border transactions.

Returning to international organizations, they also foster global dialogue through international forums and working groups, enabling countries to share best practices and adopt more harmonized approaches. Additionally, the United Nations Conference on Trade and Development (‘UNCTD’) provides technical assistance and capacity-building programs to developing countries, ensuring that all nations can implement these three regimes in a harmonized manner.

Conclusion

The existing conflict between TP, customs valuation, and FEMA should be viewed from a perspective that does not necessarily require resolution. Considering judicial precedents, one potential approach is for one department’s order to be accepted by another if the assessee has demonstrated compliance with a particular method. The correct flow is Customs to tax authorities, which both run parallel with FEMA compliance. However, this cannot be achieved without involving international organizations.

The interplay between these three regulations forms a fascinating nexus that is the lifeblood of cross-border transactions and shapes global commerce. Adopting a non-conflicting approach to the interplay between the three requires understanding the unique nuances, objectives, and methodologies of each framework. It calls for a delicate balancing act that respects the sovereignty of each regulation while acknowledging their interactions.

By fostering collaboration and sharing information between regulatory bodies and with the support of international organizations, conflicts can be mitigated and the predictability of cross-border trade and compliance enhanced.

End Notes

[i] External Commercial Borrowings (ECBs) encompass various forms of foreign borrowings by Indian entities. These include commercial bank loans, buyers’ credit, suppliers’ credit, securitized instruments (such as Floating Rate Notes and Fixed Rate Bonds), credit from official export credit agencies, and commercial borrowings from Multilateral Financial Institutions. In essence, ECBs provide a means for Indian businesses to raise funds from international sources to meet their financial requirements.

[ii] The World Trade Organization (WTO) mandate refers to the WTO’s Agreement on Subsidies and Countervailing Measures. This agreement disciplines the use of subsidies and regulates actions countries can take to counter the effects of subsidies. Under this mandate, a country can seek the withdrawal of a subsidy or the removal of its adverse effects through the WTO’s dispute-settlement procedure.

[iii] Commissioner of Customs v. Ferodo India (P) Ltd., (2008) 4 SCC 563.

[iv] PWC Newsletter, Customs & Transfer Pricing – There are Solutions for Harmony. Available at: customs-tp.pdf (pwc.com).

[v] Fuchs Lubricants (India) (P) Ltd. v. DCIT, Mumbai, [2014] 44 taxmann.com 284 (Mumbai – Trib.).

[vi] Panasonic Consumer India Private Limited v. ACIT, New Delhi, [2015] 53 taxmann.com 433 (Delhi – Trib.).

[vii] ACIT v. Caparo Engineering India Pvt. Ltd., 2018 SCC OnLine ITAT 6699.

[viii] Associated Cement Companies Ltd. v. Commissioner of Customs, (2001) 4 SCC 593.

[ix] Directorate General of Valuation, CBIC – Frequently Asked Questions (FAQs) – Q41. Available at: https://dov.gov.in/faqs.

[x] Louis Dreyfus Company India (P) Ltd. v. DCIT, [2023] 150 taxmann.com 392 (Delhi – Trib.).

[xi] Sinosteel India Private Limited v. DCIT, [2013] 40 taxmann.com 240 (Delhi – Trib.).

[xii] Coastal Energy (P) Ltd. v. ACIT, [2011] 12 taxmann.com 355 (Chennai – Trib.).

[xiii] Rohm and Haas India (P) Ltd. v. ACIT, [2019] 112 taxmann.com 90 (Mum. – Trib.).

[xiv] Tilda Riceland (P) Ltd. v. ACIT, [2014] 42 taxmann.com 400 (Delhi – Trib.).

[xv] Mobis India Ltd. v. DCIT, [2013] 38 taxmann.com 231 (Chennai – Trib.).

[xvi] Kodak Poilychrome Graphics (I) (P) Ltd. v. ACIT, 2013 SCC OnLine ITAT 4030.

[xvii] Hamamatsu Photonics Deutschland, ECLI:EU: C:2017:984, Judgment dated 20.12.2017.

[xviii] Notified vide Notification No. G.S.R.381(E) dated 03.05.2000.

Authored by Srishty Jaura, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions.

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.