Abstract

The Insolvency and Bankruptcy Code, 2016 (‘IBC’) represents a landmark legal reform in India’s financial ecosystem. It is designed to consolidate and amend the laws relating to insolvency resolution for both corporate entities and individuals. While much of the early focus of the IBC has been on corporate insolvencies, the framework for personal insolvency, though nascent, is equally significant given India’s evolving financial environment and rising personal debt levels. The dynamic and evolving nature of the personal insolvency regime makes it an area of law that is both engaging and interesting.

The personal insolvency regime under the IBC offers a structured path for individuals – debtors burdened by unsustainable financial obligations – to obtain a fresh start while simultaneously providing mechanisms for creditors to recover debts in an orderly fashion. This delicate balance between debtor relief and creditor recovery is not just a legal concept but a practical assurance of the system's fairness. It is crucial to maintain confidence in the credit market, protect the financial system’s integrity, and ensure that individuals are not disproportionately penalized for financial hardship.

Recent judicial pronouncements are pivotal in shaping the contours of personal insolvency law in India. Courts and tribunals have been instrumental in interpreting key provisions of the IBC, particularly in addressing issues related to the scope of personal guarantees, the treatment of joint liabilities, and the alignment of personal insolvency laws with constitutional safeguards. These rulings are not merely academic; they have a profound commercial impact on the rights and obligations of debtors, creditors, and guarantors, underscoring the practical relevance and engaging nature of this information.

This insight seeks to examine and distil the most significant judicial interpretations that have emerged in the context of personal insolvency under the IBC. As the personal insolvency regime continues to evolve, these judicial pronouncements will serve as key reference points, engaging practitioners, policymakers, and stakeholders in the ongoing process of navigating this complex and dynamic area of law.

Personal Insolvency & History

The legal framework governing personal insolvency in India addresses the financial distress of individuals, sole proprietorships, and partnership firms when they are unable to meet their financial obligations to creditors. Historically, personal insolvency laws have played a dual role—first, ensuring that creditors receive a fair distribution of the debtor's assets, and second, providing a social and legal mechanism to protect individuals from undue creditor pressure and societal stigma. The primary aim of such laws is to grant debtors an opportunity for a financial reset or ‘fresh start,’ allowing them to restructure or discharge their debts while maintaining a path toward stability and rehabilitation.

Personal insolvency laws serve a critical function in balancing competing interests. On the one hand, they protect debtors from being perpetually trapped in a cycle of debt, offering them a chance to regain financial control. On the other, they safeguard creditors’ rights by ensuring that any assets available are liquidated and fairly distributed, thus enabling some degree of recovery. This balance is fundamental to maintaining the integrity of the credit system and ensuring that insolvency processes are equitable for all parties involved.

Historically, personal insolvency laws heavily influenced India’s approach to insolvency. Two key legislations, the Presidency Towns Insolvency Act, 1909 (‘PTIA’) and the Provincial Insolvency Act, 1920 (‘PIA’), governed personal insolvency for different regions of the country. The PTIA was applicable in the Presidency Towns – Calcutta, Bombay, and Madras – while the PIA applied to the rest of India. Although effective in their time, these laws became increasingly outdated as India’s economy modernized and expanded. As a result, the legislative framework for insolvency needed to evolve to address the complexities of the modern financial landscape.

The IBC brought a much-needed overhaul to the insolvency regime in India, providing a comprehensive legal framework for the resolution of both corporate and personal insolvencies. However, while the corporate insolvency framework under the IBC has been widely implemented, the provisions related to personal insolvency have been limited in scope. These provisions primarily apply to individuals who act as personal guarantors (‘PGs’) for corporate loans. This leaves a significant gap in the insolvency framework for other categories of individuals and small businesses, such as sole proprietorships and partnerships.

To address this gap, the Central Government (‘CG’), with the Insolvency and Bankruptcy Board of India (‘IBBI’), has proposed draft rules and regulations, including the Insolvency Resolution Process for Individuals and Firms Regulations, 2017. These proposed regulations aim to expand the application of personal insolvency laws under the IBC to include individuals outside the realm of personal guarantees for corporate debts. When implemented, these rules will provide a more inclusive and structured insolvency resolution process for all individuals, offering a more comprehensive solution for personal financial distress.

Personal Insolvency Under the IBC

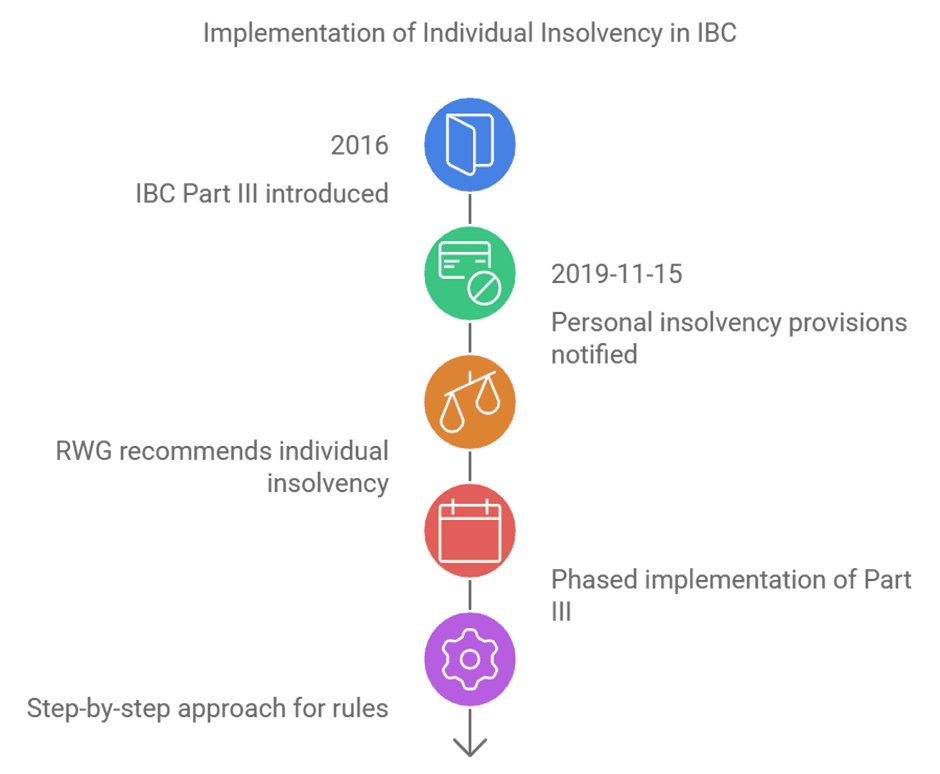

Part III of the IBC lays down the legal framework for insolvency resolution of individuals, partnership firms, and proprietorships. Prior to its enactment, India needed a modern, consolidated statute to address personal insolvency. Including personal insolvency provisions under the IBC was a significant development introduced by the Government of India (GoI) through a notification dated 15.11.2019. This marked the first comprehensive step towards incorporating individual insolvency resolution within the IBC framework.

Initially, the IBC was primarily focused on corporate insolvency, reflecting its initial purpose of addressing the growing issue of distressed companies and corporate debtors (‘CDs’). However, over time, it became clear that a structured mechanism for individual insolvency was equally necessary, particularly for those who act as PGs for corporate debts. PGs, who frequently bear significant liabilities when corporate entities default, lacked a streamlined process for resolving their insolvency issues, thus prompting the need for regulatory intervention.

The introduction of personal insolvency provisions was based on the recommendations of the Reconstituted Working Group (‘RWG’) on Individual Insolvency, which recognized the unique challenges associated with individual insolvencies. The RWG’s report emphasized that personal insolvency required a phased implementation due to the diverse nature of stakeholders involved, including individual debtors, small businesses, and partnership firms, as well as the varied types of creditor claims. In light of these complexities, the RWG advocated for a step-by-step approach to ensure a smooth and effective rollout of personal insolvency provisions.

Accordingly, the government adopted a staggered approach, beginning with the PGs and moving to CDs. This phased implementation allows for careful monitoring of the insolvency resolution process for PGs before expanding to other categories of individuals. The phased introduction ensures the framework can be refined in response to practical challenges, market dynamics, and stakeholder needs, creating a more effective and efficient system.

Therefore, while the personal insolvency framework under the IBC is still in its early stages, it represents a crucial development in India’s insolvency regime. The step-by-step expansion of Part III will ultimately allow more individuals and businesses to access structured insolvency proceedings, contributing to a more balanced and inclusive resolution framework.

Constitutional Validity of Personal Insolvency Framework

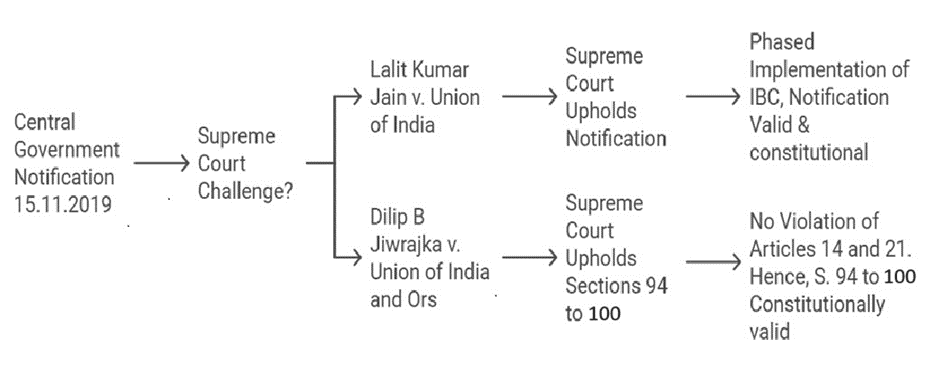

The validity of the personal insolvency framework was challenged in many cases through a writ petition. The notification dated 15.11.2019 introduced Part III of the IBC along with ss. 78, 79, and ss. 94-187, which are related to personal insolvency, was challenged, and the Supreme Court upheld the constitutional validity of both in separate writ petitions.

Constitutional Validity of Notification for Enforcement of Personal Insolvency Framework

The constitutional validity of the notification dated 15.11.2019, issued by the CG to operationalize certain provisions of the IBC concerning personal insolvency, was challenged in the case of Lalit Kumar Jain v. Union of India[i]. The notification enforced ss. 78, 79, and ss. 94-187 of the IBC, specifically in relation to PGs of CDs. This marked a significant step in the phased implementation of the personal insolvency framework under Part III of the IBC.

The petitioners, primarily PGs of corporate debts, contended that the notification selectively applied the IBC provisions only to PGs, arguing that this amounted to an unconstitutional and excessive delegation of legislative power. They asserted that the selective application of the IBC to PGs was ultra vires the IBC, as the framework did not yet apply to other categories of individuals, sole proprietorships, or partnership firms.

In its landmark decision, the Supreme Court upheld the constitutionality of the impugned notification, emphasizing that the CG’s phased approach in operationalizing the IBC was both legally sound and in line with the legislative intent. The Court observed that the IBC had been implemented progressively since its inception in 2016, with different provisions brought into force at different times. This staggered enforcement was aimed at ensuring that the necessary regulatory structures, adjudicatory bodies, and practical processes were in place before the full implementation of the IBC.

The Court rejected the argument of excessive delegation of legislative power, stating that the phased application of the IBC, including its provisions on PGs, was a deliberate and strategic policy decision that did not infringe upon constitutional principles. The phased implementation was viewed as a pragmatic response to the complexities involved in insolvency law, particularly in the context of different categories of debtors and the interconnectedness of PGs with CDs.

The decision also highlighted the integral role of PGs in the insolvency proceedings of CDs, affirming that PGs must be treated in conjunction with the corporate insolvency resolution process. The Court noted that including PGs under the IBC reflects the legislative intent to create a unified and comprehensive insolvency framework that accounts for the reciprocal relationship between CDs and their PGs.

The Court further observed that the phased implementation of the IBC was consistent with judicial interpretations on the structured application of complex legal frameworks. This approach ensured that the IBC’s provisions were not prematurely enforced without the necessary institutional and procedural foundations, thus avoiding undue hardship and confusion. The Court concluded that the notification did not violate any constitutional provisions, and its selective application to PGs was in harmony with the overarching objective of the IBC to provide a coherent, effective, and unified insolvency resolution mechanism.

By upholding the constitutionality of the notification, the Supreme Court reinforced the legislative design behind the IBC and confirmed the validity of its staged implementation. This judgment underscores the importance of a careful and methodical rollout of insolvency laws, ensuring that the interests of both debtors and creditors are effectively balanced while maintaining the integrity of the insolvency process.

Constitutional Validity of Ss. 95 to 100 of the IBC

In the case of Dilip B. Jiwrajka v. Union of India & Ors.[ii], the Supreme Court examined the constitutionality of ss. 95 to 100 of the IBC outline the insolvency resolution process for individuals, including PGs and CDs. Implemented in 2019, these provisions extend the IBC’s reach beyond corporate entities to PGs. The petitioners challenged this extension, arguing that it infringed upon as. 14 and 21 of the Constitution of India (‘Constitution’).

The primary contention raised by the petitioners was that the insolvency process under ss. 95 to 100 fails to provide adequate safeguards for debtors, particularly concerning verifying the existence of debt before initiating insolvency proceedings. The petitioners argued that the adjudicating authority ('AA') should be required to confirm the existence of a valid debt before appointing a resolution professional, as the current process does not mandate such verification at the outset. They further contended that this procedural gap disproportionately affects individual debtors and PGs, exposing them to undue reputational harm and impairing their creditworthiness. Concerns were also raised about the extensive powers granted to resolution professionals, who, the petitioners argued, wield significant influence over the debtor’s assets and affairs without prior judicial scrutiny.

The Union government's respondents defended the provisions by emphasizing the need for a streamlined and efficient insolvency process under the IBC. The petitioners argued that adding a judicial phase to verify debts at the outset would undermine the time-sensitive nature of the insolvency resolution process, which is designed to provide swift outcomes for both debtors and creditors. The respondents clarified that the role of the resolution professional is merely facilitative and not adjudicatory, ensuring that the process moves forward efficiently while adhering to the principles of natural justice.

The Supreme Court upheld the constitutionality of ss. 95 to 100 of the IBC, ruling that the insolvency process for PGs and individuals does not violate the fundamental rights enshrined in as. 14 and 21 of the Constitution. The Court clarified that the role of the resolution professional is limited to facilitating the insolvency resolution process and making recommendations to the AA without engaging in any adjudication. The AA, however, retains the responsibility of ensuring that principles of natural justice are followed, particularly under s. 100 of the IBC when it passes final orders in insolvency proceedings.

In addressing the petitioners’ concerns regarding the lack of initial debt verification, the Court ruled that while the AA is not required to verify jurisdictional facts at the initiation stage, the debtor’s rights are protected through subsequent participation in the insolvency process. The Court also found that the automatic appointment of a resolution professional and provisional measures taken at the commencement of insolvency proceedings do not constitute a breach of constitutional rights, as these steps are integral to the efficient functioning of the IBC’s framework.

The decision reaffirms that ss. 95 to 100 of the IBC are aligned with the legislative objective of providing a time-bound and effective insolvency resolution process. By upholding the constitutionality of these provisions, the Supreme Court has ensured that the IBC remains a robust and comprehensive tool for insolvency resolution, addressing both CDs and their PGs while respecting the fundamental rights of all stakeholders. The judgment further clarifies the procedural balance between expediency and protecting individual rights within the insolvency framework, reinforcing the legitimacy of the IBC’s approach to personal insolvency.

Co-Extensive Liability of the PG

Under s. 128 of the Indian Contract Act, 1872 (‘Contract Act’), the liability of PGs is unequivocally co-extensive with that of the CD. A PG’s obligations are rooted in a separate contractual arrangement, and the specific terms of the guarantee determine the scope and extent of the guarantor's liability. This co-extensive nature allows creditors to initiate legal action against both the CD and the PG concurrently or pursue them sequentially, depending on the circumstances. The creditor retains the right to recover either the full amount of the debt or any residual amount from the guarantor following the CD’s insolvency or liquidation proceedings.

One common misinterpretation is that the CD's obligations cease once a resolution plan is approved by the committee of creditors under the IBC. By extension, the PG’s liability is similarly discharged. However, Indian jurisprudence has consistently upheld the principle that a guarantor’s liability persists independently of the CD’s discharge, even where the CD’s obligations are extinguished under the IBC. High Court and Supreme Court rulings have made it clear that the liability of the PG remains intact, regardless of the CD’s insolvency resolution.

In Maharashtra State Electricity Board Bombay v. Official Liquidator[iii], the courts provided clarity on the application of s. 134 of the Contracts Act. It was held that a guarantor’s liability remains enforceable even if the CD is discharged of its liabilities through an involuntary process, such as insolvency or liquidation. The rationale behind this ruling is that the release of the CD is not due to any action or omission by the creditor. Thus, the creditor’s rights against the guarantor remain unaltered. The courts concluded that the provisions of s. 134 of the ICA, which discharges the guarantor in case of the creditor’s intentional release of the debtor, does not apply when the debtor is discharged by operation of law, as in the case of insolvency.

The well-established legal principle reinforces that while approving a resolution plan extinguishes all liabilities, claims, and dues against the CD, this discharge applies only to the CD. It does not absolve PGs, including directors of the CD, from their obligations under the contract of guarantee. The discharge of the CD is a statutory consequence under the IBC, but the PG remains bound by its independent contractual obligations to the creditors.

In Lalit Mishra & Ors. v. Sharon Bio Medicine Ltd. & Ors.[iv], the National Company Law Appellate Tribunal (‘NCLAT’) reaffirmed that the legislative intent of the IBC was not to shield PGs from creditor actions. Personal guarantees, being separate and independent contracts, do not preclude creditors from pursuing recovery through other legal avenues. The NCLAT emphasized that the IBC aims to maximize the value of the CD’s assets and resolve its financial distress. However, the personal guarantees provided by individuals remain outside the purview of the corporate insolvency resolution process and must be pursued through appropriate legal channels.

The Supreme Court, in State Bank of India v. V. Ramakrishnan[v], further observed that s. 14 of the IBC, which provides for a moratorium on legal proceedings against the CD during the insolvency process, does not extend to PGs. The Court clarified that PGs are not entitled to protection under the corporate moratorium, as they often bear unlimited liability under the terms of their guarantees. However, s. 101 of the IBC introduces a separate moratorium for PGs. Still, this moratorium is specific to the debt itself and does not protect the guarantor from being pursued for recovery during the resolution process.

In the case of Lalit Kumar Jain (Supra), the Supreme Court reaffirmed that approving a resolution plan for a CD does not automatically discharge a PG from their liabilities under the contract of guarantee. The Court ruled that a guarantor’s liability remains intact even when the principal borrower is discharged through insolvency or liquidation. This is because the guarantor’s liability arises from a separate contract, and the obligations under this contract are independent of the principal debtor’s discharge by operation of law.

Thus, Indian courts have consistently upheld the co-extensive nature of a PG’s liability under the Contracts Act and the IBC. Despite the CD’s discharge through the resolution process, the PG remains liable for the full extent of the debt. This principle ensures that creditors retain their rights to recover dues from PGs and prevents guarantors from evading their obligations through the corporate insolvency framework.

Challenges Under the Current Framework

Despite the Supreme Court’s ruling upholding the constitutionality of the notification extending the IBC’s provisions to PGs, the anticipated surge in PG insolvencies has been met with slow progress. This delay is attributed to the evolving and uncertain legal landscape surrounding the IBC, which presents several challenges in effectively implementing personal insolvency resolutions.

Corporate Debt Discharge

One significant challenge lies in the argument frequently raised by PGs that their liability is extinguished upon the discharge of the CD’s debt through an approved resolution plan. PGs contend that since the underlying debt has been resolved, they, too, are absolved of their obligations. A notable example of this issue was seen in the recent ruling by the Debt Recovery Tribunal (‘DRT’) in State Bank of India v. Prashant Ruia[vi]. The DRT rejected a claim for recovery against the PG, reasoning that the debt had been fully discharged under the CD’s resolution plan. This interpretation creates a barrier for creditors seeking recovery from PGs, as it introduces ambiguity about the extent of guarantor liability post-corporate insolvency resolution.

Jurisdictional Challenges

Jurisdictional issues have also posed significant challenges in PG insolvencies. S. 60(1) of the IBC grants jurisdiction to the National Company Law Tribunal (‘NCLT’) for insolvency resolutions and liquidations of both CDs and PGs. S. 60(2) of the IBC further provides that insolvency applications against PGs can only be submitted to the NCLT when there is an ongoing corporate insolvency resolution or liquidation proceeding. This has led some PGs to contest the NCLT's jurisdiction in instances where no active corporate insolvency process exists. The matter was clarified in State Bank of India v. Mahendra Kumar Jajodia[vii], where the NCLAT, a decision later upheld by the Supreme Court, held that the NCLT retains jurisdiction over PG insolvencies, regardless of the pendency of corporate insolvency proceedings.

However, procedural concerns remain. The NCLAT allowed for limited notice requirements at the admission stage under s. 100 of the IBC, raising questions about compliance with the principles of natural justice. A recent writ petition before the Supreme Court has challenged this process, arguing that PGs must be afforded the right to be heard before the appointment of a resolution professional. If successful, this petition could impose additional procedural safeguards, potentially delaying insolvency admissions and complicating the process.

Asset Tracing and Protection

A critical gap in the current framework concerns the need for robust asset-tracing mechanisms for PGs. While the IBC includes provisions for avoiding fraudulent and preferential transactions in the case of CDs, these provisions do not extend to PGs. This lack of safeguards opens the possibility of asset diversion by PGs before the resolution professional takes control of the guarantor’s estate. Without a mechanism to claw back such assets, the guarantor’s estate may be improperly diminished, undermining the interests of creditors. The absence of asset tracing and recovery provisions creates significant enforcement challenges, reducing the efficacy of personal insolvency proceedings.

Thus, while including PGs within the ambit of the IBC represents a significant step forward in India’s insolvency regime, the framework continues to face substantial challenges. The issues surrounding the discharge of PG liability following corporate debt resolution, jurisdictional ambiguities, and the absence of asset recovery mechanisms all contribute to a lack of clarity and enforcement difficulties. Addressing these challenges will be crucial to realizing the full potential of the IBC in dealing with PG insolvencies.

Conclusion

The personal insolvency framework under the IBC marks a significant evolution in India’s insolvency regime, extending the IBC’s reach beyond CDs to include PGs. This development is a logical progression in ensuring a comprehensive and unified approach to insolvency, especially given the crucial role that PGs play in securing corporate debts. The Supreme Court’s rulings, particularly in Lalit Kumar Jain (supra), have fortified the constitutional validity of these provisions, reinforcing that PGs cannot evade their contractual obligations simply due to the discharge of CDs in insolvency proceedings.

However, the practical implementation of personal insolvency under the IBC has encountered significant challenges. Ambiguities around the co-extensive liability of guarantors, jurisdictional issues concerning the role of the NCLT, and procedural concerns related to the protection of natural justice principles have resulted in a slower-than-anticipated uptake of personal insolvency cases. Furthermore, the absence of clear asset tracing and recovery provisions for PGs represents a substantial gap in the framework, potentially undermining creditor rights.

Despite these challenges, judicial pronouncements have provided much-needed clarity on the co-extensive nature of PG liability and the intent of the IBC to keep PGs accountable for their obligations, even after CDs are discharged. The IBC’s phased implementation for personal insolvency ensures that the complexities of personal and corporate insolvency are addressed pragmatically. Still, continued refinement of the legal framework and procedural mechanisms is essential for greater efficiency.

In light of these developments, while the IBC has successfully laid the foundation for a robust personal insolvency regime, further legislative and judicial intervention is required to address the existing gaps and uncertainties. This will ensure that PG insolvency resolutions are handled equally efficiently and fairly as corporate insolvencies. This will ultimately enhance the IBC’s overall objective of creating a balanced, time-bound, and effective insolvency resolution framework for all stakeholders involved.

* *

End Notes

[i] [2021] 127 taxmann.com 368 (SC).

[ii] [2023] 156 taxmann.com 304 (SC).

[iii] 1982 AIR 1497, 1983 SCR (1) 561.

[iv] Company Appeal (AT) (Insolvency) No. 164 of 2018.

[v] Company Appeal (AT) (Insolvency) No. 164 of 2018.

[vi] IA No. 92 of 2022 in OA No. 650 of 2018. [Debts Recovery Tribunal at Ahmedabad].

[vii] Company Appeal (AT) Insolvency No. 60 of 2022.

Authored by Ritik Kumar Jha, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions.

AUTHORED BY

More Insights

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.

2026-04-23

18

min read

Mandatory Pre-Deposit for Appeals in Indirect Tax Laws: A Barrier to Justice?

Mandatory pre-deposit has become a defining feature of indirect tax litigation, balancing revenue protection with access to appellate remedies. While the shift to a fixed statutory framework has improved procedural efficiency, it also raises concerns regarding financial barriers and effective access to justice. This insight examines the legal evolution, judicial interpretation, and practical implications of the regime.

2026-04-20

10

min read

Legal Strategy in Startup Ecosystems: Risk Mitigation and Value Maximisation from Formation to Exit

Legal structuring across the startup lifecycle extends beyond compliance to shape valuation, governance, and investor confidence. From intellectual property protection and entity selection to funding arrangements and exit mechanisms, each stage involves critical legal considerations that determine risk allocation and long-term scalability within a regulated framework.