Introduction

The Goods and Services Tax Policy Wing - Central Board of Indirect Taxes and Customs (‘CBIC’) has recently released a circular dated 10.09.2024[i], clarifying certain issues pertaining to the Goods and Services Tax (‘GST’) treatment that is to be accorded to advertising services rendered by Indian advertising companies (‘ad cos.’) to foreign clients. Such clarification has been issued against the backdrop of many ad cos. providing services to foreign clients. These companies have been engaged in providing comprehensive advertising services to foreign clients and procuring media space for them from domestic media companies. The circular provides clarification on 3 important issues referred to by the advertising industry. The issues and their respective clarifications are explained as follows:

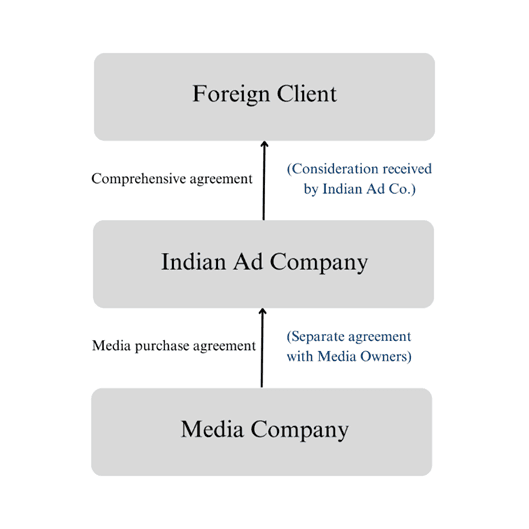

Issue 1: Whether an Indian advertising company is an ‘intermediary’ between the foreign client and the media owners as per s. 2(13) of the IGST Act?

As per s. 2(13) of Integrated Goods and Services Tax Act, 2017 (‘IGST Act’), an intermediary is a person who arranges or facilitates the supply of goods or services between two or more persons. As per the section, any person who supplies goods or services on their own account is excluded from the ambit of ‘intermediary’.

The circular clarifies that since most foreign clients enter into comprehensive agreements with Indian ad cos. to outsource their entire advertising activity, this results in a principal-to-principal relationship between the foreign client and the media companies, and thus, the same cannot be categorised as ‘intermediary’ for transactions under GST.

This is because in such arrangements, the ad cos. enters into two separate contracts: (1) with the media platform for the purchase of advertising space and (2) with a foreign client for comprehensive advertising services rendered to them. Therefore, in such a scenario, the ad cos. render services on their own account rather than facilitating the supply of services between foreign clients and media companies.

The circular observes that ad cos. would be ‘intermediaries’ in arrangements where the media company directly invoices the foreign client while the ad co. facilitates the transaction. In such a case, the place of supply would be the location of the supplier, i.e., India.

Issue 2: Whether a foreign client’s representative in India or the target audience of the advertisement in India can be considered the ‘recipient’ of the services under s. 2(93) of the CGST Act?

As per s. 2(93)(a) of the Central Goods and Services Tax Act, 2017 (‘CGST Act’), a person who is liable to pay consideration for the supply of services is the ‘recipient’ of such service.

The circular clarifies that even when the foreign client has an Indian representative or where the target audience resides in India, the onus/liability of payment of consideration is upon the foreign client. Therefore, such a representative or target audience cannot be regarded as a ‘recipient’ of services, and thus, the foreign client would be the ‘recipient’ as per s. 2(93) of the CGST Act.

Issue 3: Whether the advertising services provided by the advertising companies to foreign clients can be considered performance-based services as per s. 13(3) of the IGST Act?

S. 13 of the IGST Act prescribes a place of supply of services where the supplier or recipient's location is outside India. S. 13(2) IGST Act is the general provision that provides the place of supply as the ‘location of the recipient of service’, whereas s. 13(3) is an exception provision for performance-based services, providing their place of supply to be ‘where the services are performed’. For example, hypothetically the place where advertisements are run, i.e., India.

The circular clarifies that running advertisements does not require the physical presence of the recipient (in this case, the foreign client) or their representative. Furthermore, since neither clause (a) or (b) of s. 13(3) IGST Act are met, the default rule specified in s. 13(2) will apply; the place of supply of such services will be outside India, and the supply of such services will be eligible for export benefits under s. 2(6) of IGST Act on satisfaction of conditions specified therein.

Conclusion and Comments

This circular provides much-needed clarity for the Indian advertising industry, especially in the context of the GST treatment for services provided to foreign clients. By affirming that advertising agencies act as principals rather than intermediaries when dealing with foreign clients and media companies, the circular removes ambiguity around the place of supply, ensuring that such services qualify as exports and are eligible for GST exemptions. Furthermore, the distinction between principal-to-principal contracts and intermediary roles ensures that advertising agencies are correctly classified. Ultimately, the clarification issued by the department streamlines the tax process to foster greater ease of doing business within India’s thriving advertising sector.

End Note

[i] Circular no. 230/24/2024-GST dated 10.09.2024.

Authored by Aditya Gupta, Advocate at Metalegal Advocates. The views expressed are personal and do not constitute legal opinions.

More Insights

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.

2026-04-23

18

min read

Mandatory Pre-Deposit for Appeals in Indirect Tax Laws: A Barrier to Justice?

Mandatory pre-deposit has become a defining feature of indirect tax litigation, balancing revenue protection with access to appellate remedies. While the shift to a fixed statutory framework has improved procedural efficiency, it also raises concerns regarding financial barriers and effective access to justice. This insight examines the legal evolution, judicial interpretation, and practical implications of the regime.

2026-04-20

10

min read

Legal Strategy in Startup Ecosystems: Risk Mitigation and Value Maximisation from Formation to Exit

Legal structuring across the startup lifecycle extends beyond compliance to shape valuation, governance, and investor confidence. From intellectual property protection and entity selection to funding arrangements and exit mechanisms, each stage involves critical legal considerations that determine risk allocation and long-term scalability within a regulated framework.