The arm’s length principle is the international standard for determining the taxability of profits resulting from transactions between related entities. This article analyses the principle's conceptual bases, its implementation, its role in preventing profit shifting, and compliance with global standards. The study contrasts arm’s length price with fair market value and details the methodologies for determining ALP. Additionally, it explores the interaction between transfer pricing, customs valuation, and FEMA pricing, addressing harmonization challenges.

I. Introduction

Arm’s length principle forms the bedrock of Indian (or, of most countries’) transfer pricing regulations. This principle is instrumental in ensuring that transactions between associated enterprises reflect market conditions as if the entities were independent and unrelated to each other, and the transactions between them take place only on pure commercial bases.

Within the Indian legal framework, the principle is enshrined in the Income-tax Act, 1961[i], laying down specific anti-avoidance rules in the form of transfer pricing provisions. These rules are aligned with global standards and address the challenges of shifting profits outside India. This article delves into the philosophical underpinnings, statutory bases, and practical implications of the arm’s length principle in the context of Indian transfer pricing law.

II. What is the Arm’s Length Principle?

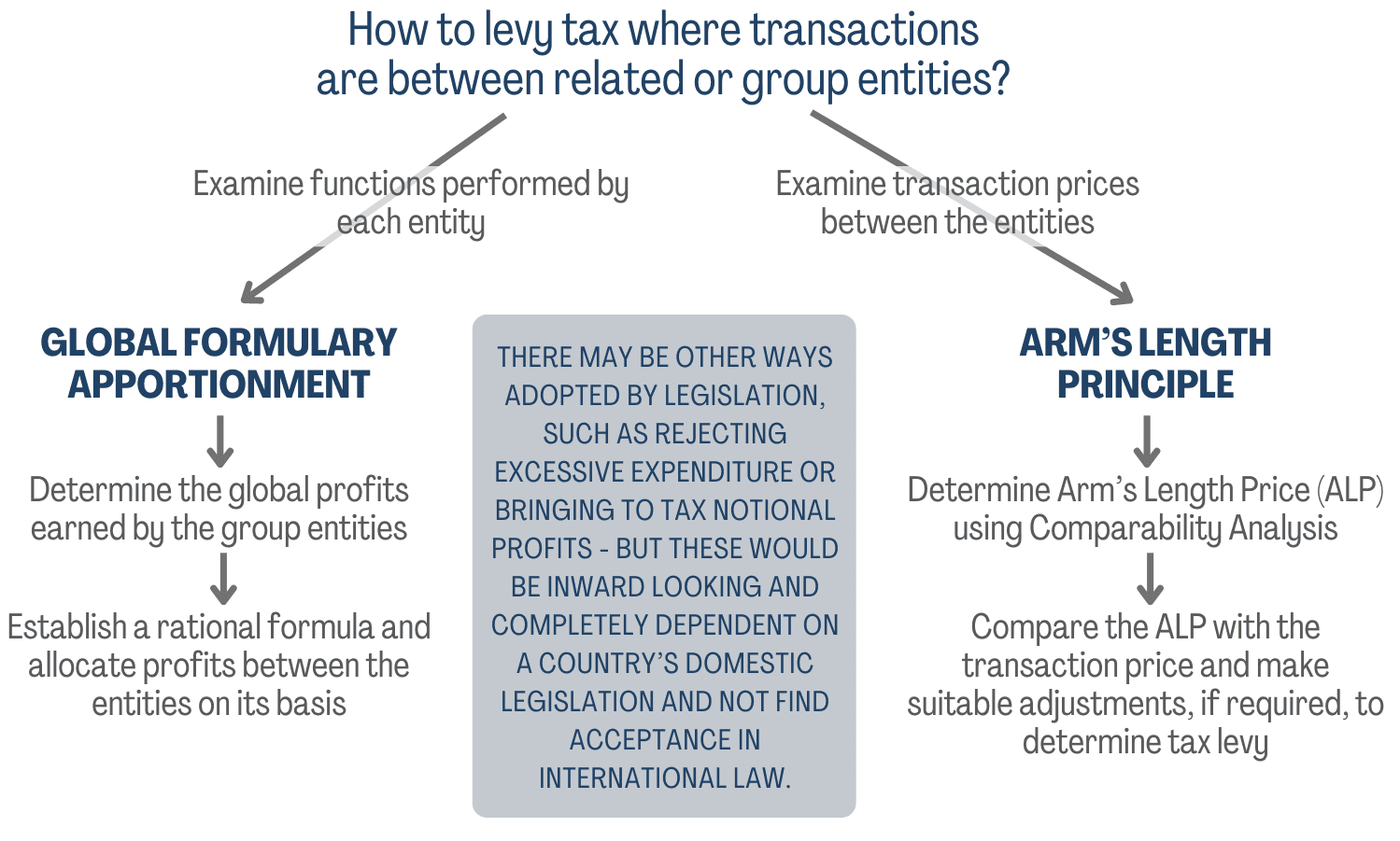

The arm's length principle (‘Principle’) is the situation or condition that the parties to a transaction are acting independently of each other, and not subservient to any other interest. Such a transaction is called an arm’s length transaction, and the price at which it is affected is called the arm’s length price (‘ALP’).

The Principle dictates that the price in a transaction between related parties should be equivalent to the price that would have been charged between unrelated parties in an uncontrolled environment or manner. The Principle thus aims to ensure that intra-group transactions mirror those that would occur in a competitive market, thereby preserving the tax base of the jurisdictions involved. The Principle finds relevance not just in tax law but also in laws governing other aspects related to cross-border transactions, such as the Foreign Exchange Management Act, 1999 (‘FEMA’), where it is desired by the law that transactions should be carried out at an arm’s length price in order to control, conserve, and regulate the flow of foreign exchange.

In the context of international tax, the Principle finds its basis in Article 9 of the Model Tax Convention of the OECD[ii]. The Article states that where conditions are imposed between two related enterprises in their commercial or financial relations, which differ from those which would have been made between independent enterprises, profits should be determined ignoring such conditions – that is, profits which should have accrued to one party and which haven’t accrued because of such conditions should be included as profits of such party. Thus, the Principle finds its roots in transfer pricing law as well as international tax law.

As an alternative to the Principle, another approach has been much deliberated in the international arena with respect to allocating profits between related enterprises. This approach termed Global Formulary Apportionment (‘GFA’), involves (i) determining the constituent units or entities who have transacted with each other, (ii) determining the global profits earned by these entities together, and (iii) establishing the formula to be used for allocating profits between the constituent entities (this could be on the basis of costs or assets or payroll or turnover or other similar variables). However, this method has largely been rejected as an alternative to the arm’s length principle.

III. Arm’s Length Price v. Fair Market Value

The terms ‘arm’s length price’ and ‘fair market value’ (‘FMV’) are both used to assess the value of transactions and/or assets in different contexts, particularly in law, finance, and taxation. Although they may seem similar, they have distinct applications and implications.

From a contextual perspective, ALP is specifically used in the context of transfer pricing to regulate transactions and ensure that their value, for the purposes of tax computations, is considered appropriately. On the other hand, FMV is a broader concept used in various contexts other than tax, such as real estate, share valuations, and business valuations.

From a transactional perspective also, the two differ. While the ALP focuses on creating parity between controlled/related party transactions and uncontrolled transactions, FMV refers itself to open market value under uncontrolled conditions.

While ALP is statutorily computed based on prescribed methods (as would be discussed later) and not much flexibility is provided for in the computation, FMV is a generic computation used both in regulated as well as unregulated contexts. For instance, an immovable property purchase would require an FMV computation by the parties and this may be based on inquiries, bids from other prospective buyers, or even a mark-up added to the circle rate or stamp duty value of the property.

IV. Core of the Principle: Comparability Analysis

The end-result sought to be achieved by the application of the Principle is to determine the ALP. Constituting the heart and core of the Principle is comparability analysis. This involves a comparison of the conditions in a controlled transaction with the conditions that would have been made had the parties been independent and undertaking a comparable transaction under comparable circumstances. This involves a methodical approach and requires factoring in several aspects crucial for an accurate comparison.

Firstly, the identification of commercial and financial relationships between the parties has to be precisely done. This would require analysing the contractual terms of the transaction, carrying out an analysis of the functions performed by each party, and noting the characteristics and nature of the goods and services involved in the transaction. Further, differences in various markets and the business strategies involved (e.g., innovation, risk diversity, duration of arrangements etc.) have also to be taken into account.

Secondly, the actual transaction would have to be identified or discovered from written contracts as well as the conduct of the parties. In case the transaction, in its substance, differs from what has been spelt out in the written contract, the comparable transaction would differ. In short, the substance of the transaction has to be compared. For instance, a contract manufacturer may actually be and behave like an actual manufacturer if it assumes all risks in practice, and it should be compared with an actual manufacturer and command higher profit attribution.

Thirdly, other factors which have a significant bearing on price and business model should be taken into account – this would include analyses of losses, the effect of government policies, other duties and taxes, and local market features. These factors may vary over time and the comparison cannot be anachronistic.

Lastly, intra-group synergies play an important role in determining the actual price. Economies of scale and combinations of manpower and assets could exert a great influence on pricing across the lifecycle of the transaction. For instance, if goods are purchased in India and sold to group subsidiaries abroad, any volume discount that has been made available in India thus lowering the price, should be factored in. It may thus be found that the Indian entity is selling at less than the market price because of such a discount.

V. Price Determination Methods

Comparability analysis involves a thorough examination of the terms and conditions of transactions between associated enterprises and comparing them to those between independent enterprises. The factors considered include the nature of the goods or services, contractual terms, market conditions, and business strategies. The primary methods endorsed by Indian law as well as international guidelines (e.g., the OECD guidelines on transfer pricing) include[iii]:

Comparable Uncontrolled Price (‘CUP’) Method: Prices in comparable transactions between unrelated parties are directly used. The comparison done here is directly between the prices of (i) the transaction under review, and (ii) another transaction between independent parties involving the same/similar goods or services.

Resale Price Method (‘RPM’): The price at which a product purchased from an associated enterprise is sold to an independent party is considered. The amount of profit retained by the reseller here is compared with other independent resellers.

Cost Plus Method (‘CPM’): The costs incurred by the supplier in a controlled transaction are marked up to arrive at an arm's length price.

Profit Split Method (‘PSM’): Profits from transactions are split based on how independent entities would have divided them under similar circumstances. This is generally done by identifying various functions performed by the constituent group entities and the profit split is determined based on who performed which function(s).

Transactional Net Margin Method (‘TNMM’): Net profit margins relative to an appropriate base (like costs or sales) are used to establish whether they are at arm’s length. Generally, this comparison is done at an entity or function level.

Though the most common statutorily prescribed method is to conduct a comparability analysis, other methods also find relevance in certain peculiar scenarios. As an example, one may say that if related parties have determined the consideration based on an international index (say, in a transaction involving the sale-purchase of coal), the price should be treated as the ALP. In India, there is a sixth method (the Other Method) that has also been prescribed – this is the residuary method, and it allows for any method which is rational and objective to be used for the determination of the ALP.

VI. Interplay between Transfer Pricing, Customs Valuation, and FEMA Pricing

The convergence of transfer pricing with customs and FEMA regulations presents a complex interplay, as each framework has distinct objectives but overlapping concerns.

Customs authorities are concerned with the value of goods at the point of import or export to determine duties, while transfer pricing regulations aim to adjust prices between associated enterprises for tax purposes. While the true objective in both cases may be to determine the accurate arm’s length price of the transaction, the laws intend to work the opposite way.

Take, for instance, an import transaction where an Indian entity imports certain goods from its related group entity. Customs duty on imports would be higher if the price determined is higher. On the other hand, since the purchase price would be sought as a deduction while computing the profits of the Indian entity, the income-tax leviable would be higher if the price determined is lower. This contradictory approach often results in different valuations being arrived at by the two authorities.

Similarly, where FEMA prescribes that a transaction has to be carried out at a price in accordance with an internationally accepted pricing methodology, the arm’s length principle becomes squarely applicable. However, depending on whether the foreign exchange is coming into or leaving the country, the approach of authorities may differ, resulting in a contradictory outcome under the two laws.

While the arm’s length principle may be relevant for customs valuations or FEMA pricing, its application is where the two laws or authorities may differ. Harmonization between the statutory authorities – the Central Board of Direct Taxes (for income-tax or transfer pricing), the Central Board of Indirect Taxes and Customs (for customs duty), and the Directorate of Enforcement or Reserve Bank of India (for FEMA) – is the only practical way to resolution.

VII. Conclusion

The arm’s length principle is the internationally accepted standard for determining the price at which related party or intra-group transactions should be carried out. It is notable that the principle does not prohibit such transactions but merely seeks to regulate them for the purpose of determining accurate profits which could be rightfully taxed in respective jurisdictions.

The Indian adoption of the Principle mirrors the international consensus and also factors in India-specific anti-avoidance rules to make the checks and balances robust. Various developments in global taxation frameworks, such as the OECD’s Base Erosion and Profit Shifting (‘BEPS’) actions, have influenced further refinements in the Indian transfer pricing regulations. The dynamic interplay between national legislation and global standards necessitates ongoing vigilance and adaptation, ensuring that the ALP remains effective in meeting both current and future challenges in international taxation.

End Notes

[i] Indian transfer pricing regulations are contained in sections 92 to 92F of the Income-tax Act, 1961.

[ii] Model Tax Convention prepared and issued by the Organization for Economic Co-operation and Development (OECD) forms the basis of bilateral tax treaties across the world. Similar model tax conventions have been issued by the United Nations (UN Model Tax Convention) and the United States of America (US Model Tax Convention).

[iii] Section 92C of the Income-tax Act, 1961 prescribes these methods.

Authored by the Editorial Team, Metalegal Advocates. The views expressed are personal and do not constitute legal opinion.

AUTHORED BY

More Insights

24-07-2026

10

min read

‘Shylockian’ Lending is ‘Squeezing of Blood’: NCLT Moves Beyond Debt & Default to Reject a Section 7 Application

In a rare departure from the conventional debt-and-default enquiry under section 7 of the IBC, the NCLT, Kochi Bench rejected the financial creditors' petition after characterizing the underlying arrangement as a ‘Shylockian system’ of lending. This court ruling discusses Shylockian lending and examines the strength of the Tribunal's focus on the economic substance of the transaction against established legal principles governing admission under section 7 of the IBC.

10-07-2026

7

min read

Faceless Reassessment after S. 147A: What the Supreme Court Did – and Did Not – Decide

The Supreme Court's decision in Tej Pratap Singh does not settle the JAO–FAO controversy. Following Parliament's retrospective insertion of s. 147A, it remands the issue to the High Courts for fresh consideration. Faceless reassessment was never merely about moving tax files from paper to portal; it fundamentally changed the statutory authority responsible for communicating with the taxpayer, examining the record, drafting the order and completing the assessment. The real question now is how far a retrospective legislative clarification can go.

22-06-2026

8

min read

Claim Admission is not Debt Acknowledgement: Supreme Court on RP’s Role & Limitation under the IBC

Can admission of a claim by a Resolution Professional extend limitation under section 18 of the Limitation Act? In Shankar Khandelwal v. Omkara Asset Reconstruction Pvt. Ltd., the Supreme Court answered this question in the negative, holding that claim admission during CIRP is merely a statutory claim-verification process and not an acknowledgement of debt. The ruling clarifies the RP’s non-adjudicatory role and reinforces important principles governing limitation under the IBC.